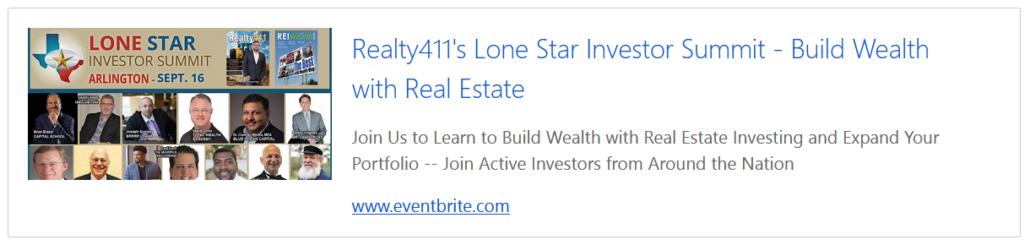

We are excited you can share the day with us this Saturday, Sept. 16th, for the Lone Star Investor Wealth Summit.

Be sure to arrive early to get the best seating — a few VIP tickets are also still available for purchase to upgrade your seating, see link below.

ALSO: We added a few complimentary tickets for you to bring a guest!

But hurry, because only a few remain, thank you. Also, parking is FREE so don’t worry about that either.

This is the event you’ve been waiting for! Get ready to expand your portfolio and connect with active investors from around the nation.

Whether you’re a seasoned investor or just starting out, this summit is designed to provide you with the knowledge, strategies, and networking opportunities you need to succeed in the real estate market.

Don’t miss out on this incredible opportunity to learn from industry experts, gain insights into the latest trends, and discover the secrets to building wealth through real estate investing. Plus, there will be plenty of time to mingle with like-minded individuals and form valuable connections that can take your investments to new heights.

NEED MORE TICKETS?Click the link below to reserve your seat today.

Enjoy a day of learning and networking. Our educators include:

* Chander Mishra MD MBA CPE FASE FASA FAACD – Blue Ocean Capital * Bob Bluhm, Esq — Asset Protection Attorney & Public Speaker * Brad Blazar – Founder of Capital School – Raised Over $2B in Private Capital * Joseph Kimbrough- Apex Real Estate Investments * Brian Carlson – Subject-To Real Estate Academy * Joseph V. Scorese – BRRR Loans * Steve Davis – Total Wealth Academy * Jimmy Reed – 1REclub.com * Jonah Dew – The Money Multiplier * Jim Edenfield – Invest Success * Tim Emery – Great Mile High Investor Summit * Arnie Abramson — Texas Tax Sales * Joel M. Desilets – Damascus Partners, LLC * Seth Desilets – Damascus Partners, LLC * Paul Finck, The Maverick Millionaire ® * AND MANY MORE!

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/09/Lone-Star-Investor-Summit.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-09-14 03:58:472023-09-14 03:58:51Lone Star Wealth Summit Information — See YOU Soon!

What you avoid in life controls you, so you must confront it or attack it head on for the pain and fear to dissipate.

At our true core, we have just two root emotions – love and fear. All other feelings are just other sides or aspects of love (compassion, generosity, trust, empathy, etc.) and fear (guilt, shame, anger, envy, greed, etc.). As it relates to money, most people quickly react with fear when making financial decisions with a “fight-or-flight” type of fearful reaction.

Many people, sadly, freeze up with “deer-in-the-headlights” type of looks and do nothing until it’s too late. If so, the months or years of stress holds them back like an anchor and the financial trauma may continue to worsen.

Fight: Medical bills and divorce are the two main causes of financial insolvency and bankruptcy here in the US. Many times, the main argument point between once loving spouses is about household debt.

Flight: The most common reaction is to avoid the debt anchor topic partly by way of seeking out addictions (drugs, booze, excessive spending) to numb our emotions and not to think about it too much. In the short term, it may be helpful. However, it can crush you emotionally, physically, and financially in the long term.

Freeze: The proverbial “deer-in-the-headlights” is perhaps the most destructive reaction of them all. While being frozen with fear, the oncoming figurative car or train in the tunnel may eventually run you over and cause a heart attack, stroke, horrific addictions, broken relationships, or suicidal tendencies. At the same time, the maxed out credit card lenders may later start a credit freeze on the person’s account or drop their balances down to near zero.

Be Proactive, Not Reactive

Our nation is built on the issuance of credit and debt. Many times, the debt like seen with mortgages later helps us create the bulk of our net worth with increased equity gains in our real estate holdings. As such, mortgage debt can be viewed as a more positive type of debt than credit cards with an APR (Annual Percentage Rate) which can be as high as 25% to 35%+ after factoring in annual fees.

First and foremost, please write down your true monthly budget if you’re interested in reducing your debt and increasing your overall net income at the same time. Most people may think that they’re spending $3,000 per month when they’re more likely spending more than $5,000 while living off of their credit cards.

While rates have risen at a fast pace for mortgages and credit cards, payday and pawn shop loans can vary between a 300% and 500% APR while making mortgage and credit card rates seem incredibly cheap by comparison.

Between 2006 and 2014 during the depths of the Credit Crisis, there were 10 million Americans who lost their homes to foreclosure over this 8-year span. Within just a few months in 2020 (March to May), we saw almost 50% of that 10 million foreclosure number with at least 4.7 million mortgages delinquencies. However due to the pandemic designation moratoriums, a near historically low percentage of delinquent mortgages had foreclosure filings. At some point, lenders and mortgage loan servicing companies will accelerate their foreclosure filings.

To Refinance Consumer Debt or Not

A high percentage of homeowners and real estate investors these days are equity rich in their homes while cash poor. In addition, they may be paying the highest amount of monthly debt ever in their entire life partly since we’re truly facing the highest inflation rates ever in our nation’s history and the most unaffordable housing market for both buying and leasing.

A recent small business owner survey completed by Alignable that was published on August 31, 2023 was truly shocking about how far that small business income has fallen. The survey found that a whopping 50% of surveyed small business owners responded that they are only making half or less of what they were earning prior to the pandemic declaration back in March 2020. Please support your local small businesses more so than the global corporations so that they can remain in business.

To simplify, I will just focus on the monthly payments and not the overall consumer debt principal amount which may be close to $200,000 combined. In this example, the borrower only has two months’ worth of cash reserves near $9,500 in liquid funds at his or her bank.

article continues after advertisement

Let’s quickly look at a fictional borrower with a $400,000 mortgage and a California home valued at $1,000,000:

$400,000 – 1st mortgage at a 3% rate: $1,686/month (not including taxes and insurance)

Student loan debt: $900/mo.

Automobile loan: $1,020/mo.

Monthly credit card payments: $600/mo.

Unsecured small business loan: $500/mo.

Total monthly payments: $4,706/mo.

The borrower not only needs to reduce their household’s monthly expenses, they also need to replenish their savings so that they don’t run out of cash. Without money on hand, they might default on their mortgage, credit cards, automobile loans, student loans, and debt and lose their hard-earned equity in their home to foreclosure.

The new mortgage refinance option offered to the homeowner with or without full income verification might be near a 70% loan-to-value (LTV) in this fictional example with a fictional lender. If the home does appraise at $1 million dollars, this would equal a new $700,000 cash-out loan.

The client is focused on lowering monthly payments, so he selects a shorter term fixed rate mortgage that’s fixed for 7 or 10 years before converting to an adjustable rate mortgage. This same loan allows much lower interest-only payments at 7% (8.25% APR – all rates are subject to change).

Out of this new cash out refinance, the client’s new $700,000 loan may pay off all of their household’s monthly debt and add another $100,000 in cash to their savings accounts. With a new shorter term interest-only rate at 7%, the monthly payment may be near $4,083. When comparing the previous monthly payment debts of $4,706, it’s $623 per month less and provides potentially increased mortgage interest tax deductions at the same time. All other consumer debt balances are now at ZERO.

The 7-Year Mortgage Average

Homeowners and investors may choose to pay off more expensive consumer debt with a cash-out refinance by way of a new 1st, 2nd, or reverse mortgage with no monthly payments. Here are some of my previous article links about how to convert home equity to cash and the benefits of reverse mortgages with no monthly payment obligations: Converting Home Equity to Cash and Moving Forward with Reverse Mortgages.

The average length of time that a property owner holds their mortgage loan before later selling or refinancing is seven years. Property owners also own their properties on average about seven years as well. If so, a 7-year fixed mortgage rate that’s interest-only with much lower monthly payments might be an exceptional option for many borrowers.

With a 30-year fixed rate mortgage, the principal amount doesn’t really begin to reduce or amortize down until after the same 7th year term anyway. Or, your original principal balance on your mortgage on the day you closed escrow may be very similar to the same balance amount seven years later. This is partly why more borrowers are choosing shorter fixed rate terms of 3, 5, 7, or 10 years that may also have interest-only payment options that are much lower than a fully amortizing mortgage which includes both principal and interest.

The monthly payments on an interest-only shorter-term mortgage can be similar to a 30-year fixed mortgage rate that’s almost equivalent to a rate of 2% lower than some of the best 30-year fixed rates today.

At a later date, if and when the housing market bubble pops again, the Federal Reserve may suddenly and very aggressively cut rates back down to near historical lows once again after the economy possibly takes a turn for the worse like following 2008.

Credit and Debt – Worldwide, US, & Consumers

The U.S., with 4.5% of the world’s population, creates 25.5% of the world’s gross domestic product (GDP).

2023 Equity, Money, and Debt Data

* Global Derivatives: $3,000+ trillion * Forex (Foreign Exchange Currency Market): $2.409 quadrillion ($7.5 trillion traded daily) * US bond market cap: $52.9 trillion * US stock market cap: $46 trillion * U.S. federal debt: $32.6 trillion (August ’23) * All US mortgage debt combined: $19.4. trillion (1st quarter ’23)

Housing and consumer debt trends:

* 140 million housing units in America. * 64.8% of homes have a mortgage (96,320,000). * 31.2% of homes have no mortgage (43,680,000). * 1.7 million housing units under construction. * 44 million rental units across the nation. * 80% of retirees own a home while nearly half live near poverty. * Credit card rates today average 25% as compared to 12% in 2008. * Today’s 30-year fixed mortgage rates are at a 22-year high. * U.S. credit card debt – $1.2 trillion * U.S. auto loans – $1.56 trillion * U.S. student loans – $1.77 trillion

article continues after advertisement

Household Income and Mortgage Debt Numbers

* House payment as % of median household income in Los Angeles County: 80.59% * House payment as % of median household income in California: 65.19% * Mortgage debt by state (1st quarter 2023): 1. California: $2.3 trillion; 2. Texas: .88 trillion; and 3. Florida: .85 trillion * California’s total unpaid mortgage debt is almost three times more than Texas with only a 25% larger population base.

Rising Consumer Debt & Imploding Savings

The average credit card balance per U.S. consumer is $5,733, according to CNBC. Back in 2008 when the average credit card rate was 12% near the start of the Credit Crisis, it would take 5 years and 10 months to pay off the balance in full if the borrower paid the minimum monthly payment. If so, the borrower would pay approximately $2,243 in additional interest. By comparison here in 2023 after a series of rate hikes, the average credit card rate is 23.99%. It will now take upwards of 24 years to pay off the debt in full with minimum monthly payments while accruing more than $27,337 in additional interest over and above the original $5,733 balance.

Crashing car market: The average car loan balance in the U.S. as of the 1st quarter of 2023 was 125% loan-to-value (LTV), as per TransUnion. The average new car price today is about $48,000. The average new car payment is $731 per month and the average used car payment is $551 per month. The average new car rate is now 9.48%, which is a multi-decade high.

The cumulative excess U.S. household savings dollar amount fell from a peak high of $2.1 trillion in August 2021 down to $91 billion in June 2023, as provided by JP Morgan Macro Research. The average U.S. homeowner has the bulk of their net worth tied up as untapped equity in their primary home.

There’s an estimated $10.5 trillion dollars’ worth of tappable equity in residential properties nationwide. The average homeowner has almost $200,000 in home equity.

Skyrocketing Energy & Inflation

We have a petrodollar (“oil for dollars”) currency system. As our oil supply declines, so does the purchasing power of our petrodollar while inflation skyrockets right alongside interest rates. Generally, energy costs are the root cause of core inflation trends, so keep a close eye on this developing story.

Oil prices per barrel are near $87 for WTI (West Texas Intermediate). By comparison in July 2008 shortly before the financial system almost imploded in late September 2008, oil prices were trading as high as $147 per barrel. As our oil supply continues to be reduced here in the US and elsewhere in Saudi Arabia, Russia, and Venezuela, demand may exceed supply and prices may rise up even more.

There are rumors of oil prices rising again very soon well above $100 per barrel. If so, the one investment that has consistently benefited from rising energy and overall inflation trends is real estate.

Sadly, a $1 back in 1933 would have the same purchasing power as 4 cents today.

Are Home Prices Peaking or Declining?

The average mortgage rate for existing mortgage loans across the nation is about 3.6%. If so, this is under half of the most recent average 30-year fixed mortgage rates. Yet, today’s higher 30-year fixed mortgage rates are only about 30% as high as the average credit card rate near 25%.

For the first time in U.S. history, median new home sale prices are about to fall below existing home prices. With a record 1.7 million new housing units being built this year, home builders must slash prices and offer significant amounts of seller credits to the buyers to sell their properties. Unlike the millions of older distressed shadow inventory that owners, lenders, and loan servicing companies can attempt to keep postponing for sale, builders have to offer these completed homes for sale as soon as the Certificate of Occupancy is received.

In the near future, home values may start to fall yet again like in past housing bubble bursts. A recent video provided by the brilliant folks at the National Real Estate Post makes the claim that today’s housing bubble may potentially be more than twice as large as the previous housing bubble near the peak highs in 2007 and 2008. If so, home prices may be peaking in certain regions if you’re thinking about selling or refinancing at the top of the market.

No matter what you decide to do with real estate and with life, the most important step is the very first one because action is much better than inaction.

Rick Tobin

Rick Tobin has worked in the real estate, financial, investment, and writing fields for the past 30+ years. He’s held eight (8) different real estate, securities, and mortgage brokerage licenses to date and is a graduate of the University of Southern California. He provides creative residential and commercial mortgage solutions for clients across the nation. He’s also written college textbooks and real estate licensing courses in most states for the two largest real estate publishers in the nation; the oldest real estate school in California; and the first online real estate school in California. Please visit his website at Realloans.com for financing options and his new investment group at So-Cal Real Estate Investors for more details.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/09/fear.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-09-13 04:09:222023-09-13 04:09:27Credit Fears – Fight, Flight, or Freeze

Are you ready to grow your real estate portfolio to brand new levels of abundance? If so, be sure to join us for Realty411’s NEW Lone Star Wealth Summit.

We are hosting a Real Estate Wealth Summit & Special In-Field Bus Training in Arlington, Texas, on September 16th & 17th.

This Extra-Special Summit will cover a wide range of real-estate investing topics, as well as focus on individual mindset, finance and leverage, maintaining motivation and joint collaborations with our “Inner Circle” of readers, subscribers and educators.

Network with high-level investors and learn from top REI educators and accredited investors. Our speakers have collectively raised billions in private capital for their real-estate investment acquisitions.

This is your opportunity to learn directly from the best in REI in the Lone Star state and beyond, don’t miss it.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/09/Investor-Summit.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-09-12 02:24:072023-09-26 05:02:03Join Us for Realty411’s Lone Star Investor Wealth Summit

The way you handle the media is the key to achieving desired success. They are finicky. Aim for the headlines. Jill Lublin has the inside scoop on what makes the media smile and what makes them cringe.

article continues after advertisement

15 things the media hates:

1. Not take “no” for an answer 2. Long news releases 3. Lying, hype, and misrepresentations 4. Lack of Preparation 5. Small Talk 6. Overkill 7. No repeated cold calling 8. Freebies 9. Name dropping 10. Lack of focus 11. Confirmation calls 12. Gimmicks 13. Not following up requests 14. Same ideas 15. Getting upset

15 things the media loves:

1. News 2. Brevity – Be Clear 3. Knowing targets 4. Relationships 5. Preparation 6. Broad appeal 7. Ties 8. Experience 9. Visualization 10. Celebrity tie-ins 11. Prompt response 12. Courtesy 13. Visual aids 14. No road blocks 15. A pleasant attitude

article continues after advertisement

Jill Lublin is an international speaker on the topics of Radical Influence, Publicity, Networking, Kindness and Referrals. She is the author of 4 Best Selling books including Get Noticed…Get Referrals (McGraw Hill) and co-author of Guerrilla Publicity and Networking Magic. Her latest book, Profit of Kindness went #1 in four categories. Jill is a master strategist on how to position your business for more profitability and more visibility in the marketplace. She is CEO of a strategic consulting firm and has over 25 years experience working with over 100,000 people plus national and international media. Jill teaches Publicity Crash Courses as both live events and live webinars and consults and speaks all over the world. She also helps authors to create book deals with major publishers and agents, and well as obtain foreign rights deals. Visit publicitycrashcourse.com/freegift and jilllublin.com

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/09/love-hate.jpg5001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-09-11 03:54:262023-09-11 03:54:30SPECIAL REPORT: The Do’s and Don’ts of Media Follow-Up – 15 Things the Media Loves / Hates

ORLANDO, FL – New Home National Title, a forward-thinking company transforming the real estate industry with cutting-edge technology and services, is excited to announce its upcoming feature on the Boom America TV show hosted by the iconic Kevin Harrington. Boom America is a distinguished platform that spotlights groundbreaking companies and their influential innovations. The feature of New Home National Title emphasizes its game-changing approach to real estate transactions, particularly its emphasis on mobile earnest money delivery and cryptocurrency payments.

article continues after advertisement

New Home National Title is spearheading advancements in the real estate sector by providing seamless and faster closing processes through its state-of-the-art technology. This includes unique features like mobile earnest money delivery and the acceptance of cryptocurrency payments, offering unparalleled convenience in home purchases. The company’s robust suite of title and escrow services cater to both residential and commercial sectors, making them a trusted ally for leading real estate and banking institutions nationwide.

“Being showcased on Boom America is a significant achievement,” said Richard Simon, owner & founder of New Home National Title. “We’re eager to introduce our modern and innovative approach to real estate transactions to a wider audience, inspiring more individuals and businesses to experience the unmatched efficiency and dedication we bring to each deal. Through our feature on Boom America, we aim to highlight how New Home National Title is setting new standards in the real estate sector.”

The feature of New Home National Title on Boom America reinforces its leadership position in the real estate industry. With its commitment to innovation, personalized user-friendly service, and a seasoned team of real property experts, New Home National Title is redefining the experience of real estate transactions. Their mission of infusing a personalized touch into every deal, regardless of its scale, underscores their customer-centric philosophy.

New Home National Title is disrupting the real estate market by using the most advanced and secure technology to streamline the closing process, including mobile earnest money delivery and crypto currency payments, making home purchases faster and more efficient than ever. New Home National Title offers a full slate of title and escrow services for both residential and commercial markets and is a trusted partner to the top real estate and banking organizations throughout the country.

Boom America is a life-changing show hosted by none other than the legendary Kevin Harrington. A pioneer of the infomercial industry and an original star of the hit TV series Shark Tank, Kevin leads a powerhouse team of business experts on a mission to take various innovative companies to new heights. The real work begins as the chosen companies embark on a journey of explosive growth, guided every step of the way by the seasoned professionals of Kevin’s team. Get ready for a game-changing ride in 2023!

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/09/New-Home-National-Title.jpg5001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-09-08 04:35:292023-09-08 04:35:34Boom America TV Show Highlights New Home National Title: Revolutionizing Real Estate Transactions

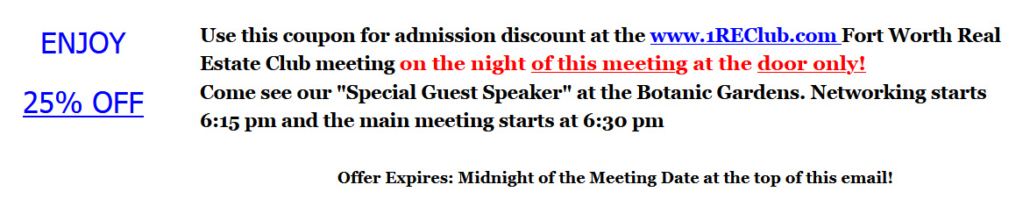

Come Network Thursday September14, 2023 6:15 PM at the Fort Worth Real Estate Club with us and our Guest Speaker. Linda Pliagas

Real Estate Generational Wealth!

And the Realty 411 Expo on Sept 16th in Arlington, TX.

LINDA PLIAGAS, CEO, REALTY411 .COM

Linda Pliagas is the CEO and publisher of Realty411, which she founded in 2007. Linda has personally owned and managed rental properties in five states, all by the age of thirty-eight. Linda and her husband have purchased single family homes, multifamily units, vacation rentals, probates, REOs, and short sales. She has worked simultaneously in media and real estate for decades.

She holds a bachelor’s degree in print journalism from California State University, Long Beach. She was a recipient of the Bobit Magazine Scholarship for her accomplishment in publishing her first national magazine while still at CSULB. She also studied real estate, accounting, and general studies at Santa Monica College. As a journalist, Linda has freelanced for numerous national magazines, local newspapers, and global websites. Her mission is to empower average Americans to build generational wealth for their families by investing in real estate. Her website is Realty411.com.

Some of the things Linda will be Talking on at this Event:

We will be doing this Meeting Interview Style!

The Interviews have been such a Favorite of Attendees we are doing it again.

We will have Questions about Generational Wealth via Real Estate

What to Expect at the Expo 2 Days after this meeting.

How to Get Started investing on the Fast Track!

How to get the Most out of the Expo & the Power of Networking at the Expo.

The 411 & REI Magazines that can help you succeed with a Coast to Coast Network.

Marketing in those Magazines for Success!

And so Much More!

Bring your Questions you need Answers to!

Be Prepared to take a lot of Notes!

If you are not a Member read below on how to become one, and then watch the meeting any time along with other meetings since April of 2020.

There are only 2 ways for you to hear this information packed segment.

Becoming an Annual Member to watch it online from the comfort of your Home OR

Coming out to our in Person Meeting at the Botanic Gardens!

YES WE ARE BACK!!! LIVE COME OUT & NETWORK!!!

New Schedule!!! Doors open at 6:15pm Main Meeting Starts a 6:30 Sharp and ends at 8:30, Then More Networking after the Meeting!

For the Fort Worth / DFW Area Real Estate Investors Club’s Monthly meeting at the Fort Worth Botanic Gardens.

Networking with local investors starts at 6:15 pm and the Main meeting starts at 6:30 pm. Come out and meet our Preferred Vendors and let them answer any questions you have about real estate investing.

*So come out and bring plenty of business cards, flyers, anything you need to network! Also if you have properties for sale then make sure to print up some info sheets on them and put them on our “Deal Table” each month along with your Networking Materials!

NOW!! just $20 to attend & Memberships are available at a discount! The club is all about providing value, which is why we bring in vendors and speakers who are here to make your life as an investor easier and more lucrative.

If you are Serious about Real Estate Investing then you need to attend this Real Estate meeting at the Botanic Gardens.

See Ya There! Jimmy Reed

Proverbs 13:20 Walk with the wise and become wise, for a companion of fools suffers harm

Also check out our Facebook page for the club. Click Link Below to see it!

You can watch some videos from past meetings. Also see some pictures of all the things we do at the club!

Annual Membership now gives you 1 year admission to the club along with 1 year access via our Private Facebook Group. So if you ever cant make a meeting you can watch it online Live, or the next day!

Just Click Either Button for Single or Double Membership! CHECK OUT THE NEW 2022 SPECIAL PRICES!

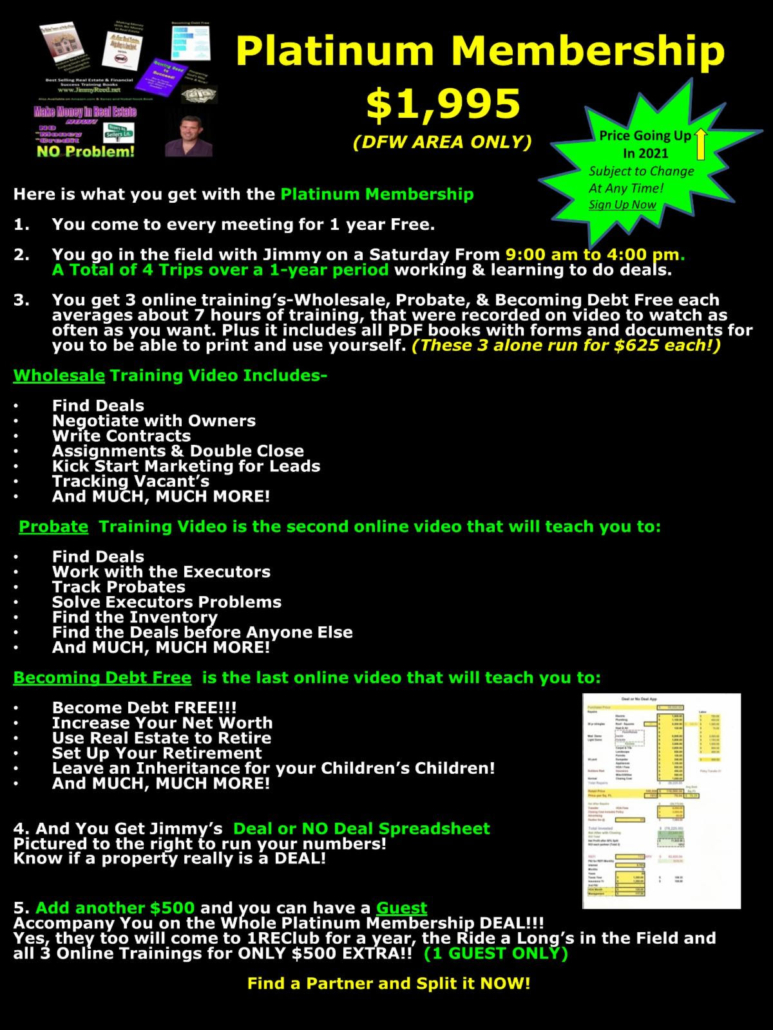

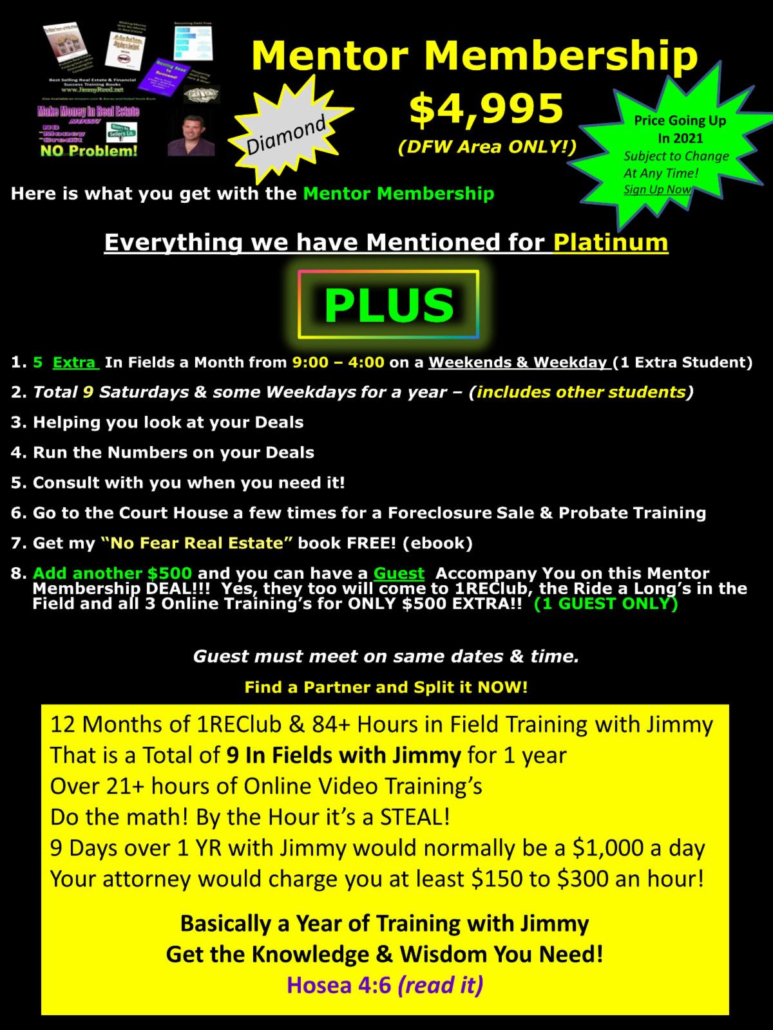

Other Memberships that Include Infield Training’s with Jimmy! Click on the Brochure for More Info.

Platinum Membership

Mentor “Diamond” Membership

For “Platinum” & Mentor “Diamond” Memberships Click Below to Start Training Now!

Check out these Videos on the Real Estate Club & Training’s we have available to help you get started Today!

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/09/Linda-featured.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-09-07 08:23:052023-09-07 09:08:35Founder of Realty 411 & REI Wealth Linda Pliagas & The Texas EXPO!

Whether you are an experienced Real Estate Investor (REIer) or are a newbie in this industry, there exist many innovative funding techniques you can use to finance current and future deals. Generally referred to as creative financing, these terms refer to alternative or unconventional approaches that REIers may choose to utilize to acquire investment properties, using OPM: Other People’s Money.

In today’s unpredictable real estate investor landscape, it is very important to have a range of funding options at the ready before you dive into a property investment deal. Let’s face it, to be a successful REIer takes money. It does not necessarily have to be YOUR money, but before you can successfully pull off a deal, chances are SOMEONE’s funds are going to have to be brought to the table. Plan ahead. Line up funds before you need them because they have to come from somewhere.

article continues after advertisement

Make sure, before you commit to any real estate deal, that you have all your web-footed waterfowl neatly arranged in a linear fashion.

A. Lease Option: You may encounter a situation where you are not ready yet (either experience- or financial-wise) to purchase a property, either for your own personal use or as an investor. That is where the lease option can work best. Doing so provides the opportunity to purchase a property at the conclusion of a pre-arranged leasing-type agreement. This approach allows you to potentially build up equity through monthly rent payments.

The landlord benefits by earning monthly revenue. Typically, and depending on specific contract terms, a portion of the monthly rent payment is credited toward the future down payment on the house. This technique normally works best in a buyer’s market.

B. Down Payment Assistance (DPA). Many REIers are finding themselves caught in a new type of financial squeeze when it comes to the percentage of the purchase price that hard money and private lenders require that they bring to closing, i.e. “Skin-In-The-Game” (SITG) cash.

Until recently, it was possible to secure, say a 90% loan from such lenders, with the borrower required to contribute the other 10% as their SITG capital. And while those terms are still available in some cases, many REIers are waking up to a new reality: They need to bring closer to 20%-30% SITG cash to closing in terms of actual down payment money, with a general average of around 25% DP money currently required.

Upping the SITG percentage is a risk-reduction strategy employed by lenders in response to what they perceive as new uncertainties in the real estate investment marketplace, on a go-forward basis. The reality for REIers caught in this new “liquidity squeeze” is that they now may need to potentially come up with tens of thousands or even hundreds of thousands in new (SITG) investment capital above what was previously required.

Without new SITG capital, the REIer cannot close on the deal. A potential solution to this new dilemma is what we refer to as “Down Payment Assistance (equity) funding”: This is where a third party provides the needed extra SITG/DP cash in return for a modest share of the profits. See below for info about DPA.

C. Seller carryback loan. Plainly speaking, this is simply owner-provided financing. The seller acts as the lender or bank, i.e. he carries a mortgage–usually a second position loan–on the property and collects monthly payments from the buyer. Such an arrangement can be a win-win for both the buyer and the seller. Often the buyer (an REIer in this case) may be willing to pay more than the asking price in trade for advantageous loan terms on a seller carryback mortgage.

Further, the buyer is often willing to pay a higher interest rate on the seller carryback loan than the seller could earn from a CD from their local bank. Also, should the buyer default, the (previous) seller can always initiate foreclosure action and take the house back from the second position. The buyer benefits since they don’t have to go through the arduous and time-consuming chore of trying to get a bank loan; this is especially true if the buyer has a low FICO score or other credit or background issues.

article continues after advertisement

D. Buying a property “Subject-To”. What this means is that the REIer essentially takes over the seller’s remaining mortgage balance (thereby effectively “assuming the loan”) without making it official with the lender. This is a popular strategy among REIers, especially in an era of rising interest rates, since the loan being assumed probably carries a lower interest rate compared to a new (bank) loan.

Savvy REIers often employ the Subject-To method to take the place of a hard money loan. However, most REIers limit the use of Subject-To loans to relatively short-term time frames, i.e. for a few months until the REIer can either refi the loan or sell the property as part of a fix-flip strategy.

E. Hard Money: A hard money loan refers to asset-based financing where the borrower receives funds that are secured by real property. In most cases, private investors are the biggest suppliers of hard money capital, which are then funneled through hard money brokers.

While the terms (interest rate, points, time frames) of hard money loans may vary, there are several common characteristics: they are usually easier to obtain vs. a conventional bank loan; credit scores and income verification are not as important as the asset value involved; they are usually for shorter time frames (say for 6-24 months); while they charge higher interest rates, the good news is that they often can fund pretty quickly if the deal is right. They usually focus on the ARV (After Repair Value) to determine the loan terms, including important factors such as the rehab blueprints, scope of work, etc. They usually prefer to work with experienced rehabbers who have a clear plan to repay the loan within the specified time frame.

F. Cross collateral loan. This REI method assumes you already own a rental property free and clear. You want to buy another rental property. A cross collateral loan allows you to use the 100% equity in the existing property as leverage to acquire the new property you want to purchase. With cross-collateralization, the lender places a lien on both the new property and your existing property. In this way, the lender receives adequate security should you default on the loan. Basically, cross-collateralization allows you to sidestep the normal down payment requirement and/or having to take out a brand new (bank) loan.

G. Retirement accounts: Use your self-directed IRA, Roth IRA, 401-K, corporate plans as investment capital, where it is legal, prudent and appropriate to do so. Utilizing a self-directed retirement plan can empower a REIer by boosting their retirement savings, one deal at a time. Since we are talking about your retirement money, an extra degree of caution is called for. You need to possess excellent due diligence and underwriting skills in order to properly assess the potential risks involved.

H. Cash-Out Refinance. If your personal residence has a good amount of equity in it, you can unlock that equity via a cash-out refinance by tapping some of that equity. Make sure you fully understand the implications of such a loan should things not go well with your anticipated new investment. A cash-out refi may feature (more) favorable interest rates compared to a hard money loan. Also, the interest you pay is tax deductible. You need to do a risk/benefit analysis before going down this road. Regardless, if a REI deal looks very promising, and you require fast capital to make it happen, a cash-out finance can be a good way to go.

I. 203-K Loan: This unique FHA mortgage enables you to finance both the purchase (or refinancing) of a house and the cost of its rehabilitation through a single mortgage or to finance the rehabilitation of their existing home.

1. Pros:

a. Lower credit score allowed b. Smaller down payment requirements (as low as 3.5%) c. Can provide temporary housing while a home is being repaired d. Lower potential interest rates, compared to similar loan types e. Ability to combine home purchase and renovations into a single loan

f. Low down payment and credit score requirements

2. Cons:

a. FHA mortgage insurance required b. FHA loan rates may be higher compared to conventional loans c. Process may require meeting with a 203(k) repair consultant d. More extensive repairs require more paperwork e. Potential for the additional cost of architectural assessments f. Property must be your primary residence g. You must live in the home for 12 months before selling or renting it out

J. More creative financing methods to consider include:

1. Approach friends, relatives, etc. Options can include debt or equity.

2. Equity investors. The advantage here is that you do not have to make monthly payments because there is no loan. When the deal is done, some sort of profit split is made to compensate the investor(s).

3. Credit card advances. This can be an expensive gambit. It is only to be undertaken when you are very sure of positive, short-term outcomes. The bank may charge several points and up to 29% interest rates, so be very careful with this one.

4. Joint venture: you bring the deal, they bring the money, split the profits at the end. This is a variation on an equity-type investment.

5. Hypothecate (borrow against) a mortgage note you own. Basically, you take out a loan by pledging the note, thereby using it as collateral to secure the loan.

6. Personal asset loans: pawn some jewelry; get a car title loan, etc.

Down Payment Assistance Funding Program

Are you a Real Estate Investor Pro (REI Pro) who has a property you want to buy, with a 70% LTV or better, but you lack some of the Down Payment (DP) money needed to close the deal? You need say, 25% DP, but can only come up with 10% and need 15% more (DP money.

The good news is if your deal meets our standard criteria (70% LTV or better = 30% or more equity in the deal, etc.), CTF can provide the missing 15% in DP funding. By not having to put out all your own capital into DPs–especially if you are low on cash–you’ll be able to do more deals. With your DP source already in place, it will shorten your time for getting positive confirmation from your primary lender, and for getting more deals successfully closed.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

Are you tired of playing it safe with your investments? Want to spice things up and take on a potentially lucrative option? Real estate syndication may be just what you’re looking for, and as a limited partner (LP), you can reap some benefits.

In this article, we’re going to explore the world of real estate syndication and why being an LP can be a fun and rewarding way to invest in real estate. From higher returns to less hassle, being an LP has some unique advantages worth considering. So put on your investor hat, and let’s dive in!

article continues after advertisement

1. Limited Liability

A key benefit is the limited liability protection from investing as an LP in a real estate syndication. It protects the investor from personal liability if the investment fails or incurs liabilities. So, for example, if a tenant slips and falls on a property owned by the syndication, the LP investor’s personal assets will not be at risk. Instead, the GP will be responsible for any losses or liabilities incurred by the partnership.

A National Bureau of Economic Research study states limited liability protection is critical in encouraging entrepreneurship and investments. The study found that limited liability is associated with a higher likelihood of investments and a more significant number of firms being created.

2. Passive Investments

Investing as an LP in a real estate syndication is a passive activity, meaning that the investor does not have to be actively involved in the day-to-day management of the real estate assets. Instead, the GP is responsible for managing the assets, and the LP investor receives a share of the proceeds based on the percentage of their investments.

According to a National Multifamily Housing Council report, passive investing in real estate is becoming increasingly popular, with many investors seeking to diversify their portfolios beyond traditional assets such as stocks and bonds. In addition, the report found that passive investing in real estate syndications can provide a steady stream of wealth and long-term capital appreciation.

3. Connect to Larger and Diversified Investments

Investing in a real estate syndication as an LP provides investors a connection to more extensive and diversified real estate projects that they may have yet to be able to approach on their own. The GP is responsible for identifying, acquiring, and managing the real estate assets, while the LP investor provides the funds.

According to a report by the Urban Land Institute, investing in real estate syndications provides a door to a wide range of real estate assets, including commercial properties, multifamily buildings, industrial properties, and more. In addition, the report found that investing in real estate syndications can provide diversification benefits to investors by allowing them to invest in various assets with different risk and return profiles.

article continues after advertisement

4. Potential for Higher Returns

Investing as an LP in a real estate syndication can provide higher returns than traditional investment vehicles, such as stocks, bonds, and mutual funds. The potential for higher returns is due to the GP’s ability to manage the real estate assets and maximize the return on investments.

According to a National Council of Real Estate Investments Fiduciaries report, real estate investments have historically provided higher returns than other traditional investment vehicles. For example, the report found that from 1999 to 2019, the total annualized return for real estate investments was 9.5 %, compared to 6.2 % for stocks and 5.3 % for bonds.

5. Tax Benefits

Investing as an LP in a real estate syndication can provide various tax benefits, including depreciation deductions, passive activity loss deductions, and capital gains tax deferral. These tax benefits can reduce the investor’s tax liability and increase their after-tax return on investments.

According to a report by PwC, real estate investments can provide various tax benefits to investors. For example, depreciation deductions can offset taxable wealth, and passive activity losses can be deducted against other passive wealth sources. Additionally, a 1031 exchange can defer capital gains taxes by reinvesting the proceeds from selling real estate assets in other qualifying real estate investments.

Investing as an LP in a real estate syndication can also provide specific advantages for busy professionals who may not have the time or expertise to manage real estate investments actively. Some additional advantages include the following:

6. Time Savings

Investing in real estate syndications as an LP can be a time-efficient investments strategy for busy professionals. The GP is responsible for identifying, acquiring, and managing the real estate assets, while the LP investor provides the funds. This allows LP investors to focus on their careers and other activities while still earning a return on their investments.

7. Expert Management

Real estate syndication allows LP investors to benefit from the expertise of the GP in managing real estate assets. The GP typically has experience and knowledge in real estate investments and can use this expertise to maximize the return on investments for the LP investors. This can be especially beneficial for busy professionals who may not have the time or expertise to manage real estate investments actively.

8. Limited Involvement

Investing in real estate syndications as an LP can provide limited involvement for busy professionals. The LP investor does not have to be actively involved in the day-to-day management of the real estate assets, allowing them to focus on their career and other activities. The GP is responsible for managing the assets, and the LP investor receives a share of the returns based on the percentage of their investments.

9. Diversification

Investing in real estate syndications as an LP can provide diversification benefits for busy professionals. The GP is responsible for identifying, acquiring, and managing various real estate assets, allowing the LP investor to invest in a diversified portfolio of assets. This can reduce investment risk and provide a more stable return on investments.

10. An Entry to Exclusive Deals

Real estate syndication can provide LP investors with a way to exclusive real estate deals that may not be available to the general public. In addition, the GP typically has a network of contacts in the real estate industry and can use this network to identify and acquire exclusive real estate assets. This can provide LP investors with unique creation wealth opportunities and higher returns.

Overall, investing as an LP in a real estate syndication can be a time-efficient, low-involvement, and diversification investments strategy for busy professionals. In addition, the expertise of the GP in managing real estate assets can help maximize the return on investments for the LP investors. At the same time, limited liability protection can provide additional security for their assets.

At Blueocean Capital, we offer a unique opportunity for investors to become limited partners (LPs) in our real estate syndication projects. As an LP, you get to enjoy the benefits of investing in larger real estate projects without having to worry about the details of managing the property. You can trust that our experienced team of professionals will handle all the work while you sit back and collect passive income from your investment. Plus, by investing with us, you can benefit from potentially higher returns compared to traditional real estate investments.

So why not consider becoming an LP with Blueocean Capital? It’s a great way to diversify your portfolio, earn passive income, and potentially achieve long-term financial goals. Join us today and let us show you how being an LP can be a rewarding investment opportunity!

You can also schedule a with us to learn more about our investment opportunities and how you can become a Limited Partner. Our team will be happy to answer any questions you have and guide you through the process.

Let’s start building your investment portfolio together!

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/09/Bigger-Better-Hassle-Free.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-09-05 05:23:092023-09-05 05:23:13Why Limited Partners Love Real Estate Syndication

We are very excited to announce our 4th Annual Los Angeles Real Estate Grand Expo. The Grand Expo returns on Saturday, October 21, 2023, 9:00 am to 6:00 pm. We’re taking over the entire Iman Cultural Center for the day – it’s all ours!

The North Hall (vendor exhibition area), the South Hall (workshops), and the middle parking lot (loaded with workshop tents and food trucks). The theme of this year’s Grand Expo will be “Hedge Inflation – Buy Real Estate”.

Last year, the Grand Expo was the largest real estate event in Southern California. We had over 800 investors, 64 vendors, and 12 national speakers…this year will be even BIGGER! An entire day celebrating real estate investing and you can be involved. Best of all, the Grand Expo will be FREE to attend.

This Expo is going to be big, really BIG! We are hosting investors from around the nation once again.

EDUCATORS. There will be national guest speakers (in three breakout rooms). Here is a partial list of our top educators:

1. Jonah Dew – “The Money Multiplier” 2. Eddie Speed – “Buying Discounted notes” 3. Rusty Tweed – “1031 Tax-Deferred Exchanges” 4. Joe Arias – “How to Get Started Investing” 5. Christopher Meza – “Developing Raw Land” 6. Tony Watson – “Tax Advantages for R.E. Investors” 7. Dani & Flip Robison – “Fixing & Flipping Houses” 8. Abbas Mohammed – “Investing in Multi-Residential Properties” 9. Marco Kozlowski – “How to Buy Lots and Lots of Houses” 10. Amanda Brown – “Invest in Commercial Real Estate” 11. Shawn Tiberio – “Marketing for Real Estate Investors” 12. Joeseph Scorese – “How to Finance Your Next Deal” 13. Jeremy Rubin – “From Employee to $100M in Flips” 14. Steve Price (Keynote) – Vice President at Auction.com

INVESTMENT EDUCATION. An all-day in-depth educational extravaganza celebrating real estate investing. Most importantly, this will NOT be a sales pitch. So regardless of whether you are a new investor, already own properties, or are very experienced, our Grand Expo is for you!

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/09/Grand-Expo-speakers.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-09-04 03:53:172024-04-17 02:50:46Join Us for Education, Motivation and Collaborate – RSVP Now!

NEW YORK, NY — B+E, the first brokerage and technology platform for net lease real estate, today announced the addition of Max Sabino as an Associate Director in the New York B+E office.

Max Sabino

“We are excited to welcome Max to the B+E team,” said B+E CEO Camille Renshaw. “He is a results-driven sales professional with a proven track record in net lease sales and is skilled in conducting market research, analyzing client requirements, and tailoring solutions to meet their needs.”

article continues after advertisement

Max focuses on the execution of sale-leaseback programs and asset disposition/acquisition programs for private family offices, franchisors, franchisees, developers, and other large institutions.

Most recently with SRS Real Estate Partners, Max was a part of the division’s most successful net lease team, based in Newport Beach, CA. During his time there, he gained deep net lease knowledge, including understanding inherent real estate value, market conditions, tenant/credit underwriting, site-level performance metrics, and lease economics. Max Sabino

article continues after advertisement

Prior to SRS Real Estate Partners, he was a broker at Aspect Real Estate Partners. While there, he was the top individual contributor and made partner with the three Max Sabinofounding principals.

About B+E

B+E is a modern investment brokerage firm, specializing in net lease real estate. The firm helps clients buy and sell single tenant real estate. Founded by deeply experienced brokers, B+E redefines trading through an intuitive end-to-end transaction platform consisting of user-friendly dashboards and an AI-driven exchange — all leveraging the largest data set in the net lease industry. With offices in New York, Chicago, Atlanta, Tampa, Charlotte, Dallas, Orange County, and San Francisco, its brokers trade property for clients across the US.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/shake-hands.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-31 02:53:592023-08-31 02:54:03Max Sabino Joins B+E’s New York Office as Associate Director