This is an incredible opportunity for skilled professionals who want to work with a company that guarantees abundant direct organic daily leads, hands-on management training and support, niche mortgage loan programs with competitive pricing, and advanced mortgage technology.

Mortgage Loan Officers can expect to close their first loan within four to six weeks after the completion of their initial training.

Mortgage Loan Officers who join the Stratton Equities team can expect the following:

Competitive compensation: Stratton Equities offers a highly competitive compensation plan, potentially allowing Mortgage Loan Officers to earn their first year $110,086.26 – $190,677.36.

Strong resources: Stratton Equities’ interest rates are some of the lowest nationwide in private lending, starting at 6.75%, and can pre-approve a loan in 24 hours.

Room for growth: As a rapidly growing company, Stratton Equities offers ample opportunities for advancement and career growth. With a focus on promoting from within, Mortgage Loan Officers who join the team will have the chance to take on new challenges and responsibilities as they progress in their careers.

A dynamic work environment: At Stratton Equities, Mortgage Loan Officers will work in a fast-paced, dynamic environment focused on innovation and results. As a part of the loan officer team, you can work directly with prospective real estate investors, entrepreneurs, and borrowers on their real estate endeavors.

If you are an experienced Mortgage Loan Officer looking for an exciting new opportunity to grow your career or a licensed Mortgage Loan Originator that is new to the industry and needs help finding business, then Stratton Equities is the place for you to earn a great income.

This is an incredible opportunity to join a leading nationwide mortgage lender and build a bright future with a company that values its employees and their contributions.

Contacts For media inquiries and interviews, please contact Kelly Bennett of Bennett Unlimited PR at [email protected].

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/01/we-are-hiring.jpg5001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-01-15 01:15:142024-01-15 01:15:16Stratton Equities is Hiring Mortgage Loan Officers to Join Their Dynamic New Jersey Team and Build a Lucrative Career in the Mortgage Industry

As the mortgage industry struggles, Advisors Mortgage Group expands

OCEAN TOWNSHIP, N.J., June 13, 2023 — Advisors Mortgage Group, based in Ocean Township, New Jersey, today announces an influx of new loan officers joining the Company. While the mortgage industry has seen many companies closing and banks, such as Wells Fargo, dissolving their mortgage lending divisions, Advisors Mortgage Group is still growing.

“One of the many things setting Advisors Mortgage apart from our competition is the support we offer loan officers. We have a marketing department that curates custom campaigns weekly for prospecting and we have implemented milestone marketing to our borrowers. CRM assistance, custom websites, social media set-up and posting are also tools provided consistently. We train our loan officers to be consultants and trusted advisors and provide them with weekly live streaming shows on the current state of the markets,” says Jonathon Iacono, national recruiting manager.

Dave Wicki, Ocean, New Jersey, branch manager, returned to Advisors after a year’s absence and had this to say: “I came back home to Advisors because of its family-oriented culture. The support they provide to all their loan officers is unrivaled. They listen to my needs and go out of their way to set me up for success.”

ADVERTISEMENT

Steve Yap recently joined the company, claiming, “Advisors is the best in the business, and I know I will be successful with all of the support they provide to their loan officers.”

Newly hired loan officer Colleen Reed notes: “I came on board to Advisors after meeting with my branch manager and talking with many title companies and agents about their past experiences with this company. I heard nothing but great things, looked into all the marketing platforms, talked to other loan officers at Advisors and made a great decision to join the company. The transition with the entire staff from onboarding to training has been amazing.”

Jordy Castillo, market manager, from the Wantagh, New York, branch states: “Before I decided to join Advisors Mortgage Group I was being recruited by Citibank and East West Bank. I also had an offer from CrossCountry Mortgage. I decided to join Advisors simply because I knew that it was the right fit. I’d referred Carlos Quezada to a few deals that I couldn’t do, and he was able to get them closed quickly and efficiently so I felt comfortable making the move.”

ADVERTISEMENT

Castillo continued: “In the current mortgage market, I truly believe that it is more important than ever before to have the right partner. I declined senior management roles at both Citibank and East West Bank because I knew I would be limiting myself and my loan officers. Big banks come in and out of the mortgage market, with that said I wanted to make sure that I joined a company where mortgage originations are their only priority. In addition to this, at Advisors, we have access to every single product you could ever need. Our transparent process, family atmosphere and loan officer-first mentality firmly sets us apart from the competition. With the support of senior leadership, Carlos and I will build a top-producing sales team here at Advisors Mortgage Group. The future looks bright at Advisors Mortgage Group, and I feel fortunate to be able to be a part of it.”

According to metrics provided by Marketrac®, a premier online portal providing intelligent, on-demand data and analysis on real estate transactions, Advisors is the top purchase lender on the Jersey Shore. The Company has also made the Inc. 5000 Fastest Growing Private Companies list numerous times since 2009, was named Best Mortgage Lender five years in a row by the Asbury Park Press in their Community Choice Best of the Best awards and also made the NJBIZ Best Places to Work list for the past decade.

To learn more about Advisors Mortgage Group, please visit their website at: https://advisorsmortgage.com/ or call them at 855-LOANS-USA.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/06/HIRING.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-06-14 02:50:572023-06-14 02:51:02Advisors Mortgage Group On a Hiring Spree

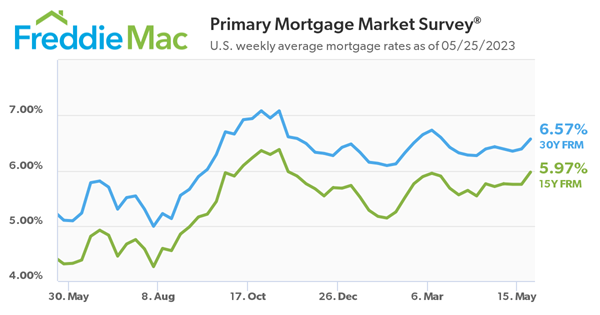

MCLEAN, Va., May 25, 2023 — Freddie Mac (OTCQB: FMCC) today released the results of its Primary Mortgage Market Survey (PMMS), showing the 30-year fixed-rate mortgage (FRM) averaged 6.57 percent.

“The U.S. economy is showing continued resilience which, combined with debt ceiling concerns, led to higher mortgage rates this week,” said Sam Khater, Freddie Mac’s Chief Economist. “Dampened affordability remains an issue for interested homebuyers and homeowners seem unwilling to lose their low rate and put their home on the market. If this predicament continues to limit supply, it could open up an opportunity for builders to help address the country’s housing shortage.”

ADVERTISEMENT

News Facts

30-year fixed-rate mortgage averaged 6.57 percent as of May 25, 2023, up from last week when it averaged 6.39 percent. A year ago at this time, the 30-year FRM averaged 5.10 percent.

15-year fixed-rate mortgage averaged 5.97 percent, up from last week when it averaged 5.75 percent. A year ago at this time, the 15-year FRM averaged 4.31 percent.

The PMMS is focused on conventional, conforming, fully amortizing home purchase loans for borrowers who put 20 percent down and have excellent credit.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/05/mortgage-increase.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-05-26 05:28:382023-05-26 05:28:42Mortgage Rates Continue to Increase

This is an incredible opportunity for skilled professionals who want to work with a company that guarantees abundant direct organic daily leads, hands-on management training and support, niche mortgage loan programs with competitive pricing, and advanced mortgage technology.

Mortgage Loan Officers can expect to close their first loan within four to six weeks after the completion of their initial training.

ADVERTISEMENT

Mortgage Loan Officers who join the Stratton Equities team can expect the following:

Competitive compensation: Stratton Equities offers a highly competitive compensation plan, potentially allowing Mortgage Loan Officers to earn their first year $110,086.26 – $190,677.36.

Strong resources: Stratton Equities’ interest rates are some of the lowest nationwide in private lending, starting at 6.75%, and can pre-approve a loan in 24 hours.

Room for growth: As a rapidly growing company, Stratton Equities offers ample opportunities for advancement and career growth. With a focus on promoting from within, Mortgage Loan Officers who join the team will have the chance to take on new challenges and responsibilities as they progress in their careers.

A dynamic work environment: At Stratton Equities, Mortgage Loan Officers will work in a fast-paced, dynamic environment focused on innovation and results. As a part of the loan officer team, you can work directly with prospective real estate investors, entrepreneurs, and borrowers on their real estate endeavors.

If you are an experienced Mortgage Loan Officer looking for an exciting new opportunity to grow your career or a licensed Mortgage Loan Originator that is new to the industry and needs help finding business, then Stratton Equities is the place for you to earn a great income.

This is an incredible opportunity to join a leading nationwide mortgage lender and build a bright future with a company that values its employees and their contributions.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/05/HIRING.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-05-09 04:39:592023-05-09 04:52:08Stratton Equities is Hiring Mortgage Loan Officers to Join Their Dynamic New Jersey Team and Build a Lucrative Career in the Mortgage Industry

Why are you just searching for listed properties for sale when the number of distressed, vacant, and “shadow inventory” homes is almost 33 times larger than the national home listing inventory supply?

How is this possible with my 33 number claim? First, upwards of 16 million homes were listed as “vacant” or shadow inventory in the fourth quarter of 2022, as per the U.S. Census Bureau, National Association of Realtors (NAR), and other groups. A vacant home can be defined as a vacation home, unsold new home building inventory (near record levels of new single-family homes and multifamily apartment buildings being built in 2023), distressed or pre-foreclosure properties, or homes held by billion-dollar corporations like BlackRock, Blackstone, or State Street for the long-term that just sit there with no intent to rent it out at present.

Second, there are at least a few million distressed mortgages (FHA loans, especially) currently in forbearance agreements in order to delay the lender’s foreclosure filing actions to bring the total to more than 18.5 million properties. Frankly, I think that the number is closer to 20 million after counting VA, conforming, non-QM, and private money loans, but we’ll just focus on the 18.5 million vacant or distressed home number.

Since 1934, FHA (Federal Housing Administration) has insured more than 40 million loans nationwide. Today, a relatively high percentage of homebuyers still rely upon FHA to purchase their homes partly due to the much lower interest rates and easier loan qualification guidelines such as loan programs which allow FICO credit scores as low as 500, debt-to-income (DTI) ratios up to 50% or higher, and loan-to-value (LTV) options near 96.5% to 100% LTV.

As of March 2023, the national home listing inventory was listed at 562,565 by data provided by the Federal Reserve Economic Data and the NAR. Let’s do the math as follows:

18.5 million distressed or vacant homes / 562,565 listed homes = 32.885 times

ADVERTISEMENT

Distressed FHA Loans & Continued Forbearance Extensions

There are three to four times as many delinquent FHA mortgage loans nationwide as compared to the entire national home listing inventory with somewhere near at least a few million distressed FHA loans.

February 8, 2023: Today, the U.S. Department of Housing and Urban Development (HUD) Secretary Marcia L. Fudge announced that, thanks to Federal Housing Administration (FHA) programs, approximately 2 million homeowners with FHA mortgages were able to stay in their homes from the beginning of the COVID-19 pandemic in March 2020 through December 2022 – when doing so was often a matter of life and death. During this period of time amid the pandemic, FHA borrowers whose ability to make their mortgage payments was impaired by the pandemic were able to obtain either a COVID-19 forbearance or a more permanent solution such as a loan modification that allowed them to avoid foreclosure. Source: HUD Secretary Announces Major Milestone of Assisting Nearly 2 Million Homeowners Stay in their Homes

With a few million distressed FHA loans that they admit to and is probably undercounted, it’s no wonder why the federal government wants to keep offering FHA forbearance extensions.

Details of FHA’s COVID-19 Forbearance

Important information about FHA’s COVID-19 Forbearance:

To be eligible for the COVID-19 Forbearance or forbearance extension in the table above, you must request this relief from your servicer on or before May 31, 2023.

You can request a FHA COVID-19 Forbearance for up to 6 months. If needed, an additional 6 month extension may be requested. If you began your initial forbearance on or after October 1, 2021, you are only eligible for the additional 6 months if your initial 6 months forbearance will be exhausted and expires on or before May 31, 2023.

Additional forbearance options may be available to you after May 31, 2023. Your mortgage servicer may provide for a temporary pause or reduce your monthly mortgage payments to allow you time to overcome your financial hardship. An extended forbearance period may be provided to you if you are unemployed and actively seeking employment.

No extra fees, penalties, or interest will be added to your account during the forbearance period.

There are also a significant number of distressed VA and conforming or conventional loans nationwide which are held by Fannie Mae or Freddie Mac in the secondary market that aren’t really being “officially” counted with the most up to date numbers. FHA and VA mortgage loans have both consistently represented close to 10% each of the annual national funded loan market. As a result, these government-backed or insured loans, which typically average close to 0% to 3.5% down payments for FHA, VA, and conforming, are something to keep a close eye on as the economy continues to soften.

The 40-Year Loan Modification Program for FHA Borrowers

Good news: National mortgage delinquency rates dropped 15% in March 2023 while reaching 2.92%, which was a new all-time record low.

Bad news: Millions of distressed mortgages are not being counted as “delinquent” once they enter forbearance agreements with their lender (FHA loans, especially). The national FHA loan default rate reached 12% in February and will likely continue to rapidly increase. Distressed FHA and VA loan investments are some of the best deals out there because they usually have the lowest mortgage rates that you can take over by way of creative seller-financing techniques.

A forbearance agreement is when the lender or mortgage loan servicing company agrees to postpone or delay their foreclosure actions with the delinquent borrower. Sometimes, these foreclosure postponements may last months or years.

On March 8, 2023, HUD issued their Mortgagee Letter 2023-06 with details described as the “Establishment of the 40-Year Loan Modification Loss Mitigation Option” with a stated purpose noted as “This Mortgagee Letter (ML) establishes the 40-year standalone Loan Modification into FHA COVID-19 Loss Mitigation policies.”

Several mainstream media analysts mistakenly described this new 40-year loan proposal offered by FHA as a purchase loan as well. Yet, this is not correct because it’s only for the refinance of currently distressed 30-year FHA loans into longer 40-year loan terms in order to reduce the monthly payments for borrowers. There is no published word about whether FHA will later consider offering 40-year purchase loans for borrower prospects.

Housing and Family Trends

Real estate is a people business, first and foremost. The #1 most important factor for housing trends is related to population trends and household formations for families especially. Without people, there’s no need for housing regardless of the affordable financing offered.

One of the main reasons why people purchase single-family homes is because they’re trying to either build a growing family or the need to house two or three generations of the family under the same roof. You can’t spell “single-family homes” without family in it.

The U.S. has the highest percentage of one-person households in the entire world. A few years ago, one-person households surpassed all other household formations in Canada.

In 2022, only 24% of U.S. households had at least one child under the age of 18. In 1965, upwards of 42% of households had a child under the age of 18.

The Decline of Family Households

Here are some of the published data numbers from sources such as the U.S. Census Bureau, the National Center for Health Statistics (NCHS), Pew Research, and numerous other data sources in regard to individuals and family structure trends:

National overall divorce rate in the USA: 50%+.

The California divorce rate is 60%.

The Orange County, California divorce rate is 72%.

41% of first marriages nationwide end in divorce.

60% of second marriages end in divorce.

73% of third marriages end in divorce.

The average length of a marriage in the U.S. that ends in divorce is 8 years.

There is one divorce every 36 seconds in the U.S. on average; 2,400 divorces per day; 16,800 divorces per week; and 800,000 to 900,000 divorces per year.

The percentage of American men between the ages of 20 and 39 who are now married has fallen by half (35% of men are married as of 2017) since the early 1970s (70% of men were married).

Unmarried parents who live together are more likely to break up than married parents, per the Brookings Institute.

Per the CDC in 2016 through at least 2020, U.S. fertility rates were the lowest ever recorded as fewer couples are having children these days. Each consecutive year over the past five or six years reached all-time record lows.

78% of all households in the U.S. contained one married couple in 1950. Today, married households are below 48%.

In 2010, the Pew Research Center reported that 44% of Americans polled in the 18-to-29 year old age range believed that “marriage was becoming obsolete.”

Divorce rates for people over the age of 50 have doubled between 1990 and 2015, per Pew Research Center.

In 1956, roughly 5% of all babies were born to unwed mothers. Between 2008 and 2016, babies born to unwed mothers were closer to the 40% range.

Upwards of 50% of children in impoverished regions of the U.S. live in homes without fathers.

46% of children live at home with a mother and father who were in their first marriage together.

The average American woman in 1970 had her first child at 21.4 years of age. Today, the woman is near 25.6 years of age.

The U.S. has the highest teen pregnancy rate in the industrialized world.

More than 50% of children are born to unmarried women under the age of 30.

Saving Equity or Creating Newfound Wealth

What are your options as either a homeowner with an ongoing forbearance agreement in place with your lender, a struggling business owner, a commercial property owner and landlord with incredibly high vacancy rates, or as an investor seeking new opportunities if and when the economy suddenly pivots and we enter a more clearly visible deeper recession? If home values are more likely to be higher today than later this year, is it now a good time to sell? If so, where will be your next destination for a home?

Generally, loss of income is the #1 reason why homeowners lose their homes to lenders or mortgage loan service companies in foreclosure. The #2 reason why homeowners walk away from their home is when the mortgage debt exceeds the current market value and it’s upside-down or underwater. This is when short sale options become more prevalent.

ADVERTISEMENT

The real risk associated with homes purchased in recent years is related to the relatively low down payment averages for first-time buyers and others that were leveraged between 96.5% and 100% loan-to-value at the close of escrow. Effectively, these homebuyers were upside-down with negative equity at closing when factoring in the potential 6% to 8% closing costs to resell the homes after paying real estate brokerage commissions, title, escrow or attorney’s fees, transfer taxes, third-party inspection reports, and possible seller credits towards the buyer’s closing costs.

In 2022, first-time homebuyers represented 34% of all home purchases across the nation, as per the NAR. During the fourth quarter of 2022, purchase loans comprised 78.6% of all FHA mortgages funded. With a high percentage of FHA borrowers reported as first-time homebuyers, their average down payments were likely close to 3.5% or below. What happens if home values fall 5%, 10%, or more in value over the next year?

If you’re currently in a distressed mortgage situation as a homeowner or investor or are searching for discounted off-market listings as a buyer with very creative and flexible financing solutions, I can show you effective ways to save your equity or create newfound wealth with my mortgage and investment business named Realloans (Real Estate Loans and Creative Sales) and my real estate group linked here: So-Cal Real Estate Investors.

Rick Tobin

Rick Tobin has worked in the real estate, financial, investment, and writing fields for the past 30+ years. He’s held eight (8) different real estate, securities, and mortgage brokerage licenses to date and is a graduate of the University of Southern California. He provides creative residential and commercial mortgage solutions for clients across the nation. He’s also written college textbooks and real estate licensing courses in most states for the two largest real estate publishers in the nation; the oldest real estate school in California; and the first online real estate school in California. Please visit his website at Realloans.com for financing options and his new investment group at So-Cal Real Estate Investors for more details.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/05/house-ratio.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-05-02 06:29:572023-05-03 02:49:39A 33-to-1 Vacant & Distressed Home-to-Listed Home Ratio

Mortgage rates are rising again, causing the average homeowner to pay $800 a month more than they would have just a year ago, according to REALTOR.com.

The interest rate for a 30-year fixed mortgage is 6.54%, while the rate for a 15-year fixed mortgage is 5.75%, per Mortgage News Daily. Even Veterans Administration (VA) loans aren’t getting much relief, with the 30-year fixed rate coming in at 5.95%.

ADVERTISEMENT

While these numbers aren’t as high as they were in November 2022, they still present significant financial hurdles to would-be homebuyers, REALTOR.com reported.

Because prices are high, people need to borrow more money than before. Hence, people who could ordinarily buy a home are choosing to rent instead; this is good news for real estate investors.

ADVERTISEMENT

The last time mortgage rates were this high was 2008. With housing prices 42% higher than they were before the COVID-19 pandemic, this is a serious situation for many aspiring homeowners.

Investors and traditional buyers alike are encouraged to shop around for concessions, special programs, and to explore multiple lenders. However, some investors believe that the state of the economy will once again cause mortgage rates to increase.

Stephanie Mojica

Stephanie Mojica, writer of How One Writer Shifted From Settling for $12 an Hour to Prospering at Over $90 an Hour and shorter books such as Quick Answers to Frequently Asked Credit Questions, is an award-winning journalist with publications such as USA Today, The Philadelphia Inquirer, San Francisco Chronicle, and The Virginian-Pilot, among many others. She helps executive coaches, business consultants, business owners, attorneys, and other decision makers generate more money online and become the go-to expert in their field by guiding them step by step through the process of writing and publishing a book.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/05/MORTGAGE.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-05-01 05:53:112023-05-01 05:53:16Mortgage Rates are Rising Again

Future and current homeowners have been mesmerized by countless media reports about increasing mortgage rates and decreasing home sales prices. However, the 20-year high in mortgage rates is not the biggest problem facing the real estate market, according to REALTOR.com.

ADVERTISEMENT

Many residential properties are staying on the market significantly longer because the combination of increased mortgage rates and home prices is too much for the average buyer to bear. As a result, a number of potential buyers are waiting for housing prices to drop, per FOX Business.

As of October 27, 2022, the average interest rate for a 30-year fixed mortgage was 7.08%. The average at the same time last year was 3.14%. The current rate for a 15-year fixed mortgage is 6.36%, compared to 2.37% in 2021.

ADVERTISEMENT

Some real estate investors are panicking over these changes in market conditions, Fortune.com noted. This may be justified, as home prices fell 27% between 2006 and 2012 — and experts expect even more significant reductions in the years to come. Prices have plunged 8.2% in San Francisco, for example.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2022/11/MORTGAGE-UP.png4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2022-11-03 04:41:272022-11-03 04:41:30Increasing Mortgage Rates are Only Part of the Problem

One of the best jobs you can go for these days if you want to work hard, make a lot of money, and change the world around you is to become a mortgage loan officer. There are so many opportunities out there in the real estate world to make a living, but one of the most fulfilling and lucrative is to become a mortgage loan officer for a private money lending firm.

But what are the steps you will have to take to even become a loan officer?

Like most careers that deal with highly valuable assets and specified levels of management and service, to become a loan officer, you need to get your license. The NMLS, or Nationwide Mortgage Licensing System, offers a variety of mortgage licenses but the one in particular that applies to loan officers most is the Mortgage Loan Originator (MLO) license.

ADVERTISEMENT

How to get licensed as a Mortgage Loan Officer/Originator

Getting an NMLS license will certify that as a loan officer, you are now able to legally serve as a mortgage loan originator. Additionally, it informs your prospective clients and employers, that you are knowledgeable of all the laws and regulations that come with mortgage lending.

More specifically, obtaining an NMLS license means that you have completed a class that teaches you all the requirements for serving as a mortgage loan officer, and that you have passed the SAFE Mortgage Loan Originator Test.

You must complete both tasks to be properly qualified to apply for the NMLS license. Once you have your NMLS license, you can easily apply for most private lending and conventional mortgage lender positions.

Although the Nationwide Mortgage Licensing System (NMLS) License covers across the country, you will still need to apply for an individual license per state you are looking to lend in.

Applying to Become a Mortgage Loan Officer with a Private Lender

Believe it or not, the next step in becoming a mortgage loan officer is finding a position at a private lending firm that suits your needs and interests. The NMLS license qualifies loan officers for all private lending and conventional lending mortgage companies. This will allow you to apply for all loan officer positions, however, you will still need the individual license per state.

After applying at your desired location, the interview process shouldn’t be too surprising or different from any other high-level interview process as they will mainly ask you questions and test you on your skillset, knowledge, and ambitions.

Once you’ve secured the position, the best private lending firms will provide thorough training, management, and support.

ADVERTISEMENT

Working at a Private Lending Mortgage Company

Through training new loan officers, a private lender prepares their sales team to help guide them to mastering some of the nuances required as a loan officer, that cannot be taught purely through an academic mindset.

You must be ready and focused as a loan officer and this level of training throughout the first few months of the job will help get you to that point.

As important as it is to get certified by the NMLS, there is only so much you can learn by studying laws, memorizing loan options, and practicing unique scenarios. The real test of grit is to see how well you work in a real-world setting.

To be successful as a loan officer you need to be sharp-minded at all hours, diligent in the details, dedicated to working hard, and affirmative in your tone, actions, and decisions. Furthermore, be intuitive enough to understand what is a good deal and how to thread the needle if plans don’t go as expected.

The work will be hard but the rewards are great. On average a mortgage loan officer at a private lending mortgage company can make an average of $150,000-$250,000 a year.

Securing Your Position as a Mortgage Loan Officer

To secure your career as a successful loan officer at a private lending institution, there are a couple more things you can do to ensure your success.

Firstly, there is the option to get certified by the Mortgage Bankers Association (MBA) and/or the American Bankers Association (ABA). This step is optional and not required for the position of loan officer, but getting this certificate can help boost your credentials, entice more clients to come your way, acquire yourself more deals and negotiations from borrowers, and specialize your skill set such that you are even more knowledgeable and prepared as a loan officer.

Lastly, you must renew your NMLS license every year. This is to ensure that whoever is still practicing they are aware of certain changes in the law, whether it be on the nationwide level or statewide. Additionally, renewing your license frequently keeps you fresh and sharp-minded as you are regularly checked on how well and how prepared you are at the job.

These are all the principal steps one takes when seeking to become a loan officer. The process is fairly intuitive for this type of position while also being thoroughly detailed in ensuring that only the best and most prepared are the ones handling multi-million dollar real estate investment deals.

Become a Mortgage Loan Officer/Originator with Stratton Equities! We’re Hiring!

If you are a licensed Mortgage Loan Originator that is new to the industry and is having a difficult time finding business, we have the solution.

Stratton Equities provides our loan officers with daily direct organic leads, that are from people that call into or apply to our offices looking for a mortgage. Not the other way around. We have a time-tested model that includes a state-of-the-art CRM and lead generation, amazing hands-on training, and the widest range of mortgage loan programs in the industry.

We have niche products that specialize in different types of loans such as Hard Money, No-DOC Loans, Soft Money Loan Programs, Non-QM Loans, Conventional, Fix & Flip, Commercial and more.

Benefits of working with Stratton Equities:

Direct Organic Leads Hands-on Training & Support Largest library of niche loan products – say “YES!” more!

Pay: $158,086.00 – $294,677.00 per year Benefits: 401(k), Dental insurance, Health insurance, Vision insurance

For more information on how to get started as a loan officer, visit Stratton Equities today. We offer the largest variety of loan options that can all be directly accessed by our borrowers. Our starting interest rate is the lowest out of any private money lender, and you can get your loan approved in as little as 24-48 hours.

Additionally, our average time frame in closing loans for our new loan officers is 4-6 weeks after training.

https://www.realestateinvestormagazines.com/wp-content/uploads/2022/11/MORTGAGE-OFFICER.png4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2022-11-02 02:38:002022-11-02 02:38:03How To Become A Mortgage Loan Officer

If you are planning to invest in turnkey real estate development collateralized by real property, one of the top items on your due diligence check list should be to determine which mortgage theory the state follows per the location of the subject property. This understanding can be detrimental to your recovery strategy if your borrower is unable to uphold their end of the deal and defaults on the loan. Each state adheres to either title theory or lien theory, though there are a few states that follow both. In title theory states, Deeds of Trust are the binding agreements utilized between lenders and borrowers, and Mortgages are the agreements utilized in lien theory states. Both documents serve the same purpose in a real estate deal between a lender and borrower, but how they affect the relationship between the parties involved and the subject property is what makes the big difference.

What are some similarities between Trust Deeds and Mortgages?

Mortgages and Trust Deeds both secure repayment of the loan by placing a lien on the property, and are considered, by law, evidence of the debt as they are generally recorded in the county where the property is located. If the borrower defaults on the loan and the lien is in first position, the lien gives the lender the right to take the property back through foreclosure and sell it. In other words, both Mortgage and Trust Deed documents are used as leverage to ensure the borrower pays back the loan in full. The ability to sell the property gives real estate investors and lenders the potential to recoup the original principle lent on the loan. Depending on the value of the property, there is the potential for the recovery of back due interest, late fees, and even capital gain.

What are the main differences between Trust Deeds and Mortgages?

Number of Parties

A Mortgage involves two parties: a borrower (the Mortgagor) and a lender or investor (the Mortgagee). A Trust Deed involves three parties: a borrower (the Trustor), a lender or investor (the Beneficiary), and the title company or escrow company (the Trustee). The Trustees main functions are to hold the title to the lien for the benefit of the Beneficiary and to initiate and complete the foreclosure process for the Beneficiary in the case of default by the Trustor.

Property Title & Foreclosure Processes

The main difference between Trust Deed and Mortgages is who holds the title to the property encumbered by the loan for the duration of the loan term. In a Mortgage State, the borrower holds the title of the property. Therefore, if the borrower defaults on the loan, the lender must go through the courts to take back the property through foreclosure. This is known as judicial foreclosure and this process involves the lender filing a lawsuit against the borrower. This can be a costly and time-consuming process for both parties involved.

In a Trust Deed State, court can be bypassed because the Trustee holds the title to the property. You would follow the non-judicial foreclosure process, which almost always results in faster execution and resolution for all parties involved, especially for the lender. The speed of foreclosure can be detrimental to minimizing carrying costs and getting the property on the market quickly to sell in what may be a more promising market than one met at a later date.

A First Trust Deed is as it implies, is recorded first before any other financial liens on the subject property, whether they be secondary mortgages, trust deeds or even mechanics liens placed by subcontractors. This means the First Trust Deed holds a priority or “senior” position, making all other liens encumbered by the loan subordinate or “junior” to the senior loan. Obtaining first position is important because in a foreclosure scenario, all outstanding subordinate liens are eliminated. This makes it so the lender does not have to worry about reconciling those other debts on top of their own.

Why invest in First Trust Deeds?

Hard money lenders like Ignite Funding, tend to operate more in Trust Deed states. First Trust Deed investments offer an attractive yield with relatively low risk to Ignite Funding investors due to their senior lien position on the property and the foreclosure process that is more conducive to the investors who are the Beneficiaries on the loan. This allows investors to earn double digit annualized returns paid as a monthly fixed income with REAL property as their collateral.

If you are interested in becoming a Trust Deed investor or want to learn more, you can schedule a FREE consultation with an Investment Representative, please click here.

Ignite Funding, LLC | 2140 E. Pebble Road, Suite 160, Las Vegas, NV 89123 | P 702.739.9053 | T 877.739.9094 | F 702.922.6700 | NVMBL #311 | AZ CMB-0932150 | Money invested through a mortgage broker is not guaranteed to earn any interest and is not insured. Prior to investing, investors must be provided applicable disclosure documents.

https://www.realestateinvestormagazines.com/wp-content/uploads/2020/12/scale-2635397_1280.jpg7111280dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2020-12-17 05:02:372020-12-17 05:02:56Trust Deeds vs Mortgages: What’s the Big Difference?

When Congress passed Section 4021 of the CARES Act in response to the effects of COVID-19, their intent was to help borrowers who were having problems making their mortgage payments. Little did Congress realize that they were potentially setting up borrowers for trouble in the future when it comes to credit worthiness as assessed by the lending community.

According to Mark Hanf, president of Pacific Private Money, “Section 4021 of the CARES Act contained a regulation that loan servicers “shall report the credit obligation or account for those participating in forbearance as current”. In other words, those participating in a forbearance program should not see their credit scores drop. However, there is a loophole that allows lenders to discover whether or not a borrower is actually making payments. It is the “comments” section of a credit report. The CARES Act does not mention the comments section of credit reports, and that’s where forbearance notations are going.” What borrowers are not being told is that any reference in a credit report to forbearance can be a Scarlet Letter for an applicant seeking a new mortgage, according to Kathleen Howley in an article she wrote in early May 2020.

According to Hanf, within a week of Howley’s article, his company received a loan request from a home buyer who was denied credit from a major bank for just this very situation. Although the bank sees the existing mortgage as “current” the forbearance has let the world know via the comment section that this borrower has requested a deferment. The major bank involved would most likely not deny the loan on its face due to the deferment, as this would violate the law; however, banks are notorious for coming up with a myriad of reasons for denying a loan and still stay within the guidelines set out for them.

Conventional lenders desire to have plain vanilla borrowers who pay back loans in a timely manner. When a borrower changes terms of the loan by requesting principal forgiveness or other aspects of the loan, the lenders generally do not usually extend credit again to these borrowers and can negatively affect the borrower’s ability to borrow again from unrelated lenders. Such is the case back during the Great Recession wherein some borrowers took advantage of the economic climate by asking their lender to reduce the principal of their loan [total forgiveness rather than just a deferment]. The borrowers may have gotten a reprieve, but the long-term effects may have been more drastic. Similarly, to when a borrower files bankruptcy. The borrower may get out of paying creditors, but their ability to borrow in the future is usually severely hampered.

In one case, back in 2009, during the heart of the Great Recession, one banker tells a story of how a wealthy borrower first asked for a principal loan reduction of $500,000 because his collateralized real estate had decreased and his request was granted. But, when this borrower was faced with the prospects of having this reduction reported on his credit report or the fact that he would have to inform any new lender that he requested a principal reduction [as this question is usually on bank applications], he voluntarily requested that the $500,000 abatement be reinstated. He decided his ability to borrow in the future was worth more than the $500,000 principal reduction.

Borrowers will have to decide if requesting deferments is worth the risk of potential future lending restrictions based upon the lender desire to lend to borrowers who choose to defer mortgage payments when the opportunity arises. Whoever said, “there’s no free lunch” must have been talking about these very situations.

Edward Brown

Edward Brown currently hosts two radio shows, The Best of Investing and Sports Econ 101. He is also in the Investor Relations department for Pacific Private Money, a private real estate lending company. Edward has published many articles in various financial magazines as well as been an expert on CNN, in addition to appearing as an expert witness and consultant in cases involving investments and analysis of financial statements and tax returns.

https://www.realestateinvestormagazines.com/wp-content/uploads/2020/07/set-of-usa-dollars-and-national-flag-4386396.jpg8531280dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2020-07-23 04:51:252020-07-23 04:52:22How Deferment of Mortgage Payments May Affect Borrowers in the Long Run