As the leading Private Money and NON-QM Mortgage Lender in the United States, Stratton Equities is looking to grow its licensed loan officer team.

2022 was a time of growth and expansion for the company. To support the abundance and high demand of direct inbound organic lead applications in the new year, they have decided to add a new roster of licensed loan officers to their sales team.

Have you been looking for a career as a mortgage loan officer?

Stratton Equities is passionate about creating a system of success for our winning sales team. We guarantee direct organic daily leads, niche loan products with competitive pricing, advanced mortgage technology, and hands-on training with management and support when working with our company.

ADVERTISEMENT

When you’re a loan officer, everywhere else, you are hunting your own business, spending money on travel, promotion, and marketing expenses that cost thousands of dollars in hopes of leads or deals. We have solved this problem by providing our loan officers with a stable location and opportunities for pure profit. For example, a Stratton Equities loan officer will structure and price out 15-20 mortgage loan scenarios a day from our direct organic daily leads.

With a significant influx of clientele, we need all hands on deck to get borrowers the best mortgage program to fit their unique loan scenarios.

If you are a licensed Mortgage Loan Originator that is new to the industry and is having difficulty finding business, we have the solution.

Stratton Equities provides our loan officers with inbound organic daily leads from people who call or apply directly to our offices inquiring about a mortgage. Not the other way around.

We have a time-tested training model that includes a proprietary system for lead generation, an open-door policy with management, and one of the industry’s most comprehensive range of mortgage loan programs under one roof.

In addition, we have innovative loan products specializing in different mortgage loan programs such as Hard Money, No-Doc Loans, NON-QM Loans, DSCR Loans, Soft Money Loan Programs, Bridge Loans, Conventional Loans, Fix & Flip Loans, Commercial Loans and more.

Why should you become a Loan Officer with Stratton Equities?

Let’s first start with some motivation and intrigue. Why might someone be interested in becoming a loan officer? Well, as a loan officer, you will be able to work with numerous borrowers and real estate investors all across the United States and help make their investment dreams become a reality.

Here are some of the benefits of joining the Stratton Equities’ Loan Officer Team:

– Direct Organic Daily Inbound Leads

– Hands-on Training & Management Support

– Largest library of niche loan products – say “YES!” more!

-Cutting-edge industry technology

Yearly Earing Potential: $129,086.00 – $189,677.00 per year

Benefits: 401(k), Dental insurance, Health insurance, Vision insurance

As a part of our private lending loan officer team, you can work directly with prospective real estate investors, entrepreneurs, and borrowers on their real estate endeavors.

Stratton Equities has the most extensive library of mortgage loan programs under one roof and can offer borrowers an array of loan strategies. In addition, we work with real estate investors advising them on what mortgage program they should opt for, all while operating under a solid private lender umbrella.

ADVERTISEMENT

We offer the most effective loan options for borrowers and direct access to new, organic leads for all our loan officers. As a result, our interest rates are some of the lowest in private money, starting at 6.99%, and we can pre-approve a loan in 24-48 hours. In addition, our new loan officers are supported to achieve the goal of closing their first loan within 4-6 weeks after training is completed.

Additionally, you will be a part of a massive operation in which you will help structure and maneuver hundreds of thousands to millions of dollars simultaneously with each client. The job will be demanding at times, but those with the patience and integrity to deal with problems as they arise will be rewarded with the satisfaction of pulling off an impressive feat for the financial glory of their clients and themselves.

How to apply to become a mortgage loan officer at Stratton Equities:

At Stratton Equities, we are looking for the following requirement for our new loan officer hires:

– Ready to work/relocate to our New Jersey Headquarters Office

– Be a motivated individual and a team player

To be successful as a mortgage loan officer, you should be fully prepared and well-versed in our mortgage loan options. At Stratton Equities, we educate our loan officers through our extensive training program that prepares our team to reasonably help clients as they apply to secure mortgage financing.

Hands-on learning is the best way to become a master of your craft, and that is why we emphasize a direct approach with onboarding, as we want our new loan officers to be fully prepared for the career path and not stumble over minor details.

A license might be the proper prerequisite to knowing how a loan officer works, but finding out the nuances on-the-job will be the ultimate test.

Stratton Equities has openings in its next training cycle in February 2023. They will choose the following candidates for their new loan officer team during the training process.

In the office, training lasts one week, with ongoing management support and education.

Loan officer trainees are trained and supported to close loans on average between 4-6 weeks after the completion of training.

Michael Mikhail is the Founder and CEO of Stratton Equities, the nation’s leading hard money-lender to national real estate investors, with the largest variety of mortgage loans and programs nationwide.

Having launched Stratton Equities in early 2017, Michael has always been an entrepreneur and innovator in the real estate market, purchasing his first home at 19.

A serial entrepreneur with a foresight for business opportunities, Michael had a slew of small businesses prior to launching Stratton Equities. One of his most prolific ventures was a car wash connected to a gym he was affiliated with in Florida during 2001-2002 while attending college.

It wasn’t until he graduated from Florida State University with a degree in Business, that he officially joined the mortgage industry in 2003 and decided to travel to explore his options globally.

After travelling to 19 countries in 5 years, Michael knew two things; he wanted to start his own business and launch it in the United States. He knew that moving back to the states was the best place he could start something small and grow it into something infinite.

In 2017, Michael noticed how the mortgage industry had transformed after the regulations presented from 2008-2012, and knew it was time to set out something on his own, thus creating Stratton Equities.

Under Michael’s leadership, Stratton Equities has grown into one of the biggest leaders in the Mortgage and Real Estate industry across genres and platforms.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/02/worth-it.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-02-21 02:54:102023-02-21 02:54:14Is Becoming A Loan Officer Worth It?

Future and current homeowners have been mesmerized by countless media reports about increasing mortgage rates and decreasing home sales prices. However, the 20-year high in mortgage rates is not the biggest problem facing the real estate market, according to REALTOR.com.

ADVERTISEMENT

Many residential properties are staying on the market significantly longer because the combination of increased mortgage rates and home prices is too much for the average buyer to bear. As a result, a number of potential buyers are waiting for housing prices to drop, per FOX Business.

As of October 27, 2022, the average interest rate for a 30-year fixed mortgage was 7.08%. The average at the same time last year was 3.14%. The current rate for a 15-year fixed mortgage is 6.36%, compared to 2.37% in 2021.

ADVERTISEMENT

Some real estate investors are panicking over these changes in market conditions, Fortune.com noted. This may be justified, as home prices fell 27% between 2006 and 2012 — and experts expect even more significant reductions in the years to come. Prices have plunged 8.2% in San Francisco, for example.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2022/11/MORTGAGE-UP.png4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2022-11-03 04:41:272022-11-03 04:41:30Increasing Mortgage Rates are Only Part of the Problem

One of the best jobs you can go for these days if you want to work hard, make a lot of money, and change the world around you is to become a mortgage loan officer. There are so many opportunities out there in the real estate world to make a living, but one of the most fulfilling and lucrative is to become a mortgage loan officer for a private money lending firm.

But what are the steps you will have to take to even become a loan officer?

Like most careers that deal with highly valuable assets and specified levels of management and service, to become a loan officer, you need to get your license. The NMLS, or Nationwide Mortgage Licensing System, offers a variety of mortgage licenses but the one in particular that applies to loan officers most is the Mortgage Loan Originator (MLO) license.

ADVERTISEMENT

How to get licensed as a Mortgage Loan Officer/Originator

Getting an NMLS license will certify that as a loan officer, you are now able to legally serve as a mortgage loan originator. Additionally, it informs your prospective clients and employers, that you are knowledgeable of all the laws and regulations that come with mortgage lending.

More specifically, obtaining an NMLS license means that you have completed a class that teaches you all the requirements for serving as a mortgage loan officer, and that you have passed the SAFE Mortgage Loan Originator Test.

You must complete both tasks to be properly qualified to apply for the NMLS license. Once you have your NMLS license, you can easily apply for most private lending and conventional mortgage lender positions.

Although the Nationwide Mortgage Licensing System (NMLS) License covers across the country, you will still need to apply for an individual license per state you are looking to lend in.

Applying to Become a Mortgage Loan Officer with a Private Lender

Believe it or not, the next step in becoming a mortgage loan officer is finding a position at a private lending firm that suits your needs and interests. The NMLS license qualifies loan officers for all private lending and conventional lending mortgage companies. This will allow you to apply for all loan officer positions, however, you will still need the individual license per state.

After applying at your desired location, the interview process shouldn’t be too surprising or different from any other high-level interview process as they will mainly ask you questions and test you on your skillset, knowledge, and ambitions.

Once you’ve secured the position, the best private lending firms will provide thorough training, management, and support.

ADVERTISEMENT

Working at a Private Lending Mortgage Company

Through training new loan officers, a private lender prepares their sales team to help guide them to mastering some of the nuances required as a loan officer, that cannot be taught purely through an academic mindset.

You must be ready and focused as a loan officer and this level of training throughout the first few months of the job will help get you to that point.

As important as it is to get certified by the NMLS, there is only so much you can learn by studying laws, memorizing loan options, and practicing unique scenarios. The real test of grit is to see how well you work in a real-world setting.

To be successful as a loan officer you need to be sharp-minded at all hours, diligent in the details, dedicated to working hard, and affirmative in your tone, actions, and decisions. Furthermore, be intuitive enough to understand what is a good deal and how to thread the needle if plans don’t go as expected.

The work will be hard but the rewards are great. On average a mortgage loan officer at a private lending mortgage company can make an average of $150,000-$250,000 a year.

Securing Your Position as a Mortgage Loan Officer

To secure your career as a successful loan officer at a private lending institution, there are a couple more things you can do to ensure your success.

Firstly, there is the option to get certified by the Mortgage Bankers Association (MBA) and/or the American Bankers Association (ABA). This step is optional and not required for the position of loan officer, but getting this certificate can help boost your credentials, entice more clients to come your way, acquire yourself more deals and negotiations from borrowers, and specialize your skill set such that you are even more knowledgeable and prepared as a loan officer.

Lastly, you must renew your NMLS license every year. This is to ensure that whoever is still practicing they are aware of certain changes in the law, whether it be on the nationwide level or statewide. Additionally, renewing your license frequently keeps you fresh and sharp-minded as you are regularly checked on how well and how prepared you are at the job.

These are all the principal steps one takes when seeking to become a loan officer. The process is fairly intuitive for this type of position while also being thoroughly detailed in ensuring that only the best and most prepared are the ones handling multi-million dollar real estate investment deals.

Become a Mortgage Loan Officer/Originator with Stratton Equities! We’re Hiring!

If you are a licensed Mortgage Loan Originator that is new to the industry and is having a difficult time finding business, we have the solution.

Stratton Equities provides our loan officers with daily direct organic leads, that are from people that call into or apply to our offices looking for a mortgage. Not the other way around. We have a time-tested model that includes a state-of-the-art CRM and lead generation, amazing hands-on training, and the widest range of mortgage loan programs in the industry.

We have niche products that specialize in different types of loans such as Hard Money, No-DOC Loans, Soft Money Loan Programs, Non-QM Loans, Conventional, Fix & Flip, Commercial and more.

Benefits of working with Stratton Equities:

Direct Organic Leads Hands-on Training & Support Largest library of niche loan products – say “YES!” more!

Pay: $158,086.00 – $294,677.00 per year Benefits: 401(k), Dental insurance, Health insurance, Vision insurance

For more information on how to get started as a loan officer, visit Stratton Equities today. We offer the largest variety of loan options that can all be directly accessed by our borrowers. Our starting interest rate is the lowest out of any private money lender, and you can get your loan approved in as little as 24-48 hours.

Additionally, our average time frame in closing loans for our new loan officers is 4-6 weeks after training.

https://www.realestateinvestormagazines.com/wp-content/uploads/2022/11/MORTGAGE-OFFICER.png4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2022-11-02 02:38:002022-11-02 02:38:03How To Become A Mortgage Loan Officer

Why can’t commercial lending be as flexible as residential lending? Residential mortgage lending for one-to-four unit properties has become more automated and streamlined for investors as we move forward here in the 21st century. More homeowners and investors are seeking out experienced independent mortgage brokers who may have relationships with numerous financial institutions, nonbank lenders, or private money sources. With a few clicks of a button, the mortgage professional can quickly find the best financial solutions available for their clients and get approvals within minutes, hours, or days.

Commercial property lending, on the other hand, still seems stuck in the 20th century for many commercial applicants. It can be perceived as a “good ol’ boy/girl network” in that the commercial loan applicant needs to have some sort of a long-established personal relationship with their local community banker dating back to high school, college, or as fellow members at the local golf club before their loan requests are approved. If so, will they be types of friendly handshake approvals or not-so-friendly “take it or leave it” approvals?

ADVERTISEMENT

If the commercial loan applicant is fortunate to find a banker who may consider their deal, this same banker may request that the borrower move their deposits from other financial institutions to their bank before considering the applicant’s loan request. Should the loan be rejected either quickly or months later after a rather brutal loan underwriting process that may include a footlong stack of paperwork, the disheartened customer may give up hope and not know where to turn for another lending option.

Today, non-owner occupied residential properties (one-to-four units) offered as short-term or long-term rentals, multifamily apartments (5+ units), mixed-use, office, industrial, retail, and special purpose (auto repair shops, etc.) can all be viewed as a “commercial loan” by certain nonbank lenders that don’t collect customer deposits like traditional banks. With lower loan-to-value (LTV) ranges for certain asset-based loan products, the risk of default is lower for the nonbank lenders.

Wealth Creation from Commercial Property Ownership

Let’s take a look at commercial property trends and how much wealth was created for those fortunate owners who learned that it’s much better to let their money work hard for them than vice versa:

The estimated total dollar value of commercial real estate was $20.7 trillion as of Q2 2021. (Nareit and CoStar)

By 2050, commercial building floor space is expected to reach 124.3 billion square feet, a 33% increase from 2020. (Center for Sustainable Systems, University of Michigan)

72% of commercial buildings in the US are 10,000 square feet or smaller. (National Association of Realtors)

The typical length of a building lease in the US is three to 10 years. (DLA Piper)

Commercial property prices rose by 20% between May 2021 and May 2022. (Green Street)

An estimated one-third of industrial space in the US is more than 50 years old. (NMRK)

For every $1 billion of growth in the e-commerce sector, it requires an extra 1.2 million square feet of new warehouse space. (Prologis)

Self-storage commercial unit REITs produced a 70% market return in 2021 (REIT)

Approximately 69% of all commercial buyers in the US need financing to purchase properties. (National Association of Realtors)

Sales of multifamily apartment buildings increased by 22.4% year-on-year in 2022 (Colliers)

Prior to the March 2020 pandemic designation, the industrial real estate sector had grown for 40 consecutive quarters or over 10 years. (NMRK)

Industrial vacancy rates nationwide fell below 3.7% at the end of 2021. (Cushman & Wakefield)

The Inland Empire (Riverside and San Bernardino counties) in California averaged an incredibly low 1.2% vacancy rate for industrial space. (Commercial Edge)

California had 27 of the 50 highest office rental prices in 2021. (Commercial Search)

The average annual return for commercial real estate investors is approximately 9.5%. (Mashvisor)

For every retail unit that closes, five new stores open up. (NRF)

Technological Advances for Commercial Loans

What if the commercial lending process could be digitized, sped up, and completed on a secure online loan application with just one point of contact? Your odds of success for getting a commercial property loan approved for a multifamily apartment building, mini-storage site, or small retail center will be much higher if your financial contact person is very experienced with commercial lending and has access to numerous lenders.

Commercial loans are somewhat like giant jigsaw puzzles. While the applicant’s loan package may not fit the guidelines required at one, two, or 10 different lenders, there are other lenders that have more flexible guidelines which allow lower positive, break-even, or even negative DSCR (Debt Service Coverage Ratio) with or without income verification.

Properties with lower positive cash flow or even negative cash flow estimates will likely not qualify at a local community bank or credit union. Yet, they may qualify with other nonbank lenders that do allow break-even or negative cash flow. Some of our lending partners are asset-based lenders that don’t review the applicant’s tax returns as well as provide financing for property improvements. These types of incredibly flexible lending guidelines can make the commercial loan application process much easier for the borrower.

ADVERTISEMENT

An Imploding Financial System and Increasing Bank Restrictions

In 2008, the Credit Crisis (aka Financial Crisis, Subprime Mortgage Crisis, or Global Financial Crisis) default risks became more readily apparent as these prominent financial institutions or government entities collapsed and/or were bailed out:

Bear Stearns: The fifth largest investment firm in the world that was heavily invested in mortgage-backed securities, collateralized debt obligations (CDOs), and other complex securities or derivatives instruments.

Lehman Brothers: The biggest bankruptcy ever involving over $600 billion in assets.

Washington Mutual (WAMU): Largest bank implosion in US history with almost $328 billion in assets.

FDIC (Federal Deposit Insurance Corporation): They only held $40 billion in cash reserves at the time of WAMU’s collapse, so the government had to silently bail them out to prevent bank runs.

Countrywide Mortgage: Once America’s #1 residential mortgage lender that almost imploded prior to being bailed out by Bank of America.

American International Group (AIG): They were the world’s largest insurance company and were bailed out by the US government starting with $85 billion while growing to more than $182 billion several years later.

Merrill Lynch: The world’s largest stock brokerage firm at the time with $2.2 trillion under management and 15,000 brokers that was taken over by Bank of America.

A derivative is a complex hybrid financial and insurance instrument which “derives” value from underlying assets or benchmarks like interest rate direction trends. Some financial analysts have stated that the total value of all global derivatives may be somewhere within the $1,500 to $3,000 trillion dollar region. If so, these derivatives dwarf all combined global assets by a significant multitude.

Because so many banks, investment firms, and insurance companies are heavily invested in one another partly by way of derivatives, this was why the Federal Reserve, the Bank of England, and other central banks around the world had to step in and bail out these multi-billion or multi-trillion dollar financial or insurance entities, directly or indirectly through others like Bank of America. If not, the global financial system would have fallen like a dominoes chain reaction.

Later, the LIBOR (London Interbank Offered Rate) Scandal, which came to light publicly in 2012, gave us a glimpse of the sheer magnitude of the derivatives market. This financial scandal was about how certain financial institutions invested or bet on the future direction of interest rates tied to LIBOR (the benchmark interest rate at which major global banks lend to one another) while being claimed to be rigged or known ahead of time so that the derivatives bets had a better chance of success.

Several publications like Rolling Stones Magazine wrote articles about the LIBOR Scandal potentially being the largest financial scandal in world history that affected upwards of $500 to $700 trillion in global assets. The named financial institutions in various publications or lawsuits which were alleged to have benefited, directly or indirectly, in the LIBOR Scandal included Deutsche Bank, HSBC, Barclays, Citigroup, JP Morgan Chase, and the Royal Bank of Scotland.

What’s important to understand is that many of the best known banks in the world may only have a few trillion of depositor assets in their checking and savings accounts today. However, they may have exposure to upwards of $50 + trillion in derivatives. As a result of their financial exposure to derivatives, these banks may be unwilling or unable to make investment property loans to even their most creditworthy clients partly due to tighter lending restrictions that came from the passage of the Dodd-Frank Act back in 2010.

This is why mortgage brokers and their non-bank lending partners became the better funding solution for investors while “handshake deals” at local banks don’t matter as much because so many banks may be technically insolvent.

Ironically, it was claimed that delinquent subprime mortgages represented less than 1% of all financial losses related to the Credit Crisis or Financial Crisis. Rather, the complex derivatives investments that were leveraged 50+ times the original amount of investments such as interest-rate options were the root cause. Sadly, mortgage professionals and stated income subprime loans still continue to be primary scapegoats. As a result, fewer banks are willing to offer more flexible residential or commercial property loans that don’t verify income.

Value Analysis for Commercial Properties

How lenders analyze income and expenses for commercial properties can be quite complex and overwhelming. Properties that do not meet most or all of these stringent underwriting guidelines may be prime candidates for asset-based loans.

Let’s try to review and simplify some key valuation terms that lenders may consider before approving or denying a borrower’s request:

Loan-to-value (LTV): The proposed loan amount as a percentage of the estimated property value. Many lenders prefer a loan-to-value range somewhere within the 50% to 75% LTV range. For purchase deals, these same lenders prefer that their clients put upwards of 25% to 50% of the purchase price as a cash down payment, depending upon the creditworthiness of the borrower and the property type.

Net Operating Income (NOI): The NOI for a commercial property can be summed up as follows: Gross Income – Operating Expenses = NOI

The property’s operating expenses include insurance, property management, utilities, and other day-to-day costs related to maintaining the property. However, the mortgage payments are not included within the NOI calculation.

Cap or Capitalization Rate: It’s a mathematical formula used to calculate the real or projected future rate of return on a property based on the net operating income that the property generates. The lower the cap rate, the better the property. Higher cap rates, in turn, are viewed as riskier investments. Cap Rate = NOI / Current Market Value

Property values and cap rates are inverse to one another like a seesaw. Decreasing cap rates as seen with prime downtown properties that are fully occupied leads to increasing property values. Conversely, rising cap rates for older rundown commercial properties usually correspond with falling property values.

Value Estimate: The property’s value estimate can be determined by way of the following formula: NOI / Cap Rate

For example, let’s look at two multifamily apartment buildings located in different cities with the exact same NOI but cap rates that are not nearly the same:

Building 1: $160,000 NOI divided by an 8% cap rate ($160,000 / .08%) = $2,000,000 value

Building 2: $160,000 NOI divided by a 4.5% cap rate ($160,000 / .045%) = $3,555,556 value

Generally, multifamily apartment rates have the lowest cap rates for income-producing properties that aren’t considered to be residential (one-to-four unit) properties. As per an analysis for the 2nd quarter of 2022 by Real Capital Analytics and the NAR, here are their numbers:

Property Type Apartments Industrial Office Retail

Cap Rate 4.5% 5.7% 6.3% 6.3%

DSCR: The easiest way to remember the debt service coverage ratio (DSCR) is that it’s used to determine whether or not a property has positive (1.25x), neutral or break-even (1.0x), or negative cash flow (0.75x). The DSCR is the ratio of operating income that’s available on a monthly or annual basis to service or cover the monthly mortgage payment (principal, interest, property taxes, insurance, etc.). As a mathematical formula, the DSCR can be visualized as follows: NOI / Debt Service

A small retail center that generates $10,000 per month in operating income and has a projected $8,000 per month in total mortgage payments would be calculated at 1.25x DSCR because the monthly or annual cash flow is 25% higher than the debt service ($10,000 / $8,000 = 1.25x). The net difference between $10,000 inflow and $8,000 debt service outflow is $2,000. This can also be calculated as $2,000 divided by the $8,000 in debt service ($2,000 / $8,000) which equals 25% more net cash flow to arrive at 1.25x DSCR.

Debt Yield: The commercial property’s NOI as a percentage of their total loan amount. The mathematical formula is as follows: NOI / Loan Amount = Debt Yield

For example, a small industrial building owner collects $100,000 NOI each year. His existing mortgage loan balance is $1 million, so his annual debt yield is 10% ($100,000 NOI / $1 million mortgage balance).

Multiple Underwriting Approval Solutions

As you better learn how lenders analyze properties, you will clearly understand that you have more than one loan program available. Some properties and owners will easily qualify after sharing tax returns, liquid assets, profit-and-loss statements, and a detailed income and expense history for their property. Other investors, however, know that their property’s cash flow is break-even or negative, but the future upside for these properties can be tremendous after occupancy rates are pushed higher.

Many commercial property owners experienced unusually high vacancy rates in recent years due to the combination of the pandemic, skyrocketing inflation, rising tenant payment delinquencies, and increasing rates for consumer debt. If so, the income and expense numbers for these commercial properties will probably not qualify at a traditional bank.

Commercial borrowers are more likely to qualify with asset-based nonbank lenders that may not closely review the income and expense numbers for the property. The verifying of income for asset-based, nonbank lenders isn’t necessary because these loans are based more on the appraised value of the subject property and its future income potential. At a later date when the income and occupancy rates are higher while the operating expenses decline, the owner can refinance into a much longer loan term at a lower rate and monthly payment.

Remember, it’s much better to have multiple lending options available for your property purchases or ballooning loan or cash-out refinance needs than just one local bank. The more efficient and flexible the mortgage broker’s technological systems and nonbank lending sources, the more likely you will close your loan and create significant income and increased wealth.

Rick Tobin

Rick Tobin has a diversified background in both the real estate and securities fields for the past 30+ years. He has held seven (7) different real estate and securities brokerage licenses to date, and is a graduate of the University of Southern California. Rick has an extensive background in the financing of residential and commercial properties around the U.S with debt, equity, and mezzanine money. His funding sources have included banks, life insurance companies, REITs (Real Estate Investment Trusts), equity funds, and foreign money sources. You can visit Rick Tobin at RealLoans.com for more details.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2022/10/mortgage.jpg3901000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2022-10-05 04:37:402022-10-05 04:37:44Simplifying and Automating Commercial Mortgages

By Zach Wichter Special Submission from Bankrate.com

What is cash-out refinancing?

Cash-out refinancing replaces your current home loan with a bigger mortgage, allowing you to take advantage of the equity you’ve built up in your home and access the difference between the two mortgages (your current one and the new one) in cash. The cash can go toward virtually any purpose, such as home remodeling, consolidating high-interest debt or other financial goals.

How a cash-out refinance works

The process for a cash-out refinance is similar to a rate-and-term refinance of a mortgage, in which you simply replace your existing loan with a new one for the same amount, usually at a lower interest rate or for a shorter loan term, or both. In a cash-out refinance, you can do the same, and also withdraw a portion of your home’s equity in a lump sum.

“Cash-out refinancing is beneficial if you can reduce the interest rate on your primary mortgage and make good use of the funds you take out,” says Greg McBride, CFA, Bankrate chief financial analyst.

For example, say the remaining balance on your current mortgage is $100,000 and your home is currently worth $300,000. In this case, you have $200,000 in home equity. Let’s assume that refinancing your current mortgage means you can get a lower interest rate, and you’ll use the cash to renovate your kitchen and bathrooms.

Since lenders generally require you to maintain at least 20 percent equity in your home (though there are exceptions) after a cash-out refinance, you’ll need to have at least $60,000 in home equity, or be able to borrow up to $140,000 in cash. You’ll also need to pay for closing costs like the appraisal fee, so the final amount could be less.

You tend to pay more in interest after completing a cash-out refinance because you’re increasing the loan amount, and like other loans, you’ll have to pay for closing costs. Otherwise, the steps to do this kind of refinance should be similar to when you first got your mortgage: Submit an application after selecting a lender, provide necessary documentation and wait for an approval, then wait out the closing.

How to prepare for a cash-out refinance

Here’s how you might prepare for a cash-out refinance:

1. Determine the lender’s minimum requirements

Mortgage lenders have different qualifying requirements for cash-out refinancing, and most have a minimum credit score — the higher, the better. The other typical requirements include a debt-to-income ratio below a certain percentage and at least 20 percent equity in your home. As you explore your options, take note of the requirements.

If you’re considering a cash-out refinance, you’re likely in need of funds for a specific purpose. If you aren’t sure what that is, it can be helpful to nail that down so you borrow only as much as you need. For instance, if you plan to use the cash to consolidate debt, then gather your personal loan and credit card statements or information about other debt obligations, and add up what you owe. If the cash is to be used for renovations, consult with a few contractors to get estimates for both labor and materials ahead of time.

3. Have your information ready when you apply

Once you’ve shopped around for a few lenders to ensure you get the best rate and terms, prepare all of your financial information related to your income, assets and debt for the application. Keep in mind you might need to submit additional documentation as the lender evaluates your application.

What’s the point of a cash-out refinance?

Considerations before cash-out refinancing

You can’t tap 100 percent of your equity: Most lenders require you to maintain at least 20 percent equity in your home in a cash-out refinance. One exception is a VA cash-out refinance, which allows you to withdraw all of your equity.

You could end up with a very different loan: Since you’re replacing your existing mortgage with a new loan, the terms of the loan could change. For instance, you might have a higher or lower interest rate (and monthly payments), or a longer or shorter loan term.

You’ll need to have your home appraised: Lenders typically require an appraisal for conventional cash-out refinances, since the amount you can borrow depends on how much equity you have.

You’ll pay closing costs: Like with your first mortgage, cash-out refinances come with closing costs, which cover lender fees, the appraisal and other expenses. It’s important to consider what a cash-out refinance could cost you because the fees might not be worth it, especially if you’re not borrowing a large amount.

The cash won’t land in your bank account right away: Lenders are required to give you three days after closing to back out of the refinance if you want to. For this reason, you’ll need to wait a few days before you receive the funds.

How much money can I get from a cash-out refinance?

While lenders typically allow homeowners to borrow up to 80 percent of the home’s value, the threshold can vary depending on your credit score and type of mortgage, as well as the type of property attached to the loan (for example, a single-family, duplex or three- or four-unit property). Lenders who offer loans insured by the Federal Housing Administration, or FHA, sometimes offer an FHA cash-out refinance that allows you to borrow as much as 85 percent of the value of your home. As noted, cash-out refinance loans guaranteed by the U.S. Department of Veterans Affairs (VA) are available for up to 100 percent of the home’s value.

What are the fees for a cash-out refinance?

Expect to pay about 3 to 5 percent of the new loan amount for closing costs to do a cash-out refinance. These closing costs can include lender origination fees and an appraisal fee to assess the home’s current value. Shop around with multiple lenders to ensure you’re getting the most competitive rates and terms.

You might be able to roll the loan costs into your new mortgage to avoid upfront closing costs, but you’ll likely pay a higher interest rate. Plus, taking out another 30-year loan or refinancing at a higher interest rate might mean you pay more in total interest. Crunch the numbers with Bankrate’s refinance calculator to gauge whether the math works in your favor.

Pros and cons of cash-out refinance

Before you decide to go through with a cash out refinance, it’s important to consider the pros and cons of cash out refinancing.

You can lower your rate: This is the most common reason most borrowers refinance, and it makes sense for cash-out refinancing as well because you want to pay as little interest as possible when taking on a larger loan.

Your cost to borrow could be lower: Cash-out refinancing is often a less expensive form of financing because mortgage refinance rates are typically lower than rates on personal loans (like a home improvement loan) or credit cards. Even with closing costs, this can be especially advantageous when you need a significant amount of money.

You can improve your credit: If you do a cash-out refinance and use the funds to pay off debt, you could see a boost to your credit score if your credit utilization ratio drops. Credit utilization, or how much you’re borrowing compared to what’s available to you, is a critical factor in your score.

You can take advantage of tax deductions: If you plan to use the funds for home improvements and the project meets IRS eligibility requirements, you could take advantage of the interest deduction at tax time.

Some of the drawbacks of cash out refinances are

Your rate might go up: A general rule of thumb is to refinance to improve your financial situation and get a lower rate. If cash-out refinancing increases your rate, it’s probably not a smart move.

You might need to pay PMI: Some lenders let you withdraw up to 90 percent of your home’s equity, but doing so might mean paying for private mortgage insurance, or PMI, until you’re back below the 80 percent equity threshold. That can add to your overall borrowing costs.

You could be making payments for decades: If you’re using a cash-out refinance to consolidate debt, make sure you’re not prolonging debt repayment over decades when you could have paid it off much sooner and at a lower total cost otherwise. “Keep in mind that the repayment on whatever cash you take out is being spread over 30 years, so paying off higher-cost credit card debt with a cash-out refinance may not yield the savings you’re thinking,” McBride says. “Using the cash out for home improvements is a more prudent use.”

You have a greater risk of losing your home: No matter how you use a cash-out refinance, failing to repay the loan means you could wind up losing it to foreclosure. Don’t take out more cash than you absolutely need, and ensure you’re using it for a purpose that will ultimately improve your finances instead of worsening your situation.

You might be tempted to use your home as a piggy bank: Tapping your home’s equity to pay for things like vacations indicates a lack of discipline with your spending. If you’re struggling with getting your debt or spending habits under control, consider seeking help through a nonprofit credit counseling agency.

A cash-out refinance might be eligible for mortgage interest tax deductions so long as you’re using the money to improve your property. Some acceptable home improvement projects might include:

Adding a swimming pool or hot tub to your backyard

Constructing a new bedroom or bathroom

Erecting a fence around your home

Enhancing your roof to make it more effective against the elements

Replacing windows with storm windows

Setting up a central air conditioning or heating system

Installing a home security system

In general, the improvements should add value to your home or make it more accessible. Check with a tax professional to see whether your project is eligible.

Is a cash-out refinance right for you?

Cash-out refinancing can be a good idea for many people.

Mortgages currently have among the lowest interest rates of any type of loan. The collateral involved — your home — means that lenders take on relatively little risk and can afford to keep interest rates low. This is especially true in today’s low-rate environment.

That means that cash out refinancing is one of the cheapest ways to pay for large expenses. Most homeowners use the proceeds for the following reasons:

Home improvement projects: Homeowners who use the funds from a cash-out refinance for home improvements can deduct the mortgage interest from their taxes if these projects substantially increase the home’s value.

Investment purposes: Cash-out refinances offer homeowners access to capital to help build their retirement savings or purchase an investment property.

High-interest debt consolidation: Refinance rates tend to be lower compared to other forms of debt like credit cards. The proceeds from a cash-out refinance allow you to pay these debts off and pay the loan back with one, lower-cost monthly payment instead.

Child’s college education: Education is expensive, so tapping into home equity to pay for college can make sense if the refinance rate is much lower than the rate for a student loan.

Both a cash-out refinance and a home equity loan allow borrowers to tap their home’s equity, but there are some major differences. As noted, cash-out refinancing involves taking out a new loan for a higher amount, paying off the existing one and obtaining the difference in cash. A home equity loan, in contrast, is a second mortgage — it doesn’t replace your first mortgage — and can sometimes have a higher interest rate compared to a cash-out refinance.

Alternatives to cash-out refinancing

In addition to a home equity loan, consider these other options:

HELOC

A home equity line of credit, or HELOC, allows you to borrow money when you need to with a revolving line of credit, similar to a credit card. This can be useful if you need the money over a few years for a renovation project spread out over time. HELOC interest rates are variable and change with the prime rate.

Personal loan

A personal loan is a shorter-term loan that provides funds for virtually any purpose. Personal loan interest rates vary widely and can depend on your credit, but the money borrowed is typically repaid with a monthly payment, like a mortgage.

Reverse mortgage

A reverse mortgage allows homeowners aged 62 and up to withdraw cash from their homes, and the balance does not have to be repaid as long as the borrower lives in and maintains the home and pays their property taxes and homeowners insurance.

Zach Wichter is a mortgage reporter at Bankrate. He previously worked on the Business desk at The New York Times where he won a Loeb Award for breaking news, and covered aviation for The Points Guy.

https://www.realestateinvestormagazines.com/wp-content/uploads/2022/05/pexels-kindel-media-7578939.jpg7201280dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2022-05-23 05:26:092022-05-23 05:26:11Cash-out mortgage refinancing: How it works and when it’s the right option

The coronavirus pandemic has affected virtually every aspect of our daily lives, from schooling to socializing to business. Since lockdowns commenced nearly a year ago, I’ve had mortgage loan officers, long accustomed to building relationships and generating leads through in-person networking, asking me how they can generate new business.

Sure, spending money on advertising is one strategy. But in a brave new world where people are spending huge amounts of time online, my advice to loan officers is this: go social like you mean it. These are my top three ways that loan officers can grow leads organically—that is, without spending a dime.

Be strategic with social media engagement.

Create quality content that people want to consume.

Present yourself in a genuine manner—i.e., be the “real you.”

Unless you’ve got a monstrous amount of time to devote to social media or the budget to pay someone else to do it for you, it’s difficult to have a huge presence across several different platforms. Instead, I tell my clients to choose one, two, maybe three social media platforms, and get really good at using those. This comes down to researching which audiences you’ll reach on different platforms and honing in on those that can be the most fruitful. Here are just two examples of how I tell clients to use the many platforms out there:

LinkedIn: While LinkedIn isn’t exclusively a B2B platform, it is the place where you’re more likely to network with referral partners, such as real estate agents and other loan officers. It’s a great place for work-related content, but posting links to shared content will actually reduce your engagement here, since LinkedIn (and Facebook) wants to keep people in the site. Instead, create short, original posts that talk about your business. This doesn’t have to be “hard sell” stuff. Try posting video or screenshot testimonials from happy clients, or you celebrating closing a loan in record time. This is called “social proof”—it’s what establishes you as a leader in your field and attracts potential colleagues and referral partners. Also, be sure to congratulate colleagues who post about promotions or job change. But go beyond a simple “Well done!” with substantive, sincere praise. “Congratulations Jan! I’ve been following your career since we worked together at ___, and it’s no surprise you’ve been so successful.”

Facebook: If LinkedIn is your office, Facebook is your living room. Use your personal Facebook page—yep, that’s right; your personal page, as it’s amazingly difficult to generate organic traffic on a business page—to share your original content on mortgage news, career wins and challenges. Intersperse these with normal Facebook stuff, whether it’s family photos or funny animal videos. When you sprinkle in the work-related posts, always think about engagement: “The Fed is threatening to raise interest rates again: do you think it’s too soon for another rate hike?” Make your non-personal posts public so that they can be shared with anyone. Accept friend requests that don’t seem sketchy or stalkerish. And engage, engage, engage.

I say it all the time and I’ll never stop saying it. When it comes to growing organic leads, it’s about quality, not quantity. Posting 60 pieces of shared content a day, regardless of the platform, is going to turn people off and make them reach for the dreaded “mute” button—and it might also get you flagged as a spammer. Instead, post original, quality, shareable content that people can use. Here are just a few ideas:

A short video (60-120 seconds is ideal) of you explaining how the mortgage pre-approval process works, or telling folks how they can improve their credit score

An attractive infographic showing the steps from loan application to closing

Remember, most first-time buyers—and a lot of second- or third-time buyers—have no clue how this stuff works. By creating content that explains the process, you establish yourself as an expert. Just don’t forget to add links to your email address and business website!

They say that all business is personal, and that’s truer now than ever before. There might have been a time when prospective loan applicants could choose from just a handful of loan officers. Now, there are more than 300,000 loan officers in the US, most of them reachable with the click of a mouse. So how do you stand out in a crowded field? Just by being you—and social media is the place to do it.

Be genuine. Share your kid’s stellar report card and your spouse’s new promotion just as readily as you do mortgage industry news. You’re a lot more than just your job, and your clients want to know that.

Engage actively, but naturally. Make a concerted effort to share and comment more on social, but don’t fake it. If you’re interested in a topic, try to generate lively discussion around it. If you’re happy for a friend or colleague’s positive news—express it!

I tell my colleagues to be themselves online and in-person, with one caveat: stay as apolitical as possible. Mortgage loans aren’t red or blue!

Building a social media presence that generates organic leads won’t happen overnight. It takes months, if not years, to create and curate quality content, build your followings and raise your profile. But when it all starts to click, it’s some of the most rewarding business you can land—and not just because it’s free. For loan officers, marketing and lead generation through social media enables you to really create a trusted brand. And the satisfaction of knowing you did it yourself, using your own initiative, creativity, and industry knowledge? That’s priceless.

https://www.realestateinvestormagazines.com/wp-content/uploads/2021/03/Luke.jpg6401080dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2021-03-26 06:37:302021-03-26 06:39:473 Ways Mortgage Loan Officers Can Grow Leads Without Spending Money on Ads

If you are planning to invest in turnkey real estate development collateralized by real property, one of the top items on your due diligence check list should be to determine which mortgage theory the state follows per the location of the subject property. This understanding can be detrimental to your recovery strategy if your borrower is unable to uphold their end of the deal and defaults on the loan. Each state adheres to either title theory or lien theory, though there are a few states that follow both. In title theory states, Deeds of Trust are the binding agreements utilized between lenders and borrowers, and Mortgages are the agreements utilized in lien theory states. Both documents serve the same purpose in a real estate deal between a lender and borrower, but how they affect the relationship between the parties involved and the subject property is what makes the big difference.

What are some similarities between Trust Deeds and Mortgages?

Mortgages and Trust Deeds both secure repayment of the loan by placing a lien on the property, and are considered, by law, evidence of the debt as they are generally recorded in the county where the property is located. If the borrower defaults on the loan and the lien is in first position, the lien gives the lender the right to take the property back through foreclosure and sell it. In other words, both Mortgage and Trust Deed documents are used as leverage to ensure the borrower pays back the loan in full. The ability to sell the property gives real estate investors and lenders the potential to recoup the original principle lent on the loan. Depending on the value of the property, there is the potential for the recovery of back due interest, late fees, and even capital gain.

What are the main differences between Trust Deeds and Mortgages?

Number of Parties

A Mortgage involves two parties: a borrower (the Mortgagor) and a lender or investor (the Mortgagee). A Trust Deed involves three parties: a borrower (the Trustor), a lender or investor (the Beneficiary), and the title company or escrow company (the Trustee). The Trustees main functions are to hold the title to the lien for the benefit of the Beneficiary and to initiate and complete the foreclosure process for the Beneficiary in the case of default by the Trustor.

Property Title & Foreclosure Processes

The main difference between Trust Deed and Mortgages is who holds the title to the property encumbered by the loan for the duration of the loan term. In a Mortgage State, the borrower holds the title of the property. Therefore, if the borrower defaults on the loan, the lender must go through the courts to take back the property through foreclosure. This is known as judicial foreclosure and this process involves the lender filing a lawsuit against the borrower. This can be a costly and time-consuming process for both parties involved.

In a Trust Deed State, court can be bypassed because the Trustee holds the title to the property. You would follow the non-judicial foreclosure process, which almost always results in faster execution and resolution for all parties involved, especially for the lender. The speed of foreclosure can be detrimental to minimizing carrying costs and getting the property on the market quickly to sell in what may be a more promising market than one met at a later date.

A First Trust Deed is as it implies, is recorded first before any other financial liens on the subject property, whether they be secondary mortgages, trust deeds or even mechanics liens placed by subcontractors. This means the First Trust Deed holds a priority or “senior” position, making all other liens encumbered by the loan subordinate or “junior” to the senior loan. Obtaining first position is important because in a foreclosure scenario, all outstanding subordinate liens are eliminated. This makes it so the lender does not have to worry about reconciling those other debts on top of their own.

Why invest in First Trust Deeds?

Hard money lenders like Ignite Funding, tend to operate more in Trust Deed states. First Trust Deed investments offer an attractive yield with relatively low risk to Ignite Funding investors due to their senior lien position on the property and the foreclosure process that is more conducive to the investors who are the Beneficiaries on the loan. This allows investors to earn double digit annualized returns paid as a monthly fixed income with REAL property as their collateral.

If you are interested in becoming a Trust Deed investor or want to learn more, you can schedule a FREE consultation with an Investment Representative, please click here.

Ignite Funding, LLC | 2140 E. Pebble Road, Suite 160, Las Vegas, NV 89123 | P 702.739.9053 | T 877.739.9094 | F 702.922.6700 | NVMBL #311 | AZ CMB-0932150 | Money invested through a mortgage broker is not guaranteed to earn any interest and is not insured. Prior to investing, investors must be provided applicable disclosure documents.

https://www.realestateinvestormagazines.com/wp-content/uploads/2020/12/scale-2635397_1280.jpg7111280dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2020-12-17 05:02:372020-12-17 05:02:56Trust Deeds vs Mortgages: What’s the Big Difference?

With the Covid crisis still looming, much attention has been focused on conventional loans where monthly mortgage payments are required. Recently, laws have been passed on both local and national levels to ensure homeowners are not evicted for non-payment on FHA loans.

Relatively little attention has been geared toward reverse mortgages during the Covid virus. Why is that? At first glance, the simple answer is that no monthly payments are required for reverse mortgages; thus, there is no risk for a foreclosure for non-payment of a mortgage. However, one needs to go deeper to understand that there could be a potential risk to the homeowner of losing their house in certain circumstances but for the foreclosure moratorium.

Image by fernando zhiminaicela from Pixabay

Under normal circumstances, the borrower on a reverse mortgage does not have to worry about foreclosure by the lender because no monthly payments are required; the loan balance just keeps increasing as interest accrues over time and is only required to be paid back upon the death of the last remaining borrower, move out by the borrower, or death of the non-borrowing spouse if the borrowing spouse predeceased them. The borrower’s only requirement for yearly payments are real estate taxes and insurance, HOA dues if applicable, plus maintenance and utilities. If the borrower fails to pay these, technically, they are in default and the loan may be called. This could lead to a foreclosure. In addition, the house may not be left vacant or abandoned.

For those borrowers who take a lump sum reverse mortgage and whose income is estimated to be too low to maintain the real estate taxes and insurance, they may be required to have a Life Expectancy Set Aside [LESA]. LESA is similar to an escrow account that is set aside for future real estate taxes and insurance and is based on the life expectancy of the borrower. These future expenses are deducted from the lump sum provided by the reverse mortgage company and held by them. The funds in the LESA become part of the loan balance once the lender disburses them to pay the property charges on behalf of the borrower. Thus, those borrowers who have LESA, for all intents and purposes, would not typically face foreclosure during their expected lifetime.

Many conventional borrowers have requested deferments from their lending institution as they fell on hard times with the loss of income during Covid. The need for deferment requests are all but eliminated for reverse mortgages.

There has been a tremendous push toward applying for reverse mortgages by homeowners. There are many reasons for this; historically low interest rates mean that a borrower can obtain a much larger reverse mortgage, as the interest that gets added to the mortgage every year is less than in a high interest rate environment. Thus, the lower the interest rate, the better it is for the homeowner and, consequently, the less risk for the mortgage company.

In addition, many older homeowners have lost their job during the virus, and their largest retirement asset, by far, is their home equity from which they can draw upon. These same homeowners not only may not qualify for a HELOC [Home Equity Line of Credit], they may not want them after considering the benefits of a reverse mortgage (HECM) vs. a HELOC. For one, HELOCs require monthly mortgage payments. In addition, unlike a reverse mortgage (HECM), the bank can freeze [or reduce] the HELOC line and not allow access to it. This puts the homeowner in a precarious position of having debt against their property [as the HELOC is recorded against the property for the maximum potential draw of the line] without any benefit. Such was the case during The Great Recession in the mid-late 2000s when $6 billion of HELOC credit was frozen in June of 2008, and the freezing continued for some time. Why? The answer lies in the fact that the fastest way for a bank to shore up its balance sheet is to freeze HELOCs, so they do not have to set aside reserves. During The Great Recession, banks were facing write downs and write offs of loans as the loans that they had previously written took a downturn when borrowers, during the credit crisis, were unable to pay their mortgage. When a bank makes loans, they use depositors’ funds. The government requires reserves [loan loss reserves] be set aside to ensure the return of those depositors’ funds. If a bank has existing loans outstanding, they cannot just call in those loans [unless borrowers default]; however, a HELOC is a “potential loan” as the loan technically only exists as the borrower draws upon it. In this situation, if they freeze [or reduce] the line, the bank has not lent the money yet and can stop it before the borrower accesses the money that was available to them.

Most major banks have seriously curtailed the issuance of HELOCs during the current Covid crisis, and those that continue to offer HELOC’s have imposed stringent qualifications to borrowers.

Many borrowers are realizing reverse mortgages offer advantages over HELOCs in this regard. There are limited income and credit qualifications to obtain a reverse mortgage. Reverse mortgage (HECM) lines of credit cannot be frozen or reduced, and, since there are no monthly mortgage payments, the risk of foreclosure [even after the moratorium] is slim.

A new situation has arisen due to Covid and that has to do with nursing homes. Once considered an alternative to in-home care [which is usually two to three times the cost of a nursing home], many stories have been published about the increase in deaths surrounding Covid and older Americans in care facilities. Most people would like to be in their own home instead of a care facility given the choice, but, unfortunately, many people cannot afford the [around the clock] care required to stay home and be cared for. Loved ones, especially during the virus, are looking for a way to keep their elders in the safety of their own home and receiving the quality and quantity of care they needed. Many are looking toward a reverse mortgage to fill this need. Many people have enough equity in their homes, especially as real estate has tremendously rebounded since The Great Recession, to allow them a large enough reverse mortgage to afford the costs associated with in-home care.

Image by Tumisu from Pixabay

The National Reverse Mortgage Lenders Association [NRMLA] reports that there have been significant increases in draws [on the HECM reverse mortgage line of credit]. Those retirees who lost their part time jobs and need to make ends meet, helping family affected by Covid, and those who are just generally concerned about their future finances. NRMLA states there has been a 55% increase in the number of draws and 14% in the size of the draws. In fact, they notice that some borrowers who had never previously drawn on their line of credit are fully drawing the line now.

As Covid gets more impactful on the economy and on peoples’ lives in general, we should expect reverse mortgages to grow, and now seems to be the most opportune time to obtain one – before interest rates increase.

Edward Brown

Edward Brown currently hosts two radio shows, The Best of Investing and Sports Econ 101. He is also in the Investor Relations department for Pacific Private Money, a private real estate lending company. Edward has published many articles in various financial magazines as well as been an expert on CNN, in addition to appearing as an expert witness and consultant in cases involving investments and analysis of financial statements and tax returns.

https://www.realestateinvestormagazines.com/wp-content/uploads/2020/09/covid-19-business.jpg6651280dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2020-09-10 04:46:162020-09-10 04:46:16The Effects from Covid on Reverse Mortgages

According to Investopedia, Unrelated Business Taxable Income [UBTI] is income regularly generated by a tax-exempt entity by means of taxable activities. This income is not related to the main function of the entity and prevents or limits tax-exempt entities from engaging in businesses that are unrelated to their primary purposes.

UBTI greater than $1,000 is subject to taxation. For 2019, the highest tax rate was 37%.

Most forms of passive income, such as dividends, interest income, and capital gains from the sale of capital assets, are not treated as UBTI.

Many investors use their IRAs to invest in Mortgage Debt Funds [MDF]. MDF lend money similar to a bank where they take a deed of trust as collateral for the loans they make to borrowers. Typically, income derived from MDF are not subject to UBTI even though the income derived at the MDF level is not passive in and by itself. The IRA investor, however, is a passive investor; consequently, it is not usually subject to UBTI. There are times, however, when this is not so.

Ways that UBTI can be triggered for the investor in a MDF can involve a few different scenarios; if the IRA borrows on margin to purchase the MDF; if the MDF borrows within itself to generate income [called a leveraged MDF], or if the MDF ends up foreclosing on too many assets and the IRS treats the MDF as a dealer in real estate. [This last risk is relatively small, as most MDFs would not be treated as being in the business of buying and selling real estate by the IRS under normal circumstances]. The first risk [the IRA borrows to invest in the MDF] is also not a normal risk, and the investor has control over this by not borrowing to invest in the MDF]. It is the second risk that is the main one, as the MDF controls how much [if at all] it borrows.

Most MDFs that use leverage usually center around attempting to enhance its yield to investors. If the MDF can borrow from a bank at 5% and lend it out at 8%, there is a 3% arbitrage in favor of the MDF; however, this may possibly put undue risk in its portfolio – depending on how much leverage is used and the bank covenants required to obtain this leverage. In addition, for those investors in the MDF who use their IRAs [or 401(k)s, pension, or profit-sharing plans], this leverage may subject the income derived to create UBTI.

Certain key factors for the investor’s IRA are; how much the IRA has invested in the MDF [because the first $1,000 of UBTI is not taxable to the IRA, the income derived by the MDF, and how much leverage was used to produce that income. In addition, it is important the length of time that leverage was used, as the UBTI will be calculated using a formula.

For example, Chart 1 shows an IRA investor having $100,000 in a MDF generating a rate of return of 6.5% [without leverage] will not have its $6,500 income subject to UBTI as no leverage was used. If the MDF chooses to leverage the Fund 50% [50% investor funds and 50% bank funds] for the entire year and can borrow at 5% and invest that portion at 8%, the net income to the IRA [after subtracting the bank interest expense and UBTI tax ] would be $8,760.

Many IRA investors may not feel that the extra $2,760 earned in this example is worth the risk. When a real estate syndication goes bad, it is usually only for one reason – leverage. If no leverage is used, then, usually, the only way for a real estate investor to lose substantially most or all of his/her investment in these types of investments [be they REITS, Limited Partnerships, Limited Liability Companies, etc.] is if the real estate taxes associated with the underlying real estate are not paid. When leverage is used, the banks have first priority over the assets. Simply, the more leverage that is used, the riskier the investment.

It is important for those investors using their retirement savings to invest in assets that can produce UBTI to ask the manager how much debt/leverage is used in the investment. A small amount of leverage is not usually taking on undue risk, especially if that leverage is used sparingly. Mark Hanf, president of Pacific Private Money, says that he likes to use a small amount of leverage, and on a very short term basis for his MDF for specific reasons; mostly, to help fund short term loans in his Fund when he is expecting payoffs on other loans or anticipated investor money flowing in. As soon as payoffs or investor money comes in, he immediately pays down line of credit [leverage]. This creates the benefit of having the ability to close deals that he might not otherwise have been able. The short-term nature of this leverage does not usually create enough UBTI income to concern the retirement investor. In addition, the short duration of the leverage puts his Fund at minimal risk; however, since the rate of interest to obtain the leverage is less than the income derived from it, his Fund still benefits from a small amount of positive arbitrage.

The retirement investor would be wise to look for Funds that conservatively use leverage in their MDF to avoid UBTI as well as undue risk. In addition, the investor should calculate the anticipated UBTI ahead of time to determine how much should be invested, as only the first $1,000 of UBTI income is tax free; The investor can then decide the risk reward of investing in a MDF that uses leverage.

Edward Brown

Edward Brown currently hosts two radio shows, The Best of Investing and Sports Econ 101. He is also in the Investor Relations department for Pacific Private Money, a private real estate lending company. Edward has published many articles in various financial magazines as well as been an expert on CNN, in addition to appearing as an expert witness and consultant in cases involving investments and analysis of financial statements and tax returns.

https://www.realestateinvestormagazines.com/wp-content/uploads/2020/09/financial-5050415_1280-attribute.jpg8261280dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2020-09-01 05:25:092020-09-01 05:25:09UBTI and Mortgage Debt Funds

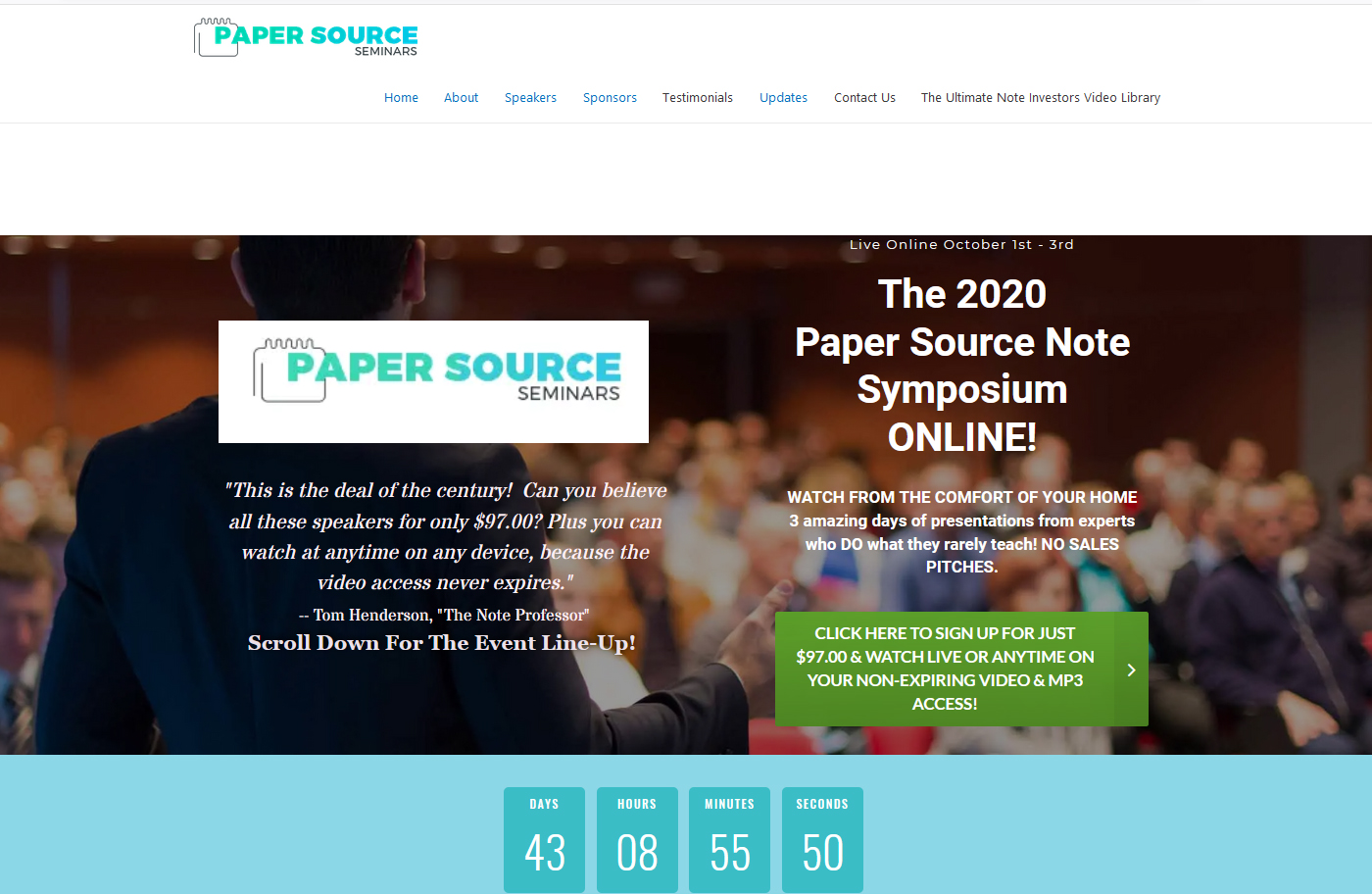

Savvy real estate investors balance their portfolio with real estate notes (trust deeds or mortgages); real estate for appreciation, real estate notes for income.

My name is Bill Mencarow. While my wife Alison and I were on the staff of the US Congress in Washington, we started to invest in real estate and later discovered notes (trust deeds and mortgages). We still love real estate, and since then we’ve bought and sold lots of it, and lots of notes.

We then started The Paper Source, an educational resource for note investors and those who want to be. For many years we have hosted the annual Paper Source Note Symposium which attracts several hundred investors.

Because of virus restrictions we can’t hold it live this year. Instead, it will be at your house! (That is, it will be online.)

* Our speakers are people who DO what they teach. Over three days you will learn from some of the most experienced people on the planet (full-time note investors, tax and asset protection attorney, self-directed IRA experts, to name just a few) – and absolutely NO sales pitches.

* There will be presentations for beginners on up.

* You will get NON-EXPIRING access to all the speakers’ videos and MP3 audios.

Tom Henderson, whom many call “The Note Professor” (and you will too, once you hear him) recently told me, “Bill, this is the deal of the century! Can you believe all these speakers for only $97.00? And be able to watch at anytime on any device?!”

This is my invitation to join us for the online Note Symposium Oct. 1-3. Please CLICK HERE to see all that it offers. The $97.00 registration includes admission to the event and lifetime access to the videos and MP3s.

And that’s not all. If you register by this Friday, Aug. 21, you will receive a one year subscription (or renewal) to THE PAPER SOURCE JOURNAL, the only publication for real estate note investors, which sells for $79.00.

Every month you’ll get news affecting your investments, including court decisions, scam warnings, tips and techniques on everything from finding notes, negotiation, recasting them to double and triple your yields, and much more.

Cheers,

Bill

W. J. Mencarow, President, The Paper Source, Inc.

Remember to register by this Friday to receive the $79 bonus. Your registration includes access to all the speakers’ videos and MP3 audios which will NEVER expire – you will be able to watch and/or listen anytime now or in the future. CLICK HERE for more information and to register. And please don’t miss the Friday deadline!

Feel free to contact me with any questions. My personal email is[email protected] and my cell is 830-285-5926.

https://www.realestateinvestormagazines.com/wp-content/uploads/2020/08/pexels-black-ice-1314544.jpg8531280dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2020-08-19 05:21:252023-04-10 03:52:37Don’t Miss The Deadline To Balance Your Real Estate Portfolio