PARSIPPANY, N.J.–(BUSINESS WIRE)–In an ever-evolving mortgage lending landscape, NON-QM mortgage loans are emerging as the industry’s future, providing opportunities for a wider range of borrowers to achieve their homeownership and investment goals. Stratton Equities, the Leading Nationwide Private Money and NON-QM Mortgage Lender, has been at the forefront of this revolution for the past six years, setting the pace for other companies to follow.

NON-QM mortgage loans, short for non-qualified mortgage loans, have gained significant traction in recent years as a viable alternative to traditional QM (qualified mortgage) mortgage loans, which come with stringent government regulations and eligibility criteria. Recent statistics reveal that only a small percentage of Americans qualify for QM loans due to these stringent requirements.

article continues after advertisement

According to industry data, the demand for NON-QM mortgage loans has steadily increased yearly, with a notable surge in the past few years. In 2022 alone, NON-QM loans accounted for a significant portion of the mortgage market, surpassing expectations. It has been estimated that one in four loans will go NON-QM in the near future.

Stratton Equities recognized the potential of NON-QM loans six years ago, positioning themselves as pioneers in private money lending, specifically NON-QM mortgage loans. This early recognition of market trends has been the cornerstone of their continued success.

Michael Mikhail, CEO and Founder of Stratton Equities, emphasized their focus on generating NON-QM leads and their commitment to offering a wide range of lending programs, including NON-QM, DSCR, Hard Money, and No-Doc Loans. He stated, “Our aim has always been to provide solutions that cater to a broader spectrum of borrowers. Stratton Equities had the foresight six years ago to recognize the market’s direction, which is why we were at the forefront of NON-QM mortgage lending. This serves as a foundation for our continued success.”

NON-QM mortgage loans are designed to serve most Americans who do not meet the strict eligibility criteria of QM loans. These loans facilitate home ownership, second home ownership, and investment properties, allowing income generation and wealth building for a more diverse range of borrowers. Contrary to misconceptions, NON-QM mortgage loans often offer competitive rates, making them attractive.

article continues after advertisement

Traditional lenders like banks and credit unions primarily offer QM loans for one-to-four-family investment properties. However, these loans have heavy documentation requirements and lower loan-to-value (LTV) ratios, typically capping at 70%. Stratton Equities stands out by providing NON-QM mortgage loans for such properties with easier qualifications, lower documentation requirements, and higher LTV ratios, currently at 80%.

Stratton Equities also recommends closing within an LLC for investment properties due to tax and security advantages. Despite some lingering stigma associated with NON-QM mortgage loans, they often result in lower rates, higher LTVs, and streamlined documentation, making them a practical choice for borrowers.

Educating borrowers about the advantages of NON-QM mortgage loans and dispelling misconceptions is vital. Stratton Equities is committed to leading the way in providing these beneficial lending options and believes in the potential for growth and success in this market. Their loan officers benefit from the advantages offered by the company, including a consistent stream of leads, as exemplified by recent hires who have quickly achieved success within the organization.

Stratton Equities invites individuals and investors to explore the world of NON-QM mortgage loans and discover the possibilities for achieving their financial goals. For more information, please visit www.strattonequities.com.

Contacts Kelly Bennett, Director of PR Stratton Equities [email protected] (949) 463-6383

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/02/futureloading.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-02-01 00:37:082024-02-01 00:37:10Stratton Equities: Pioneering the Future of NON-QM Mortgages

This is an incredible opportunity for skilled professionals who want to work with a company that guarantees abundant direct organic daily leads, hands-on management training and support, niche mortgage loan programs with competitive pricing, and advanced mortgage technology.

Mortgage Loan Officers can expect to close their first loan within four to six weeks after the completion of their initial training.

Mortgage Loan Officers who join the Stratton Equities team can expect the following:

Competitive compensation: Stratton Equities offers a highly competitive compensation plan, potentially allowing Mortgage Loan Officers to earn their first year $110,086.26 – $190,677.36.

Strong resources: Stratton Equities’ interest rates are some of the lowest nationwide in private lending, starting at 6.75%, and can pre-approve a loan in 24 hours.

Room for growth: As a rapidly growing company, Stratton Equities offers ample opportunities for advancement and career growth. With a focus on promoting from within, Mortgage Loan Officers who join the team will have the chance to take on new challenges and responsibilities as they progress in their careers.

A dynamic work environment: At Stratton Equities, Mortgage Loan Officers will work in a fast-paced, dynamic environment focused on innovation and results. As a part of the loan officer team, you can work directly with prospective real estate investors, entrepreneurs, and borrowers on their real estate endeavors.

If you are an experienced Mortgage Loan Officer looking for an exciting new opportunity to grow your career or a licensed Mortgage Loan Originator that is new to the industry and needs help finding business, then Stratton Equities is the place for you to earn a great income.

This is an incredible opportunity to join a leading nationwide mortgage lender and build a bright future with a company that values its employees and their contributions.

Contacts For media inquiries and interviews, please contact Kelly Bennett of Bennett Unlimited PR at [email protected].

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/01/we-are-hiring.jpg5001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-01-15 01:15:142024-01-15 01:15:16Stratton Equities is Hiring Mortgage Loan Officers to Join Their Dynamic New Jersey Team and Build a Lucrative Career in the Mortgage Industry

Real estate lending encompasses both real estate and securities laws.

A) Deeds of trust and mortgage instruments are securities:

Promissory notes secured by deeds of trust or mortgages are security instruments. These contracts represent evidence of indebtedness. Ownership is a security under the Federal Securities Act of 1933.

The definition of security under federal law is as follows:

a) Property given or pledged to guarantee the performance of an obligation. b) An instrument that functions as proof of a security interest in a public or private body.

article continues after advertisement

Parties in a loan transaction:

Borrowers and private-party lenders are the principals in a transaction. A borrower will sign a promise to pay called a promissory note and the security instrument called a deed of trust. The deed of trust is an instrument recorded at the county recorder’s office, which becomes a matter of public notice of the charging lien against the property.

The note and deed of trust are contracts between the borrower and private-party lenders. After the loan closing, the investors/lenders, or the servicing agents of the investors, will retain the executed and recorded documents as evidence of the investment.

Promissory notes and deeds of trust (or mortgages) are considered personal rather than real property.

B) Deeds of trust and mortgage investments are securities requiring federal or state registrations unless there are applicable exemptions from registration.

Each state in the U.S. has its own securities laws and regulations. State statutes, known as Blue Sky laws, are designed to establish safeguards against fraud for investors. Each state passed separate securities laws to protect the public from fraudulent schemes as far back as 1911 in Kansas. The term “blue sky law” originated in the early 1900s, gaining widespread use when a Kansas Supreme Court justice declared his desire to protect investors from speculative ventures that had “no more basis than so many feet of ‘blue sky.’”

What does securities registration mean?

Registration occurs when a company files the required documents with the Securities and Exchange Commission (SEC). The extensive process involves approving disclosures and other information related to the offering. There will usually be quarterly and annual reporting requirements.

Unregistered securities have fewer protections than registered securities. Companies can only sell unregistered shares to a limited number of qualified or high-income and high-net-worth investors.

Securities overview:

Federal and state securities exemptions from registration are common and available.

Federal Exemptions:

Federal exemptions for privately funded loan transactions and loan pooled investors are referenced in Regulation D, Rule 506 section 4(a)(2), and 506(b), Regulation A, and Rules 147 and 147A. Information about these regulations can be found at:

Definitions and exemptions are on the www.sec.gov website.

article continues after advertisement

State securities exemptions:

Each state has its own securities laws and exemptions.

I am using California as an example because that is my state of origin. However, those involved with loans and investors in other states should identify their dominion’s relevant state securities statutes.

California Corporate Codes relating to securities are 25000-31516

California Corporate Securities Law of 1968 regulates all offerings and sales of securities in California. All securities offered or sold must be qualified by the Department of Financial Protection and Innovation Commissioner or exempted from qualification and registration by a specific law or corporate rule. Securities references include 10CCR, Chapter 3, Sections 260.115 and 260.204.1, California Corporate Securities rules 25206, 25100 (p), 25102, (e) (f) (n), and 25102.5 which refers to the multi-lender rules.

a) 25100 (p), is referred to as a whole note exemption, one note purchased by one party

(p) This is a promissory note secured by a lien on real property which is neither a series of notes of equal priority secured by interests in the same real property nor a note in which beneficial interests are sold to more than one person or entity.

b) 25102 for state offerings exemption

c) 25102 (e)

Under Section 25102 (e, f,), an exemption from the qualification requirement for issuer transactions is available for any offer of sale of evidence of indebtedness, a partnership, a joint venture, and certain participating interest in railroad rolling stock, or other equipment, if the transaction does not involve a public offering.

California state exemptions for fractional trust deeds are 25102(e), 25102(f), and 25102.5, which cover multiple investors who invest in real estate loan transactions. 25102(e) and 25102.5 allow a maximum of 10 investors. Both exemptions, 25102 (e) and 25102.5 contemplate lending on California properties with California-based investors. Family members are considered as one in the same household.

d) 25102.5is referred to as the fractional note exemption.

California rules are promulgated in the Business & Professions Code 10237-10238, 10232.3, 10232.4, 10232.5, Civil Code 2941.9, and many others.

Under the 25102 (e) and 25102.5 exemptions, ten private investors can co-invest into a single trust deed as tenants-in-common. The difference between 25102 (e) and 25102.5 is that “e” requires disclosure documents in the form of an offering circular, subscription agreements, and a suitability questionnaire. 25102.5 provides a framework for suitability and investor disclosures within 10237-10238 of the Business & Professions code. Interested parties should consult a real estate or securities lawyer specialist

e) 25102(f) private offering exemption.

The Corporations code sets forth an exemption from the qualification requirement for transactions where (1) the sale is to 35 or fewer persons, (2) each purchaser has a preexisting relationship with the securities issuer, (3) each purchaser represents the purchase is for the person’s own account, (4) the offer or sale is not accomplished through advertising, and (5) the issuer files a notice with the Department of Corporations, within 15 dates from of the issuance. Corporate commissioner’s rule 260.102.14 provides instructions for filing the notice and paying a fee. Failure to file the notice on time negates the exemption.

25102 (f) allows up to 35 investors, with conditions. 25102 (f) does not require California investors or California properties for a particular loan request. Discuss with counsel.

There are three instances when a 25102 (f) exemption may be helpful. (1) when a trust deed requires more than ten investors, (2) when an occasional (accredited investor) out of state party invests in a trust deed on a California property, (3) when a California real estate lender makes a loan on an out of state property.

(f) 25113 provides a path to eligibility for qualification by a permit process. An issuer may apply for a permit to operate under this section and provide the accompanying documentation as required by the commissioner. These permits are usually renewable annually. Caution: Applying appropriate securities exemptions and actions to remain in regulatory compliance is most likely accomplished by consultation with a qualified securities attorney. The above is a general but not all-inclusive overview of securities compliance.

2) California Corporate Commissioners rule 25206.

A broker licensed by the Real Estate Commissioner is exempt from the provisionsof Section 25210(broker-dealers) when engaged in transactions in any interest in any general or limited partnership, joint venture, unincorporated association, or similar organization (but not a corporation) owned beneficially by no more than 100 persons and formed for the sole purpose of, and engaged solely in, investment in or gain from an interest in real property, including, but not limited to a sale, exchange, trade, or development. An interest held by a husband and wife shall be owned by one person for this section.

article continues after advertisement

3) California Code of Regulations, Section 260.204.1

An exemption from the provisions of Section 25210 of the Code is hereby granted, as is necessary and appropriate in the public interest and for the protection of investors, to any person who is a real estate broker as defined in Section 10131of the Business and Professions Code, duly licensed to engage in the business of a real estate broker in this state, and whose business as a broker-dealer, in addition to any transactions within Section 25206 of the Code, is limited to any or all of the following:

(d) Transactions in a series of notes secured by interests

in the same real property, or undivided interests in a note secured by

real property, according to qualification under Section 25110,

Section 25120, or Section 25130

of the Code or according to the exemption contained in Section25102(e),

Section 25102(if) or Section 25102.5, other than an offering which is

made under a registration under the Securities Act of 1933 or a

Regulation

“A” exemption under that Act ( 17 CFR 230.231 et seq.).

California is highly regulated, with other laws passed and pending future legislative bills that diminish property ownership rights and lessen processionary benefits. Real property ownership rights and benefits continue to be eroded.

There are hundreds of code sections about licensing, fiduciary obligations, operation of real estate and mortgage companies, and disclosure requirements for both borrowers and trust deed investors. I omitted the abundantly extensive list of all the code sections because the number is significant. Therein lies the continuous employment of lending consultants, expert witnesses, real estate lawyers, and securities lawyers.

C) Disclosure requirements for trust deed Investors.

A California mortgage broker soliciting an investor to purchase all, or a fractional share of a trust deed must provide a lender/purchaser disclosure statement before taking funds.

A lender/purchaser, disclosure statement 851-C, revised 7/2018

Investor disclosures are in 10232.3 &10232.5 of the California Business and Professions Code.

Business and Professions Codes 10232.3 and 10232.5 outline the disclosure requirements the funding lender must adhere to for a real estate licensee. I am highly familiar with these requirements since I co-sponsored Senate Bill SB 1554 in 1998 and wrote a portion of the language that resulted in adopting the code.

The purpose is to provide the investors with written disclosures to make them aware of the material facts and risks and to enable them to make an informed investment decision.

Address or other means of identification of the real property that is to be the security for the borrower’s obligation.

Estimated fair market value

of the securing property as determined by an independent appraisal, a

copy provided to the lender. However, a lender may waive the

requirement of an independent assessment in writing on a case-by-case

basis, in which case, the real estate broker shall provide the broker’s

reported estimated fair market value of the securing property, which

shall include the objective data upon which the broker’s estimate is

based. A broker has the option of issuing

broker’s opinion of value.”

Age, size, type of construction, and a description of improvements to the property if contained in the appraisal or as represented to the broker by the prospective borrower.

Borrower(s) Identity, occupation, employment, income, and credit data as represented to the broker.

Terms of the loan transaction.

Liens and encumbrances:

pertinent information concerning all liens and encumbrances against the

securing property and, to the extent of actual knowledge of the broker,

relevant information about other loans that the borrower expects

or anticipates will result in a lien recorded against the collateral

property securing the promissory note, created in favor of the

prospective lender. As used in this paragraph, actual knowledge

concerning any anticipated loans means knowledge gained by

the broker through arranging the subject loan or other loans on behalf

of the borrower.

Title insurance: The broker

shall provide the prospective lender with the option to purchase a title

insurance policy or an endorsement of an existing title insurance

policy covering the securing property.

Written loan application (signed) loan application.

Credit report.

Loan servicing provisions: including disposition of the late charge and prepayment penalty fees paid by the borrower.

Industry standards and best practices may expand investor disclosures. Here are recommended guidelines on data accumulation.

Individuals/entities: The borrower may be one or

more individuals or an entity such as a family trust, limited liability

company, or corporation. The procuring loan broker should be able to

articulate who the borrower is and provide

a brief background.

Collateral property:

Describe the property and its uses, along with the address. Describe the

tenancy, income stream, and vacancy if the property is

income-producing. Describe the condition of the property and its

strengths and

weaknesses. Will the property be improved because of this loan?

Purpose of loan:

What is the intended use of the loan proceeds? What other debts are to

be paid as part of the loan? How much net proceeds will the borrower

receive? What will the net proceeds be used for? Will the majority of

the loan proceeds be used for consumer or business purposes?

Some lenders operate under a pooled limited liability format with a California Finance Lenders license. Others operate under a Bureau of Real Estate broker’s license. Some real estate brokers also create pools using one of the various federal and state securities exemptions. Three questions arise: (1) does the entity or the security issuer have a fiduciary obligation to the investors? (2) is the entity required to follow real estate law? (3) can the entity or issuer wave or disregard reasonable and prudent underwriting processes without violating fiduciary or breaking the law?

D) Private-party investors:

Private-party investors may invest by purchasing 100% of a loan, co-invest fractionally, with a small group as tenants-in-common, or in a pooled entity format with other investors. Private-party investors include individuals, family trusts, corporations, IRAs, and pension plans.

Most investors invest with multiple ownership methods (holding titles), such as a family trust for a portion and an IRA custodian for a portion. I have noticed various titles for couples who establish a family trust for themselves and their descendants and invest in each. Multiple family members living in the same home are considered one investor for ten investors or less.

The entire trust deed investment percentage represents the investor’s beneficial interest portion of ownership. For example, if the trust deed investment is for $1,000,000 and the investor purchased $200,000, they would own a 20% undivided interest as tenants-in-common. A $100,000 investor would hold a 10% undivided interest as tenants-in-common with other investors.

article continues after advertisement

Private-party Investors who desire to invest in trust deeds with their available capital understand that they are securing their investment by accepting a signed promissory note from a borrower, a signed and notarized recorded deed of trust on the security property. Investors’ names are affixed on a recorded trust deed as beneficiaries. Investors will also assume there is a title insurance policy with their names connected as beneficiaries.

Trust deed investments usually provide for receiving monthly interest payments from the borrower and are distributed to the investors. The annualized yields are comparatively reasonable. Investor distributions are generally a tiny fraction less due to being charged a servicing fee.

Interested parties should seek loan broker professionals who understand required regulatory compliance, best practices process & underwriting, and correct documentation. Lastly, interested parties should seek someone with an experienced track record as their agent and source of trust deed investments.

Thank You,

Dan Harkey.

Dan Harkey

Dan Harkey is a contributing author to Weekly Real Estate News and is a Business & Financial Consultant. He can be contacted at 949-533-8315 or [email protected].

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/mortgage-investments.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-25 01:04:382023-08-25 01:04:43Deed of Trusts and Mortgage Investments

(New Jersey, July 25, 2023) – Stratton Equities, the Leading Nationwide Private Money and NON-QM Mortgage Lender, proudly celebrates its fifth anniversary. Since its launch in 2018, Stratton Equities has experienced significant growth and expanded its operations. The company has successfully established itself as a prominent player in the real estate investment and lending industry under the visionary leadership of its Founder and CEO, Michael Mikhail.

Mikhail encountered numerous challenges on his path to becoming a prominent figure in the industry. Following a five-year journey spanning 19 countries, he returned to the United States in 2017, homeless and without financial resources. However, his unwavering determination to reshape his future propelled him forward as he drew upon his extensive background in mortgage lending from 2003 to 2010. He deliberately leveraged that experience and explored opportunities within the mortgage lending industry. He faced numerous obstacles, including a lack of managerial support, limited program options, a shortage of leads, inadequate training or technology, and unhealthy work culture. This toxic environment was an industry-wide issue, contributing to a high turnover rate and low production among loan officers.

Stratton Equities was born as a response to these challenges. Mikhail’s vision was to overhaul the methods used by the mortgage lending industry by incorporating more programs and generating an influx of organic inbound leads. Mikhail achieved remarkable success, making $1.3 million within six months of launching the company.

ADVERTISEMENT

Due to Mikhail’s unwavering dedication to delivering exceptional service and driving success, Stratton Equities is a leading player in the private money and NON-QM mortgage lending industry. With its customer-first approach, state-of-the-art technology, and extensive expertise, Stratton Equities has expanded its market reach and aims to achieve an impressive target of $1.2 billion in closed loan volume annually, or $100 million monthly.

Reflecting on the milestone, Mikhail commented, “As we celebrate, I am humbled and grateful for the incredible journey we have embarked upon. It has been a testament to our unwavering commitment, relentless dedication, and the trust our clients and partners place in us. This milestone is a celebration of our accomplishments and a reflection of the transformative power of perseverance and innovation in the lending industry. We have expanded our reach, refined our strategies, and surpassed expectations each year. As we look back on our journey, we are energized by the opportunities that lie ahead. Together, we will continue to shape the future of real estate financing and empower dreams. This is only the beginning, and the best is yet to come.”

One of the many successes that Mikhail created for Stratton Equities is the unique programs, lead generation model, and loan portfolio milestones. Mikhail has revolutionized lead generation and digital marketing with his innovative platform at Stratton Equities. Unlike traditional private money lenders relying on loan officers to hunt for leads through cold calls and networking, Mikhail’s system brings leads to the company daily, eliminating manual prospecting. This powerful tool generates an abundance of organic leads, surpassing the strategies of other private money-lending companies and propelling the company’s performance while enabling aggressive hiring.

Moreover, Mikhail’s platform provides loan officers with access to the largest collection of nationwide private money and NON-QM mortgage loan programs. This comprehensive offering allows them to effectively cater to the needs of real estate investors, entrepreneurs, and diverse mortgage borrowers.

Stratton Equities has received recognition within the industry for its exceptional services and expertise, as well as for Mikhail’s success. In 2021, Forbes Magazine included Mikhail in their “The Next 1000” list, celebrating individuals redefining what it means to build and run businesses today. NJBIZ, New Jersey’s leading business journal, also recognized Stratton Equities as one of the Top 250 Privately Held Companies for 2021. They further honored Mikhail as one of their 2022 Leaders in Finance, and he was nominated for the prestigious Ernst & Young Entrepreneur of the Year program.

Stratton Equities consistently achieves high levels of customer satisfaction. Through its commitment to providing personalized solutions and exceptional customer service, the company has built a strong reputation for its client-centric approach. Many clients have praised Stratton Equities for its outstanding service, professionalism, and ability to secure funding quickly. One client, John S., commended the company for its efficient processing and dedication to finding the best loan options, expressing gratitude for their personalized approach that ensured his unique needs were met. Another client, Sarah L., emphasized the team’s expertise in navigating complex financial situations, stating that Stratton Equities provided her with the guidance and support needed to secure a loan for her real estate investment. These testimonials and many more highlight the company’s commitment to client satisfaction and its track record of delivering outstanding results.

In addition to client testimonials, Stratton Equities has received positive feedback on reputable platforms such as Indeed and Glassdoor. Several employees have shared their experiences working for the company, consistently praising the supportive and collaborative work environment and highlighting the company’s dedication to fostering professional growth and providing ample opportunities for career advancement. Employees also speak highly of the company’s management, describing them as knowledgeable, approachable, and committed to the team’s and clients’ success. This positive employee feedback further supports the notion that Stratton Equities excels in serving its clients and maintains a workplace culture that values and nurtures its employees.

Mikhail’s visionary leadership and persistent commitment have solidified Stratton Equities’ position as a trusted and innovative company with high expertise, cutting-edge technology, and a customer-centric approach.

Michael Mikhail is the Founder and CEO of Stratton Equities, the nation’s leading hard money-lender to national real estate investors, with the largest variety of mortgage loans and programs nationwide.

Having launched Stratton Equities in early 2017, Michael has always been an entrepreneur and innovator in the real estate market, purchasing his first home at 19.

A serial entrepreneur with a foresight for business opportunities, Michael had a slew of small businesses prior to launching Stratton Equities. One of his most prolific ventures was a car wash connected to a gym he was affiliated with in Florida during 2001-2002 while attending college.

It wasn’t until he graduated from Florida State University with a degree in Business, that he officially joined the mortgage industry in 2003 and decided to travel to explore his options globally.

After travelling to 19 countries in 5 years, Michael knew two things; he wanted to start his own business and launch it in the United States. He knew that moving back to the states was the best place he could start something small and grow it into something infinite.

In 2017, Michael noticed how the mortgage industry had transformed after the regulations presented from 2008-2012, and knew it was time to set out something on his own, thus creating Stratton Equities.

Under Michael’s leadership, Stratton Equities has grown into one of the biggest leaders in the Mortgage and Real Estate industry across genres and platforms.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/07/celebration-cakes.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-07-28 04:24:592023-07-28 04:25:04From Homelessness to Multi-Millionaire: Michael Mikhail Leads Stratton Equities in Celebrating 5 Years of Success and Achievement

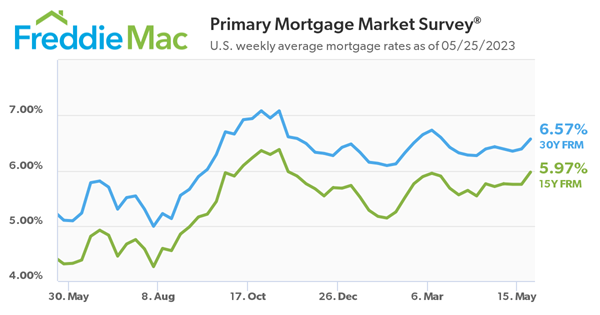

MCLEAN, Va., May 25, 2023 — Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey (PMMS), showing the 30-year fixed-rate mortgage (FRM) averaged 6.57 percent.

“The U.S. economy is showing continued resilience which, combined with debt ceiling concerns, led to higher mortgage rates this week,” said Sam Khater, Freddie Mac’s Chief Economist. “Dampened affordability remains an issue for interested homebuyers and homeowners seem unwilling to lose their low rate and put their home on the market. If this predicament continues to limit supply, it could open up an opportunity for builders to help address the country’s housing shortage.”

ADVERTISEMENT

News Facts

30-year fixed-rate mortgage averaged 6.57 percent as of May 25, 2023, up from last week when it averaged 6.39 percent. A year ago at this time, the 30-year FRM averaged 5.10 percent.

15-year fixed-rate mortgage averaged 5.97 percent, up from last week when it averaged 5.75 percent. A year ago at this time, the 15-year FRM averaged 4.31 percent.

The PMMS is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/05/mortgage-increase.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-05-26 05:28:382023-05-26 05:28:42Mortgage Rates Continue to Increase

This is an incredible opportunity for skilled professionals who want to work with a company that guarantees abundant direct organic daily leads, hands-on management training and support, niche mortgage loan programs with competitive pricing, and advanced mortgage technology.

Mortgage Loan Officers can expect to close their first loan within four to six weeks after the completion of their initial training.

ADVERTISEMENT

Mortgage Loan Officers who join the Stratton Equities team can expect the following:

Competitive compensation: Stratton Equities offers a highly competitive compensation plan, potentially allowing Mortgage Loan Officers to earn their first year $110,086.26 – $190,677.36.

Strong resources: Stratton Equities’ interest rates are some of the lowest nationwide in private lending, starting at 6.75%, and can pre-approve a loan in 24 hours.

Room for growth: As a rapidly growing company, Stratton Equities offers ample opportunities for advancement and career growth. With a focus on promoting from within, Mortgage Loan Officers who join the team will have the chance to take on new challenges and responsibilities as they progress in their careers.

A dynamic work environment: At Stratton Equities, Mortgage Loan Officers will work in a fast-paced, dynamic environment focused on innovation and results. As a part of the loan officer team, you can work directly with prospective real estate investors, entrepreneurs, and borrowers on their real estate endeavors.

If you are an experienced Mortgage Loan Officer looking for an exciting new opportunity to grow your career or a licensed Mortgage Loan Originator that is new to the industry and needs help finding business, then Stratton Equities is the place for you to earn a great income.

This is an incredible opportunity to join a leading nationwide mortgage lender and build a bright future with a company that values its employees and their contributions.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/05/HIRING.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-05-09 04:39:592023-05-09 04:52:08Stratton Equities is Hiring Mortgage Loan Officers to Join Their Dynamic New Jersey Team and Build a Lucrative Career in the Mortgage Industry

Why are you just searching for listed properties for sale when the number of distressed, vacant, and “shadow inventory” homes is almost 33 times larger than the national home listing inventory supply?

How is this possible with my 33 number claim? First, upwards of 16 million homes were listed as “vacant” or shadow inventory in the fourth quarter of 2022, as per the U.S. Census Bureau, National Association of Realtors (NAR), and other groups. A vacant home can be defined as a vacation home, unsold new home building inventory (near record levels of new single-family homes and multifamily apartment buildings being built in 2023), distressed or pre-foreclosure properties, or homes held by billion-dollar corporations like BlackRock, Blackstone, or State Street for the long-term that just sit there with no intent to rent it out at present.

Second, there are at least a few million distressed mortgages (FHA loans, especially) currently in forbearance agreements in order to delay the lender’s foreclosure filing actions to bring the total to more than 18.5 million properties. Frankly, I think that the number is closer to 20 million after counting VA, conforming, non-QM, and private money loans, but we’ll just focus on the 18.5 million vacant or distressed home number.

Since 1934, FHA (Federal Housing Administration) has insured more than 40 million loans nationwide. Today, a relatively high percentage of homebuyers still rely upon FHA to purchase their homes partly due to the much lower interest rates and easier loan qualification guidelines such as loan programs which allow FICO credit scores as low as 500, debt-to-income (DTI) ratios up to 50% or higher, and loan-to-value (LTV) options near 96.5% to 100% LTV.

As of March 2023, the national home listing inventory was listed at 562,565 by data provided by the Federal Reserve Economic Data and the NAR. Let’s do the math as follows:

18.5 million distressed or vacant homes / 562,565 listed homes = 32.885 times

ADVERTISEMENT

Distressed FHA Loans & Continued Forbearance Extensions

There are three to four times as many delinquent FHA mortgage loans nationwide as compared to the entire national home listing inventory with somewhere near at least a few million distressed FHA loans.

February 8, 2023: Today, the U.S. Department of Housing and Urban Development (HUD) Secretary Marcia L. Fudge announced that, thanks to Federal Housing Administration (FHA) programs, approximately 2 million homeowners with FHA mortgages were able to stay in their homes from the beginning of the COVID-19 pandemic in March 2020 through December 2022 – when doing so was often a matter of life and death. During this period of time amid the pandemic, FHA borrowers whose ability to make their mortgage payments was impaired by the pandemic were able to obtain either a COVID-19 forbearance or a more permanent solution such as a loan modification that allowed them to avoid foreclosure. Source: HUD Secretary Announces Major Milestone of Assisting Nearly 2 Million Homeowners Stay in their Homes

With a few million distressed FHA loans that they admit to and is probably undercounted, it’s no wonder why the federal government wants to keep offering FHA forbearance extensions.

Details of FHA’s COVID-19 Forbearance

Important information about FHA’s COVID-19 Forbearance:

To be eligible for the COVID-19 Forbearance or forbearance extension in the table above, you must request this relief from your servicer on or before May 31, 2023.

You can request a FHA COVID-19 Forbearance for up to 6 months. If needed, an additional 6 month extension may be requested. If you began your initial forbearance on or after October 1, 2021, you are only eligible for the additional 6 months if your initial 6 months forbearance will be exhausted and expires on or before May 31, 2023.

Additional forbearance options may be available to you after May 31, 2023. Your mortgage servicer may provide for a temporary pause or reduce your monthly mortgage payments to allow you time to overcome your financial hardship. An extended forbearance period may be provided to you if you are unemployed and actively seeking employment.

No extra fees, penalties, or interest will be added to your account during the forbearance period.

There are also a significant number of distressed VA and conforming or conventional loans nationwide which are held by Fannie Mae or Freddie Mac in the secondary market that aren’t really being “officially” counted with the most up to date numbers. FHA and VA mortgage loans have both consistently represented close to 10% each of the annual national funded loan market. As a result, these government-backed or insured loans, which typically average close to 0% to 3.5% down payments for FHA, VA, and conforming, are something to keep a close eye on as the economy continues to soften.

The 40-Year Loan Modification Program for FHA Borrowers

Good news: National mortgage delinquency rates dropped 15% in March 2023 while reaching 2.92%, which was a new all-time record low.

Bad news: Millions of distressed mortgages are not being counted as “delinquent” once they enter forbearance agreements with their lender (FHA loans, especially). The national FHA loan default rate reached 12% in February and will likely continue to rapidly increase. Distressed FHA and VA loan investments are some of the best deals out there because they usually have the lowest mortgage rates that you can take over by way of creative seller-financing techniques.

A forbearance agreement is when the lender or mortgage loan servicing company agrees to postpone or delay their foreclosure actions with the delinquent borrower. Sometimes, these foreclosure postponements may last months or years.

On March 8, 2023, HUD issued their Mortgagee Letter 2023-06 with details described as the “Establishment of the 40-Year Loan Modification Loss Mitigation Option” with a stated purpose noted as “This Mortgagee Letter (ML) establishes the 40-year standalone Loan Modification into FHA COVID-19 Loss Mitigation policies.”

Several mainstream media analysts mistakenly described this new 40-year loan proposal offered by FHA as a purchase loan as well. Yet, this is not correct because it’s only for the refinance of currently distressed 30-year FHA loans into longer 40-year loan terms in order to reduce the monthly payments for borrowers. There is no published word about whether FHA will later consider offering 40-year purchase loans for borrower prospects.

Housing and Family Trends

Real estate is a people business, first and foremost. The #1 most important factor for housing trends is related to population trends and household formations for families especially. Without people, there’s no need for housing regardless of the affordable financing offered.

One of the main reasons why people purchase single-family homes is because they’re trying to either build a growing family or the need to house two or three generations of the family under the same roof. You can’t spell “single-family homes” without family in it.

The U.S. has the highest percentage of one-person households in the entire world. A few years ago, one-person households surpassed all other household formations in Canada.

In 2022, only 24% of U.S. households had at least one child under the age of 18. In 1965, upwards of 42% of households had a child under the age of 18.

The Decline of Family Households

Here are some of the published data numbers from sources such as the U.S. Census Bureau, the National Center for Health Statistics (NCHS), Pew Research, and numerous other data sources in regard to individuals and family structure trends:

National overall divorce rate in the USA: 50%+.

The California divorce rate is 60%.

The Orange County, California divorce rate is 72%.

41% of first marriages nationwide end in divorce.

60% of second marriages end in divorce.

73% of third marriages end in divorce.

The average length of a marriage in the U.S. that ends in divorce is 8 years.

There is one divorce every 36 seconds in the U.S. on average; 2,400 divorces per day; 16,800 divorces per week; and 800,000 to 900,000 divorces per year.

The percentage of American men between the ages of 20 and 39 who are now married has fallen by half (35% of men are married as of 2017) since the early 1970s (70% of men were married).

Unmarried parents who live together are more likely to break up than married parents, per the Brookings Institute.

Per the CDC in 2016 through at least 2020, U.S. fertility rates were the lowest ever recorded as fewer couples are having children these days. Each consecutive year over the past five or six years reached all-time record lows.

78% of all households in the U.S. contained one married couple in 1950. Today, married households are below 48%.

In 2010, the Pew Research Center reported that 44% of Americans polled in the 18-to-29 year old age range believed that “marriage was becoming obsolete.”

Divorce rates for people over the age of 50 have doubled between 1990 and 2015, per Pew Research Center.

In 1956, roughly 5% of all babies were born to unwed mothers. Between 2008 and 2016, babies born to unwed mothers were closer to the 40% range.

Upwards of 50% of children in impoverished regions of the U.S. live in homes without fathers.

46% of children live at home with a mother and father who were in their first marriage together.

The average American woman in 1970 had her first child at 21.4 years of age. Today, the woman is near 25.6 years of age.

The U.S. has the highest teen pregnancy rate in the industrialized world.

More than 50% of children are born to unmarried women under the age of 30.

Saving Equity or Creating Newfound Wealth

What are your options as either a homeowner with an ongoing forbearance agreement in place with your lender, a struggling business owner, a commercial property owner and landlord with incredibly high vacancy rates, or as an investor seeking new opportunities if and when the economy suddenly pivots and we enter a more clearly visible deeper recession? If home values are more likely to be higher today than later this year, is it now a good time to sell? If so, where will be your next destination for a home?

Generally, loss of income is the #1 reason why homeowners lose their homes to lenders or mortgage loan service companies in foreclosure. The #2 reason why homeowners walk away from their home is when the mortgage debt exceeds the current market value and it’s upside-down or underwater. This is when short sale options become more prevalent.

ADVERTISEMENT

The real risk associated with homes purchased in recent years is related to the relatively low down payment averages for first-time buyers and others that were leveraged between 96.5% and 100% loan-to-value at the close of escrow. Effectively, these homebuyers were upside-down with negative equity at closing when factoring in the potential 6% to 8% closing costs to resell the homes after paying real estate brokerage commissions, title, escrow or attorney’s fees, transfer taxes, third-party inspection reports, and possible seller credits towards the buyer’s closing costs.

In 2022, first-time homebuyers represented 34% of all home purchases across the nation, as per the NAR. During the fourth quarter of 2022, purchase loans comprised 78.6% of all FHA mortgages funded. With a high percentage of FHA borrowers reported as first-time homebuyers, their average down payments were likely close to 3.5% or below. What happens if home values fall 5%, 10%, or more in value over the next year?

If you’re currently in a distressed mortgage situation as a homeowner or investor or are searching for discounted off-market listings as a buyer with very creative and flexible financing solutions, I can show you effective ways to save your equity or create newfound wealth with my mortgage and investment business named Realloans (Real Estate Loans and Creative Sales) and my real estate group linked here: So-Cal Real Estate Investors.

Rick Tobin

Rick Tobin has worked in the real estate, financial, investment, and writing fields for the past 30+ years. He’s held eight (8) different real estate, securities, and mortgage brokerage licenses to date and is a graduate of the University of Southern California. He provides creative residential and commercial mortgage solutions for clients across the nation. He’s also written college textbooks and real estate licensing courses in most states for the two largest real estate publishers in the nation; the oldest real estate school in California; and the first online real estate school in California. Please visit his website at Realloans.com for financing options and his new investment group at So-Cal Real Estate Investors for more details.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/05/house-ratio.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-05-02 06:29:572023-05-03 02:49:39A 33-to-1 Vacant & Distressed Home-to-Listed Home Ratio

Mortgage rates are rising again, causing the average homeowner to pay $800 a month more than they would have just a year ago, according to REALTOR.com.

The interest rate for a 30-year fixed mortgage is 6.54%, while the rate for a 15-year fixed mortgage is 5.75%, per Mortgage News Daily. Even Veterans Administration (VA) loans aren’t getting much relief, with the 30-year fixed rate coming in at 5.95%.

ADVERTISEMENT

While these numbers aren’t as high as they were in November 2022, they still present significant financial hurdles to would-be homebuyers, REALTOR.com reported.

Because prices are high, people need to borrow more money than before. Hence, people who could ordinarily buy a home are choosing to rent instead; this is good news for real estate investors.

ADVERTISEMENT

The last time mortgage rates were this high was 2008. With housing prices 42% higher than they were before the COVID-19 pandemic, this is a serious situation for many aspiring homeowners.

Investors and traditional buyers alike are encouraged to shop around for concessions, special programs, and to explore multiple lenders. However, some investors believe that the state of the economy will once again cause mortgage rates to increase.

Stephanie Mojica

Stephanie Mojica, writer of How One Writer Shifted From Settling for $12 an Hour to Prospering at Over $90 an Hour and shorter books such as Quick Answers to Frequently Asked Credit Questions, is an award-winning journalist with publications such as USA Today, The Philadelphia Inquirer, San Francisco Chronicle, and The Virginian-Pilot, among many others. She helps executive coaches, business consultants, business owners, attorneys, and other decision makers generate more money online and become the go-to expert in their field by guiding them step by step through the process of writing and publishing a book.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/05/MORTGAGE.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-05-01 05:53:112023-05-01 05:53:16Mortgage Rates are Rising Again

In the wake of recent bank failures, mortgage rates have dropped, according to REALTOR.com. During the week of March 13, 2023, mortgage rates have been between 6.57% and 6.75%.

The rates are anticipated to continue to fall, giving renewed hope to many traditional homebuyers and real estate investors.

ADVERTISEMENT

Silicon Valley Bank, Signature Bank, and Silvergate Bank have all failed, which has caused some would-be homebuyers to become nervous about getting a mortgage. There are concerns that other banks could collapse as well as anxiety about the general economic uncertainty in the world, Ali Wolf, chief economist of the building consultancy Zonda, told REALTOR.com.

However, Wolf noted that all the drama will probably lower mortgage rates even further. If rates go down by even .50 percent, the average housing payment would be lowered by $100 each month.

ADVERTISEMENT

The good news in the bank collapse situation is that the U.S. federal government is covering people’s losses from Silicon Valley Bank and Signature Bank, which will surely assuage some people’s fears. Because Silvergate Bank handled cryptocurrency such as Bitcoin, the feds are not able to recoup customers’ losses.

REALTOR.com recommends that people in the market for a mortgage to check rates at least once a day and stay in close contact with lenders.

Stephanie Mojica

Stephanie Mojica, writer of How One Writer Shifted From Settling for $12 an Hour to Prospering at Over $90 an Hour and shorter books such as Quick Answers to Frequently Asked Credit Questions, is an award-winning journalist with publications such as USA Today, The Philadelphia Inquirer, San Francisco Chronicle, and The Virginian-Pilot, among many others. She helps executive coaches, business consultants, business owners, attorneys, and other decision makers generate more money online and become the go-to expert in their field by guiding them step by step through the process of writing and publishing a book.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/03/MORTGAGE-DROP.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-03-17 03:18:392023-03-17 03:18:44Bank Failures Cause Mortgage Rates to Drop

Over 33% Reduction in FHA Annual Mortgage Insurance Premium Will Open the Door to Home Ownership for More Americans

Advisors Mortgage Group, based in Ocean Township, New Jersey, today comments on the recent announcement from the Department of Housing and Urban Development (HUD), through the Federal Housing Administration (FHA), that starting on March 20, 2023, it is reducing annual mortgage insurance premiums by 30 basis points on FHA-insured mortgages. The reduction will benefit approximately 850,000 borrowers over the next year, which will save these families an average of $800 annually.

ADVERTISEMENT

How does this translate into savings for a buyer looking to get an FHA-insured mortgage*? If an individual were to buy a home at a sales price of $400,000 and put 3.5% down, the mortgage would be $386,000. The current mortgage insurance premium (MIP) would be $271.89 per month. Once the 30 basis point reduction takes place, the MIP will be $175.93 per month. That is a savings of $1,151.52 per year. This change applies to new loans only starting on March 20, 2023.

This change comes on the heels of a few other recent updates by HUD to make home ownership a reality for more Americans. The FHA’s underwriting policies were changed to allow lenders to use positive rental history in evaluating applicants’ creditworthiness for an FHA-insured mortgage. This will make it easier for first-time home buyers to qualify for a mortgage. HUD also changed the way in which student loan debt is evaluated in FHA mortgage underwriting, which will enable more borrowers who are making payments on student loans to qualify for an FHA mortgage.

ADVERTISEMENT

Erika Whalen, Advisors’ underwriting manager, states, “These steps by HUD and the FHA are going to help many more people achieve the dream of owning a home. We at Advisors are excited to see these changes take place and that we now get to be a part of the American dream of home ownership for even more first-time home buyers.”

*The FHA’s annual MIP is a percentage of the outstanding loan balance. Advisors Mortgage Group is an FHA-approved lender and is not acting on behalf of or at the discretion of HUD/FHA or the federal government.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/03/advisors-3-7-23.jpg352624dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-03-08 02:56:192023-03-08 02:57:43Advisors Mortgage Poised to Help Clients Benefit from Recent Federal Housing Authority (FHA) Announcement