It’s National Homeownership Month: Chase Debuts Updated Offerings andReveals First-Time Homebuyer Attitudes Study

Amid Economic Fluctuations, 70% Of First-Time Buyers Still See Homeownership As An Important Step To Building Wealth

Chase Home Lending unveiled a refreshed suite of homebuyer resources and findings from a recent consumer survey. Chase’s new homebuyer product offerings, educational resources, and easy-to-use tools have been designed to help consumers navigate the homebuying process and manage homeownership.

Despite the fluctuating housing market this past year, Chase’s latest First-Time Homebuyer Study revealed that confidence levels remain high with 44% of respondents indicating they are confident they’ll be financially ready to purchase in the coming year, up 12% YoY.

Refreshed Suite of Chase Offerings and Educational Resources

article continues after advertisement

Chase has expanded its portfolio of resources to support customers on their path to homeownership. New and updated resources include:

Lock and Shop: Chase’s new Lock and Shop offering allows you to lock in your mortgage rate for 90-days with

no upfront fee when using Chase Homebuyer Advantage.

Locking in a rate helps customers move quickly and gives them peace of

mind while shopping around for a home. Customers must find their

property within 60 days, and will have the option of a one-time float

down if rates improve. Once a customer finds their

home, they’ll also have the added confidence of Chase’s Closing Guarantee,

which guarantees an on-time closing in as little as 21 days, or the customer will receive $5,000.

Beginner To Buyer Season II Now Available: Chase recently launched the second season of its award-winning homebuyer education podcast.

Beginner To Buyer

offers 10 new episodes featuring conversations

with real buyers and expert guests discussing homebuying and ownership,

home equity, common misconceptions, renovations, and investment

properties. Buyers can dive deeper into these topics and more in Chase’s

Homebuyer Education Center.

Savings + Assistance Programs: Finding homebuyer grants and assistance programs is now quick and easy with Chase’s

Homebuyer Assistance Finder.

Users can search and discover

grants and programs they may qualify for, like Chase’s $5,000 grant for

eligible homebuyers purchasing in majority-Black and Hispanic

neighborhoods throughout the U.S.

$200 Pilot Program:Prospective buyers with an active loan offer from another lender can

compare their offer to Chase’s with a home lending advisor. Chase will

give eligible buyers $200 if they can’t match the offer or do better.

The

benefit is currently available for Chase customers

in Houston, Ohio, and Arizona.

“The homebuying process can be complex, so it’s critical that homebuyers have the right knowledge, tools and experts to help them,” said Sean Grzebin, Head of Consumer Originations, Chase Home Lending. “The latest set of resources from Chase, coupled with our network of home lending advisors, were designed with the current needs of homebuyers in mind, like locking in a rate and finding opportunities for savings. We’re excited for consumers to explore our updated offerings and engage with tools that can help them achieve homeownership.”

New Research From Chase

The study was commissioned to better understand the needs of first-time homebuyers purchasing amid an uncertain economic environment. Homebuying attitudes, behaviors, and expectations were evaluated, specifically as it relates to confidence, financial readiness, and more. Though the current state of the economy has a considerable impact, 58% of respondents said that they were likely to purchase in the next 12 months, and 70% still see homeownership as an important step to building wealth.

article continues after advertisement

“Prospective homebuyers are eager to tap into the wealth-building capabilities that homeownership brings,” shared Grzebin. “Despite market uncertainty and lengthened timelines, first-time buyers are making the necessary lifestyle adjustments to reach their homeownership goals.”

Respondents know what they need to do to get financially ready for homeownership, and confidence in their financial readiness is improving (up 12% YoY). Two-in-three respondents have improved their credit score and implemented budgeting techniques to save more for a home. Sixty-four percent are working to improve their credit score, 63% are creating and sticking to monthly budgets, and 67% are making lifestyle adjustments.

The study is based on the responses of 1,900 U.S.-based consumers fielded in Q4 2022 amongst those who have never owned a home. For more information about Chase Home Lending, visit www.chase.com/mortgage.

Additional survey findings:

Black Americans represent 21% of first-time homebuyers in 2022.

Thirteen percent of first-time homebuyers are Hispanic.

Single women make up 22% of first-time homebuyers.

First-time homebuyers are more likely to be married or partnered Millennials

(56%), but nearly 40% are single. Twenty-five percent are Gen X, and even some

(7%) Boomers are entering the homebuying process for the first time.

One-in-four first-time homebuyers moved in with their parents/family as a money-saving strategy, up

12% YoY.Two-in-five future homeowners plan to move in with family, up from

one-in-five last year. Even Gen X is more likely to resort to live with family than a year ago, with

19% having already moved in (up from 10% in 2021), and an additional

14% (up from 7% in 2021) expecting to do so.

Sixty-three percent know the financial-related changes and activities they need to do to qualify for a loan.

Fifty-nine percent know how much money they need to have to purchase a home, yet

46% are not sure they will ever be able to save enough.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/save-money-to-buy-a-house.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-09 05:03:332023-08-09 05:03:38Saving Up To Buy A Home—Would You Consider Moving In With Family? Some Buyers Are

The 2023 year continues to be one of the most interesting, perplexing, and challenging years that many of us have ever seen. From my perspective, there has never been a year like this year to compare it to as it relates specifically to housing, finance, investments, insurance, and to our federal government.

The only constant in life is change. Remember, if you always do what you’ve always done, you will always get what you’ve always gotten. As such, please be flexible and ever-changing as needed to minimize your downside risks and to maximize your financial gains.

Let’s take a look next at my Top 10 topic points that I will be sharing and discussing with my So-Cal Real Estate Investors group this month:

article continues after advertisement

1. Credit downgrades for the US, Fannie Mae, and Freddie Mac:

The Fitch credit rating agency just downgraded our federal government and the two largest secondary market investors for 70% of all mortgages named Fannie Mae and Freddie Mac, which have both been under government control since the fall of 2008 when they both almost imploded. The new credit rating is AA+ for all three entities after falling from the highest AAA credit rating.

As a result, the borrowing costs will likely increase while moving mortgage rates higher along with the 10-year Treasury yield which is inverse to the 10-year Treasury bond price like a seesaw. All 30-year fixed mortgage rates are tied to the 10-year Treasury yield directions, not to the fed funds rate which affects other consumer debts like credit cards, school loans, and car loans. Don’t be surprised if we soon see double-digit mortgage rates above 10%. The all-time record high 30-year fixed mortgage rate reached 18.6% in October 1981, by comparison.

Both Fannie Mae and Freddie Mac are highly leveraged with derivatives (a complex financial and insurance hybrid instrument) which can cause them to default on their investments due to triggering factors like rising distressed mortgage or foreclosure rates. If so, they may be forced to sell off some of their tens of millions of mortgages held in their portfolio to deep-pocketed corporations like BlackRock, Vanguard (largest BlackRock shareholder), and Blackstone (a BlackRock spinoff that’s also the world’s largest commercial real estate owner).

2. Why did mortgage rates reach all-time record lows in recent years?

Answer: The Federal Reserve created the Quantitative Easing (QE) program in November 2008 shortly after the US and global financial markets almost collapsed on September 29, 2008. The QE program is a fancy name for creating money out of thin air to buy stocks, bonds, and mortgages so that asset values don’t fall.

Back in 1961, President John F. Kennedy helped back the Operation Twist monetary policy program in an attempt to drive down long-term interest rates while buying and selling gold and gold-backed dollars at the same time. The “twist” name was partly derived from the Chubby Checker Twist dance craze.

In 2011, Operation Twist was brought back on a larger scale as both short-term and long-term bonds were simultaneously purchased and sold to artificially suppress the 10-year Treasury yield while driving the 30-year mortgage rate down to as low as the 2% rate ranges to boost home sales and prices. In recent years, the Federal Reserve became a net seller of assets purchased through Quantitative Easing. Due to fewer buyers for our debt, the lowered demand pushes the price down while boosting the 10-year Treasury yield. When bond prices fall, yields and corresponding 30-year fixed mortgage rates and borrowing costs rise.

The Fed’s record-setting rate hikes makes the borrowing costs for the US Treasury much higher as well. We’re on pace for $1 trillion dollars per year in interest payments made on the all-time record federal debt.

3. Insurance costs continue to skyrocket:

About 22% of homeowner insurance companies have completely stopped offering homeowners insurance here in California. As shared before, more than 70% of residential properties in California have a mortgage that requires active homeowners or landlord insurance. If not, it can trigger a foreclosure filing because the lender or mortgage loan servicing company requires homeowners insurance that lists them as a “named insured” in the event of a fire, flood, or some other type of property damage.

State Farm, Farmers, AIG, Chubb Geico, and others are just some of the insurance companies that have decreased or completely eliminated the issuing of new or renewal policies in California, Florida, and elsewhere. The reinsurance market is freezing up for insurance carriers, which is somewhat akin to their version of Fannie Mae, Freddie Mac, or secondary market derivatives investors who replenish capital for banks or insurance companies.

Due to fewer investors for riskier insurance in the reinsurance marketplace and fewer insurance companies willing to write new policies, the prices charged for new borrowers has absolutely skyrocketed. For example, a homeowner in St. Augustine, Florida (America’s first city) saw her annual insurance premiums for her 120-year old home rise from $8,800 to $36,000.

4. Housing and mortgage trends nationwide:

There are 140 million housing units in America.

64.8% of homes have a mortgage (96,320,000).

31.2% of homes have no mortgage (43,680,000).

There are almost one million Airbnb and VRBO rental units.

There are currently 1.7 million housing units in America under construction.

There are 44 million rental units across the nation.

80% of retirees own a home while almost half live near poverty.

Retirees (Baby Boomers and older Generation X) own 55.58% of the nation’s housing stock (55.8% of 140 million housing units = 77,812,000; 44% of these units have a mortgage or 34,237,280 properties). If half of these property owners are in distress, this could equal 17,118,640 properties, which might be equal to almost 39% of the rental market.

The IRS continues to remove family transfer benefits by way of trusts and other entities that may rapidly increase the amount of capital gains taxes which the heirs of older American property owners must pay following death. If so, it may accelerate the number of future listings so that heirs can pay their higher taxes.

5. Homeowner bailout options:

Forbearance agreements: The lender agrees to postpone or delay their foreclosure actions with the delinquent borrower. Sometimes, these foreclosure postponements may last months or years.

Deferment: The lender agrees with the borrower’s request to delay or defer their delinquent payments until a later date. In some cases, the late payments and penalties are added years later when the loan may become all due and payable.

Loan modification: The lender or mortgage loan service company agrees to reduce the existing interest rate and/or monthly payment amount so that the mortgage is more affordable as a way to avoid foreclosure.

Loan repayment plan: Both the lender and borrower mutually agree to add unpaid delinquent payments and late fees to the existing mortgage which may slightly increase their monthly payments or increase the loan term to give the borrower more time.

Reinstatement: After the borrower and lender agree to modify the monthly payments to avoid foreclosure, the loan is removed from foreclosure status and reinstated in “good standing.”

Seller-financed sales: If the homeowner needs a quick sale to a new buyer who can effectively take over his monthly mortgage payments and give the seller some much needed cash, the seller may consider creating some type of wraparound mortgage {contract for deed or all-inclusive trust deed (AITD)} or “subject-to” property transfer in which the buyer receives the deed to the property that is “subject-to” the existing mortgage still secured by the property.

Short sale: If and when the mortgage debt is greater than the current market value for the property (aka “upside-down” mortgage), the homeowner may consider contacting an experienced local Realtor who can help negotiate a discounted mortgage payoff with the lender when they find a qualified new buyer.

“Cash for Keys”: During the depths of the last major national foreclosure crisis between 2009 and 2013 especially, lenders were offering delinquent homeowners upwards of several thousand to $25,000 + to vacate the home while not damaging it or removing appliances.

Bankruptcy: For homeowners who are days away from losing their home at the final lender auction sale, they may consider filing Chapter 7 (complete liquidation of most debts) or Chapter 13 bankruptcy (a longer term workout payment plan).

6. The collapsing automobile lending sector: There are now 20,000 car repossessions per day and 600,000 repos per month.

Car insurance has increased almost 20% over the past year.

In 2019, the average car payment was near $350 – $375. Today, it’s closer to $730 per month. Yes, car payments have doubled in just four years as the purchasing power of the dollar rapidly declines.

The average cost of full coverage car insurance in Florida is now $300 per month. In 2021, Florida averaged more than 1,100 car accidents per day with 449 of these accidents involving alleged injuries which is a major factor for skyrocketing insurance costs there and elsewhere.

85% of new cars are financed with upwards of 125% loan-to-value (LTV) being fairly common partly to cover taxes, tags, warranties, and other costs.

1-in-6 Americans pay more than $1,000 per month for car payments. After adding insurance ($200 to $300+), gasoline ($200 – $300+), oil changes, and other maintenance expenses to the monthly payment, many people are paying upwards of 20% to 40%+ of their gross monthly income just for their car while paying another 40% to 50%+ per month for housing. (Partial source: First Notebook)

The choice between paying a mortgage or rent payment and making a car payment on time becomes more challenging as the economy continues to weaken.

7. Commercial real estate trends:

Multifamily apartment buildings have fallen the most out of all commercial property asset classes with a -13.8% year-over-year price drop as of May 2023. This is almost double the annual percentage losses for office buildings.

Right now, we’ve never had more residential housing units under construction at the same time with upwards of 1.7 million units, which includes a high percentage of new apartment units. The wave of new housing units that later hit the market for sale or lease may drive down sales and rental prices for other nearby properties.

Approximately 22% of all commercial mortgages nationwide were non-recourse loans as of 2021, per the Federal Reserve. A “non-recourse” loan makes it easier for the borrower to walk away and avoid deficiency judgments.

article continues after advertisement

8. Estimated U.S. Cost of Living:

Food – $1,000 per month Car Payment – $716 per month Car Insurance – $150 per month Gas – $200 per month Cell phone – $100 per month Housing – $1,702 (average one-bedroom apartment rent) Health or Medical Insurance – $500 per month Utilities and Internet – $150 per month (it’s closer to $500/month in CA) Student Loans – $300 (monthly payment is 40% below national average) Credit Cards – $300 (monthly payment is 40% below national average) —————————– Total: $5,118 per month Annual: $61,416

Median Individual Gross Income: $34,987 Median Individual Gross Losses (taxes not included): – $26,429 (negative) Median Household Income: $80,440 (two or more income sources)

How to set aside money each year: If you break down $10,000 into a daily savings goal, you would need to save about $27 per day to reach $10,000 in one year. To save $20,000 per year, reduce your monthly expenses by $54 per day.

9. Credit card debt:

Unpaid credit card debt recently surpassed $1 trillion for the first time ever and rates and fees reached all-time record highs this year.

“A credit card borrower with the average $5,733 credit card balance at 20.55% will be in debt for over 17 years if they make just the minimum payments every month, according to Rossman. They will also pay about $8,400 in interest on top of the $5,733 balance, he said.” – CNBC

Sadly, a higher percentage of credit card rates today are closer to 25% to 30%+, so it will take much longer to pay the debt off.

Paying off credit card debt: 1. Opt for zero percent balance transfers; 2. Create a debt payoff plan; 3. Seek professional help; 4. Keep saving, if possible; and 5. Consider filing for bankruptcy protection (as low as $200 online for do-it-yourself plans). If so, I will teach you how to quickly rebuild your credit after the Chapter 7 bankruptcy discharge.

10. Finding distressed properties:

There are millions of distressed homes in probably just California alone. Please look for unkept front lawns, FSBOs (For Sale by Owner), and seek out distressed property lists that may include mortgage, homeowners, and property tax lien lates.

Network with groups like ours and share business cards with your sphere of influence which include details about how you offer quick cash for homes. If you have an exceptional deal but no cash, please bring the deals to our next meetings or email them to me.

Rick Tobin has worked in the real estate, financial, investment, and writing fields for the past 30+ years. He’s held eight (8) different real estate, securities, and mortgage brokerage licenses to date and is a graduate of the University of Southern California. He provides creative residential and commercial mortgage solutions for clients across the nation. He’s also written college textbooks and real estate licensing courses in most states for the two largest real estate publishers in the nation; the oldest real estate school in California; and the first online real estate school in California. Please visit his website at Realloans.com for financing options and his new investment group at So-Cal Real Estate Investors for more details.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/trends.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-08 01:51:002023-08-08 01:51:05Top 10 Housing, Financial, and Government Trends

Attention real estate investors, broker/agents, private lenders, and REI professionals, Realty411 has exciting news regarding their upcoming In-Person Event in Irvine, California.

Our special one-day conference will host incredible educators from

around the country, who are ready to share their valuable insight.

Be

sure to pencil this event on schedule now. Sophisticated investors

won’t want to miss out on the updated news on both local and national

markets, real estate trends, plus the latest industry information.

article continues after advertisement

Don’t

forget about this brand-new event designed to share the latest news on

real estate investing. Our educators will be providing valuable insight,

including:

Kaaren Hall, uDirect IRA Services, LLC

Hector Padilla, HP Capital Investments

Christopher Meza, Real Titan Acquisitions

Paul Finck, The Maverick Millionaire

Rusty Tweed, TFS Properties

Barry Duron, AltLender Mortgage

Jeremy Rubin, The Friendly Flipper

Kris Miller, Legacy Wealth Strategies

Deborah Razo, Women’s Real Estate Network

Julie Harrison, Buy Direct Mississippi

Emily Nesselroad, 3 Fives Properties

Paul Wilkins, Approved Inheritance Cash

Jim Edenfield, Invest Success

Tim Emery, The Great Mile High Real Estate Investors Summit

AND MANY MORE!

article continues after advertisement

Be sure to join us IN PERSON. We will have wonderful resources, plus guests will have access to private capital, and business and commercial funding as well. We have investors joining us from across the nation for one day of networking.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/Irvine-Wealth-Summit.png4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-07 02:49:332023-08-16 01:26:35LEARN FROM SOPHISTICATED NATIONAL INVESTORS JOINING US IN SOUTHERN CALIFORNIA

New modern new home community in Michigan features stunning architectural and interior design

ANN ARBOR, Mich., Aug. 02, 2023 (GLOBE NEWSWIRE) — Toll Brothers, Inc. (NYSE:TOL), the nation’s leading builder of luxury homes, today announced the grand opening of its model home at Concord Pines of Ann Arbor, a new single-family community of luxury homes in a wooded enclave just minutes from downtown Ann Arbor, Michigan. A limited number of home sites remain available at the community, as well as quick move-in homes that will be ready for delivery in early 2024.

ADVERTISEMENT

The highly anticipated Buckley Modern Farmhouse model home features innovative architecture complemented by stunning interior design and merchandising, showcasing the perfect blend of luxury and modern contemporary design. Toll Brothers architecture is unmatched in the area, with homes in Concord Pines featuring open-concept single-story ranch or two-story floor plans ranging from 2,300 to 3,500 square feet and 3 to 6 bedrooms. Homeowners will enjoy well-appointed gourmet kitchens, luxury primary bedroom suites, convenient bedroom-level laundry rooms, private home offices, first-floor guest suite additions, and much more.

“Our Concord Pines of Ann Arbor community is now offering the final opportunities for our luxury single-family home designs in a prime Ann Arbor location,” said Isaac Boyd, Division President of Toll Brothers in Michigan. “The newly opened model home serves as an inspiration for our home buyers who are looking to create just the right space for their family to call home.”

The community is located in the top-rated Ann Arbor School district and next to the acclaimed Greenhills School. The central location provides residents with high-end shopping, dining, and entertainment opportunities in Downtown Ann Arbor, as well as numerous recreational options including hiking, biking, and golf. This community is also a short drive to the University of Michigan campus and medical center.

Concord Pines of Ann Arbor has experienced tremendous interest from new home buyers. Only six to-be-built home sites remain in which home buyers can choose their home design, and three quick move-in homes already under construction are available for sale with delivery dates in early 2024.

Home prices start in the low $800,000s.

For more information and to schedule an appointment to visit Concord Pines and tour the new Toll Brothers model home, call 866-267-0537 or visit ConcordPines.com.

ADVERTISEMENT

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/CONCORD-PINES.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-04 02:56:492023-08-04 02:56:53Toll Brothers Model Home Opens in Concord Pines of Ann Arbor Luxury Home Community

Number of existing homes bought by international buyers declined to 84,600 – the fewest since 2009

Washington, D.C., Aug. 01, 2023 (GLOBE NEWSWIRE) —

Key Highlights

International buyers purchased $53.3 billion worth of U.S. residential properties from April 2022 to March 2023, down 9.6% from the previous year. The 84,600 existing homes sold – the lowest since NAR began tracking in 2009 – retreated 14.2% from the prior year.

The average ($639,900) and median ($396,400) purchase prices for international buyers were the highest ever recorded by NAR.

China, Mexico, Canada, India and Colombia were the top five countries of origin by number of U.S. existing homes purchased. The top U.S. destinations for foreign buyers were Florida (23%); California and Texas (12% each); and North Carolina, Arizona and Illinois (4% each).

ADVERTISEMENT

Foreign buyers purchased $53.3 billion worth of U.S. existing homes from April 2022 through March 2023, slipping 9.6% from the previous 12-month period, according to a new report from the National Association of Realtors®. Foreign buyers purchased 84,600 properties, down 14.2% from the prior year and the fewest number of homes bought since 2009, when NAR began tracking this data. Overall, U.S. existing-home sales totaled 5.03 million in 2022, down 17.8% from 2021.

“Sharply lower housing inventory in the U.S. and higher borrowing costs across the world have dented international buyers for two straight years,” said NAR Chief Economist Lawrence Yun. “However, recovering international travel following the end of the pandemic will bring more foreign transactions in coming months and years.”

NAR’s 2023 International Transactions in U.S. Residential Real Estate report surveyed members about transactions with international clients who purchased and sold U.S. residential property from April 2022 through March 2023. Foreign buyers who resided in the U.S. as recent immigrants or who were holding visas that allowed them to live in the U.S. purchased $23.4 billion worth of U.S. existing homes, a 31.4% decrease from the prior year and representing 44% of the dollar volume of purchases. Foreign buyers who lived abroad purchased $29.9 billion worth of existing homes, up 20% from the 12 months prior and accounting for 56% of the dollar volume. International buyers accounted for 2.3% of the $2.3 trillion in existing-home sales during that period.

The average ($639,900) and median ($396,400) existing-home sales prices among international buyers were the highest ever recorded by NAR – and 7% and 8.3% higher, respectively, than the previous year. The increase in prices for foreign buyers reflects the increase in U.S. home prices, as the median sales price for all U.S. existing homes was $384,200. At $1.23 million, Chinese buyers had the highest average purchase price, with a third – 33% – purchasing property in California. In total, 15% percent of foreign buyers purchased properties worth more than $1 million from April 2022 to March 2023.

China and Canada remained first and second in U.S. residential sales dollar volume at $13.6 billion and $6.6 billion, respectively, continuing a trend going back to 2013. Mexico ($4.2 billion), India ($3.4 billion) and Colombia ($0.9 billion) rounded out the top five.

“Home purchases from Chinese buyers increased after China relaxed the world’s strictest pandemic lockdown policy, while buyers from India were helped by the country’s strong GDP growth,” Yun added. “A stronger Mexican peso against the U.S. dollar likely contributed to the rise in sales from Mexican buyers.”

For the 15th consecutive year, Florida remained the top destination for foreign buyers, accounting for 23% of all international purchases. California and Texas tied for second (12% each), followed by North Carolina, Arizona and Illinois (4% each).

ADVERTISEMENT

“Florida, Texas and Arizona continue to attract foreign buyers despite the hot weather conditions during the summer and the significant spike in home prices that began a few years ago,” Yun said.

All-cash sales accounted for 42% of international buyer transactions compared to 26% of all existing-home buyers. Non-resident foreign buyers (52%) were more likely to make an all-cash purchase than resident foreign buyers (32%). Two-thirds of Colombian buyers (67%) made all-cash purchases, the highest share among the top five foreign buyer nations. Approximately half of Canadian (51%) and Chinese (47%) buyers made all-cash purchases. Asian Indian buyers were the least likely to pay all cash, at just 15%.

Half of foreign buyers purchased their property for use as a vacation home, rental property, or both – up from 44% the previous year. Almost three out of five international buyers (59%) purchased detached, single-family homes.

“Fostering economic investment in culturally dynamic communities, businesses, and industry is a top priority for NAR,” said Charlie Dawson, NAR’s vice president of engagement and advocacy outreach. “Our work across the country provides members and their communities with tools, resources and data to identify and highlight international investment opportunities in U.S. real estate. This acts as a key pillar in our efforts to further support local communities to drive economic development in markets across the country. NAR and the Realtor® brand has developed a network of partnerships with over 100 real estate organizations across 77 countries providing growth opportunities by ensuring ethical and accessible markets that allow our members to make direct connections with global real estate professionals and international investors.”

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/FOREIGN-INVESTMENT.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-03 04:26:022023-08-03 04:26:09Annual Foreign Investment in U.S. Existing-Home Sales Declined 9.6% to $53.3 Billion

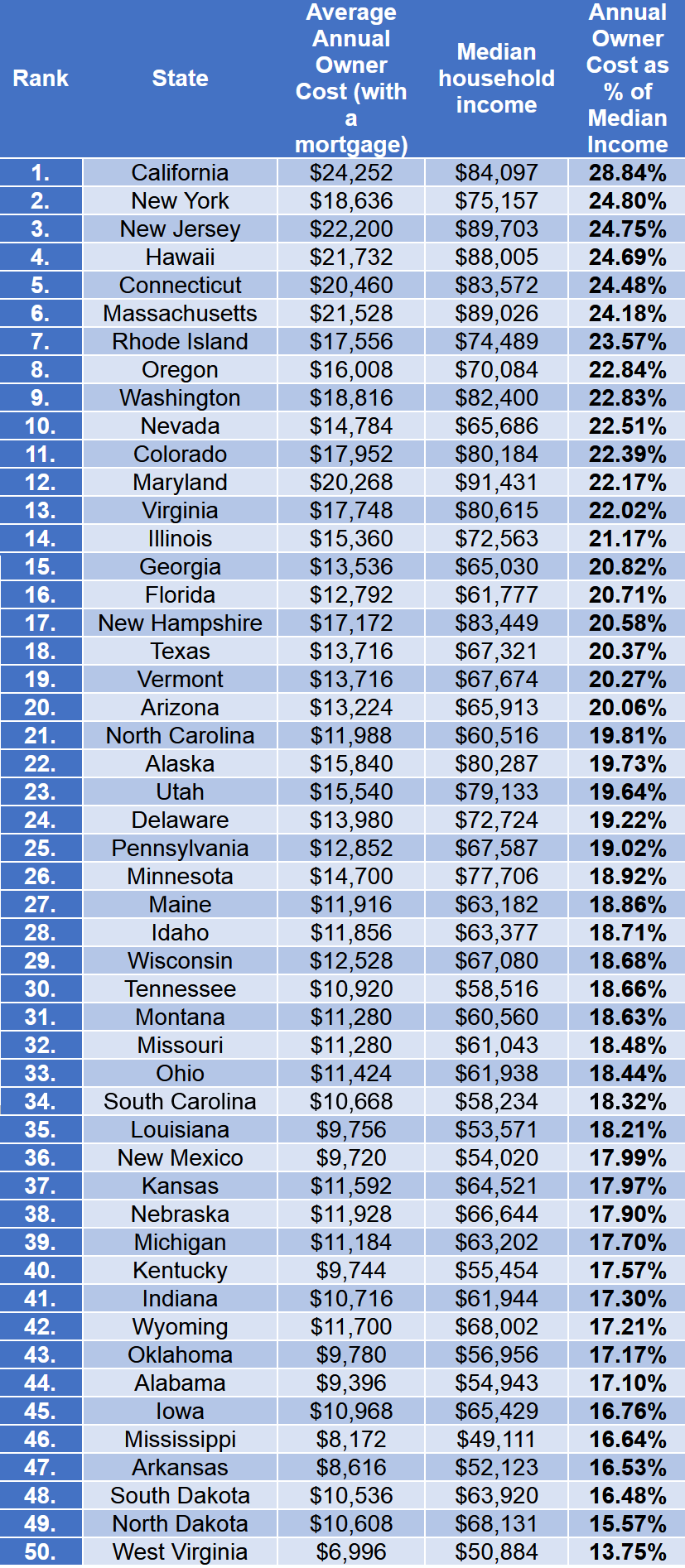

A new study has revealed that California residents spend the most income on housing costs.

Real estate website NewJerseyRealEstateNetwork.com analyzed census data to find the average yearly housing cost in each state as a proportion of median income, to uncover which state costs the most to own a home.

Housing costs included mortgage repayments, various insurances, property taxes, utility bills, fuel bills, mobile home costs, and condominium fees.

California is the state where homeowners spend the largest percentage of their income on housing costs. The average annual cost for a homeowner with a mortgage in California is $24,252, which is 28.84% of the state median income of $84,097.

New York homeowners are the second biggest spenders in terms of housing costs. The average homeowner pays $18,636 per year on housing costs, which is 24.8% of the state median income of $75,157.

New Jersey homeowners are the third biggest spenders when it comes to housing costs. The average cost to the homeowner was $22,200 per year, which is 24.75% of the state median income of $89,703.

Hawaii ranks fourth for states where homeowners are spending the largest proportion of their income on housing costs. The average cost for a homeowner in Hawaii is $21,732 per year, which is 24.69% of the state’s median income of $88,005.

With an average annual cost to the homeowner of $20,460, which is 24.48% of the state median income of $83,572, Connecticut is fifth for the state where homeowners are spending the largest proportion of their income on housing costs.

Massachusetts comes sixth and Rhode Island comes seventh for the state where homeowners are spending the largest proportion of their income on housing costs. Massachusetts homeowners spend 24.18% of the state’s median income on housing costs, while Rhode Island homeowners spend 23.57% on housing costs.

Rounding out the top ten is Oregon in eighth, Washington in ninth, and Nevada in tenth. Homeowners in each of these states spend 22.84%, 22.83%, and 22.51% of their income on housing costs respectively.

West Virginia is the state where it costs the least to be a homeowner, with homeowners spending just $6,996 per year on housing costs, which is only 13.75% of the state’s median income of $50,884.

Table showing the average annual cost to homeowners compared to median household income

“California is known for relatively higher housing costs, yet it is still surprising to see how much higher the costs to the homeowner are in the state compared to the rest of America. The homeowners of the next closest state, New York, spend 15.1% less on average than homeowners in California, when accounting for differences in household income.

It will be particularly interesting to see how the rising cost of living impacts these figures and whether California’s cost to the homeowner continues to remain so high compared to the rest of America.

ADVERTISEMENT

Sources: (via Census Business Builder): 2021 American Community Survey 5-year Summary File, 2016 American Community Survey 5-year Summary File, 2021 American Community Survey 5-year Data Profile

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/Hawaii.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-02 01:43:102023-08-02 02:05:05Hawaii Homeowners Spend the Fourth Most on Housing Costs on Average

The Los Angeles home where Walt Disney lived and worked on some of his most important movies such as Snow White, Cinderella, and Pinocchio is for rent at $40,000 per month. Walt and family lived in the home from 1932 to 1950.

Mick Jagger’s Florida Home For Sale

Mick Jagger and girlfriend Melanie Hamrick have listed their Florida home for sale at $3.49 million. Jagger bought the four-bedroom lakefront home near Sarasota in 2020 for $1.98 million.

ADVERTISEMENT

James Corden Sells LA Home Before US Exit

Heading back to his native UK, James Corden has sold his LA home for $17.1 million. Originally listed at $22 million, James had to lower the price for the seven-bedroom home for several reasons, including a slow real estate market and the new LA luxury homes tax. James will be doing several new projects in England, including building a new home in Oxfordshire – near London.

Johnny Depp Saves Hollywood Hills Homes

Johnny Depp has owned an eclectic collection of real estate, including his five LA penthouses that he sold a few years ago and an entire French village. He just saved two of his West Hollywood Hills homes from foreclosure after taking out a $10 million loan.

Photo credit:Daniel Dahler for Sotheby’s International Realty

Jim Carrey’s LA Mansion

In 2022, Jim Carrey announced that he was taking a break from acting and was considering retirement. The prolific star has relocated to his vacation property in Hawaii and put the Los Angeles home where he has lived for the last 30 years up for sale. The 12,700-square-foot home is listed for $26.5 million.

John Fogerty’s California Contemporary

John Fogerty is a fortunate son: the owner of a beautiful 18,600-square-foot California contemporary home with ocean and mountain views. John is one of the world’s most popular musicians and longtime leader of Creedence Clearwater Revival. The home is for sale at $19.95 million.

Photo credit: Michael MacNamara and Jason Speth

Rihanna Buys One LA Home – Lists Another One

Rihanna recently made celebrity real estate news when she bought Matthew Perry’s former Los Angeles penthouse for $21 million. Now she is selling one of two side-by-side homes in Beverly Hills that she bought in 2020 and 2021. The Tudor-style, 5,100-square-foot home is listed at $10.5 million.

Promises Malibu For Sale

Three Malibu properties, formerly the world-renowned Promises Malibu, have gone on the market. Frequented by A-listers for many decades, the longtime celebrity-rehab clinic on over three acres includes ocean views, a tennis court, a salt water pool and three single family homes totaling over 9,300 square feet. The asking price is $19.95 million.

ADVERTISEMENT

Kevin James Sells Another Florida Mansion

Comedian Kevin James has sold his latest Florida home – this one for $12.7 million. The home includes six bedrooms and seven bathrooms plus a game room and wine cellar. The star of The King of Queens has bought and sold several homes in Delray; he sold a similar home in 2016 for $26.4 million.

Rosie O’Donnell Lists Her Manhattan Penthouse

Rosie O’Donnell has listed her Midtown Manhattan penthouse for $8.3 million. With 3,600 square feet and postcard views of the Empire State Building and the East River, the apartment has just about everything a New York home buyer could want, including four bedrooms, a private rooftop terrace, professional sound system, and a 70-bottle wine refrigerator.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/WDISNEY-HOME.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-01 04:49:392023-08-01 04:49:43July’s Top 10 Celebrity Real Estate News: Walt Disney, Mick Jagger & James Corden

SACRAMENTO – In the wake of a recent statewide consumer alert on identity theft and rental properties, the California Department of Real Estate (DRE) is once again sounding the alarm. This time, the focus is on an emerging false identity scam targeting vacant land and unencumbered properties. With a surge in real estate fraud involving identity theft, law enforcement agencies and District Attorney’s offices across California are urging more than 434,000 DRE licensees to stay vigilant.

ADVERTISEMENT

The scam entails fraudsters scouring public records to identify properties without mortgages or liens, especially vacant lots, long-term rentals, or vacation homes often owned by vulnerable populations such as the elderly and foreigners.

Posing as the property owners, the criminals contact real estate agents, seeking assistance in selling the properties that they do not actually own. They lure agents with offers to list the properties below market value to generate quick interest, while ensuring no “For Sale” signs are displayed. They prefer cash buyers, demand rapid closing, and evade in-person meetings by relying on email, text, and phone communications, refusing video calls. To add another layer of deceit, they employ their own notary, who provides falsified documents to title companies or closing attorneys, insisting that proceeds be wired directly to them.

Detecting this scheme can be challenging, but real estate agents must exercise due diligence by verifying the property owner’s identity before accepting a listing. To protect themselves and their clients, agents are advised to:

1. Request in-person or virtual meetings with proper government-issued identification.

2. If an in-person meeting is not possible, require the use of a third-party identity verification service.

3. Conduct thorough online searches to verify the owner’s identity, including checking for recent photos and contact information.

4. Send a copy of the electronically signed listing via overnight mail to the property’s address on record, asking for confirmation from the actual owner.

5. Obtain a copy of a voided check with the seller’s disbursement authorization form from the property owner.

6. Use a wire verification service to ensure that wire instructions match the account details provided on the seller’s disbursement authorization form.

ADVERTISEMENT

DRE strongly encourages brokers to establish written policies regarding listings for properties where the licensee and seller have never met in person.

Should any suspicious real estate fraud cases arise, agents are urged to report them to local law enforcement or their District Attorney’s office. If another real estate licensee is potentially involved in the fraud, the information should be provided to DRE through its Enforcement Online Complaint System.

Vigilance and proactive measures can help thwart these scams and protect both real estate professionals and property owners from falling victim to such deceptive practices.

Stephanie Mojica

Stephanie Mojica, writer of How One Writer Shifted From Settling for $12 an Hour to Prospering at Over $90 an Hour and shorter books such as Quick Answers to Frequently Asked Credit Questions, is an award-winning journalist with publications such as USA Today, The Philadelphia Inquirer, San Francisco Chronicle, and The Virginian-Pilot, among many others. She helps executive coaches, business consultants, business owners, attorneys, and other decision makers generate more money online and become the go-to expert in their field by guiding them step by step through the process of writing and publishing a book.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/07/SCAM-ALERT.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-07-31 02:44:342023-08-02 03:53:24Beware: Unmasking the Vacant Land Property Scam — A Call to Vigilance for Real Estate Licensees

(New Jersey, July 25, 2023) – Stratton Equities, the Leading Nationwide Private Money and NON-QM Mortgage Lender, proudly celebrates its fifth anniversary. Since its launch in 2018, Stratton Equities has experienced significant growth and expanded its operations. The company has successfully established itself as a prominent player in the real estate investment and lending industry under the visionary leadership of its Founder and CEO, Michael Mikhail.

Mikhail encountered numerous challenges on his path to becoming a prominent figure in the industry. Following a five-year journey spanning 19 countries, he returned to the United States in 2017, homeless and without financial resources. However, his unwavering determination to reshape his future propelled him forward as he drew upon his extensive background in mortgage lending from 2003 to 2010. He deliberately leveraged that experience and explored opportunities within the mortgage lending industry. He faced numerous obstacles, including a lack of managerial support, limited program options, a shortage of leads, inadequate training or technology, and unhealthy work culture. This toxic environment was an industry-wide issue, contributing to a high turnover rate and low production among loan officers.

Stratton Equities was born as a response to these challenges. Mikhail’s vision was to overhaul the methods used by the mortgage lending industry by incorporating more programs and generating an influx of organic inbound leads. Mikhail achieved remarkable success, making $1.3 million within six months of launching the company.

ADVERTISEMENT

Due to Mikhail’s unwavering dedication to delivering exceptional service and driving success, Stratton Equities is a leading player in the private money and NON-QM mortgage lending industry. With its customer-first approach, state-of-the-art technology, and extensive expertise, Stratton Equities has expanded its market reach and aims to achieve an impressive target of $1.2 billion in closed loan volume annually, or $100 million monthly.

Reflecting on the milestone, Mikhail commented, “As we celebrate, I am humbled and grateful for the incredible journey we have embarked upon. It has been a testament to our unwavering commitment, relentless dedication, and the trust our clients and partners place in us. This milestone is a celebration of our accomplishments and a reflection of the transformative power of perseverance and innovation in the lending industry. We have expanded our reach, refined our strategies, and surpassed expectations each year. As we look back on our journey, we are energized by the opportunities that lie ahead. Together, we will continue to shape the future of real estate financing and empower dreams. This is only the beginning, and the best is yet to come.”

One of the many successes that Mikhail created for Stratton Equities is the unique programs, lead generation model, and loan portfolio milestones. Mikhail has revolutionized lead generation and digital marketing with his innovative platform at Stratton Equities. Unlike traditional private money lenders relying on loan officers to hunt for leads through cold calls and networking, Mikhail’s system brings leads to the company daily, eliminating manual prospecting. This powerful tool generates an abundance of organic leads, surpassing the strategies of other private money-lending companies and propelling the company’s performance while enabling aggressive hiring.

Moreover, Mikhail’s platform provides loan officers with access to the largest collection of nationwide private money and NON-QM mortgage loan programs. This comprehensive offering allows them to effectively cater to the needs of real estate investors, entrepreneurs, and diverse mortgage borrowers.

Stratton Equities has received recognition within the industry for its exceptional services and expertise, as well as for Mikhail’s success. In 2021, Forbes Magazine included Mikhail in their “The Next 1000” list, celebrating individuals redefining what it means to build and run businesses today. NJBIZ, New Jersey’s leading business journal, also recognized Stratton Equities as one of the Top 250 Privately Held Companies for 2021. They further honored Mikhail as one of their 2022 Leaders in Finance, and he was nominated for the prestigious Ernst & Young Entrepreneur of the Year program.

Stratton Equities consistently achieves high levels of customer satisfaction. Through its commitment to providing personalized solutions and exceptional customer service, the company has built a strong reputation for its client-centric approach. Many clients have praised Stratton Equities for its outstanding service, professionalism, and ability to secure funding quickly. One client, John S., commended the company for its efficient processing and dedication to finding the best loan options, expressing gratitude for their personalized approach that ensured his unique needs were met. Another client, Sarah L., emphasized the team’s expertise in navigating complex financial situations, stating that Stratton Equities provided her with the guidance and support needed to secure a loan for her real estate investment. These testimonials and many more highlight the company’s commitment to client satisfaction and its track record of delivering outstanding results.

In addition to client testimonials, Stratton Equities has received positive feedback on reputable platforms such as Indeed and Glassdoor. Several employees have shared their experiences working for the company, consistently praising the supportive and collaborative work environment and highlighting the company’s dedication to fostering professional growth and providing ample opportunities for career advancement. Employees also speak highly of the company’s management, describing them as knowledgeable, approachable, and committed to the team’s and clients’ success. This positive employee feedback further supports the notion that Stratton Equities excels in serving its clients and maintains a workplace culture that values and nurtures its employees.

Mikhail’s visionary leadership and persistent commitment have solidified Stratton Equities’ position as a trusted and innovative company with high expertise, cutting-edge technology, and a customer-centric approach.

Michael Mikhail is the Founder and CEO of Stratton Equities, the nation’s leading hard money-lender to national real estate investors, with the largest variety of mortgage loans and programs nationwide.

Having launched Stratton Equities in early 2017, Michael has always been an entrepreneur and innovator in the real estate market, purchasing his first home at 19.

A serial entrepreneur with a foresight for business opportunities, Michael had a slew of small businesses prior to launching Stratton Equities. One of his most prolific ventures was a car wash connected to a gym he was affiliated with in Florida during 2001-2002 while attending college.

It wasn’t until he graduated from Florida State University with a degree in Business, that he officially joined the mortgage industry in 2003 and decided to travel to explore his options globally.

After travelling to 19 countries in 5 years, Michael knew two things; he wanted to start his own business and launch it in the United States. He knew that moving back to the states was the best place he could start something small and grow it into something infinite.

In 2017, Michael noticed how the mortgage industry had transformed after the regulations presented from 2008-2012, and knew it was time to set out something on his own, thus creating Stratton Equities.

Under Michael’s leadership, Stratton Equities has grown into one of the biggest leaders in the Mortgage and Real Estate industry across genres and platforms.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/07/celebration-cakes.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-07-28 04:24:592023-07-28 04:25:04From Homelessness to Multi-Millionaire: Michael Mikhail Leads Stratton Equities in Celebrating 5 Years of Success and Achievement

Where: The Curtis Hotel Denver Colorado When: March 8-10th 2024

The Great Mile High Real Estate Investors Summit is the first of its kind. This multi- day event will start at the unique Curtis Hotel in downtown Denver and end with a ski trip to the mountains.

From the leaders of Invest Success and The John Fisher Breakfast Club, join Dave Seymour from hit TV show, “Flipping Boston” and learn from successful investors and seasoned educators. Confirmed speakers Kevin Amolsch with Pine Financial, Tim Emery with Invest Success, Joe Massey with Castle & Cooke Mortgage, and Joseph Scorese with BRRRR Loans, just to name a few. Many more speakers to be announced from across the country and will be ready to share their valuable insights!

Investors of all levels are welcome. Attendees will have access to resources like private capital, business and commercial funding. Now is the time to grow your real estate business to new levels. Come build your network!

This is not your ordinary real estate investor summit. Enjoy educational and networking opportunities, happy hours, dinners, entertainment and a property bus tour around Denver. Stay to hit the slopes and enjoy all that beautiful Colorado has to offer!

Discount hotel rates available at The Curtis Hotel Downtown Denver.

If you would like to promote your business during the event as a Speaker, Vendor, or Sponsor, email [email protected]. PR/ Marketing Contact: Vanessa Edgett Email: [email protected]

Sponsors:

Invest Success

Realty 411

BRRRR Loans

Elevate Title

Pine Financial

Real Estate Investors Group (RIG)

More sponsors to be announced soon!

About The Great Mile High Real Estate Investors Summit

The Great Mile High Real Estate Investors Summit’s goal is to create unique educational and networking opportunities for investors at all levels. We believe in the power of connecting with people in person, and having fun!

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/07/The-Great-Mile-High.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-07-27 05:43:182023-07-27 05:43:22The Great Mile High Real Estate Investors Summit is Coming to Denver in 2024!