Investing in real estate is a skill that can be developed over time. However, the skill of real estate investing is composed of sub-skills and traits that add up into the overarching experience and know-how on how to invest in real estate. By understanding the keys of what makes a good real estate investor, you can make the adjustments needed to also become a good real estate investor. The good news is that none of the skills or traits needed to become a successful real estate investor require anything that you wouldn’t have access to.

article continues after advertisement

Develop Your Network

Becoming a good real estate investor involves developing the right relationships and growing your network. Every good real estate investor knows that the right network provides support and opportunities. Who should be included in your network? Focus on finding mentors, other investors, agents, mortgage brokers, lawyers, and potential business partners. You can leverage each individual’s experience to further your own investment goals. Sign up to local real estate organizations and online communities to find individuals to network with.

Stay Educated

A good real estate investor understands the value of constantly learning. It is important to stay up to date with the latest industry news, current events, and changes in laws when it comes to real estate and any other business as a matter of fact. But also, it is important to continue learning new real estate investing related skills and sharpening the ones you already have. Investing in real estate can become very competitive. By taking the time to learn and continue to educate yourself, you can become a good real estate investor and stay competitive in the marketplace.

article continues after advertisement

Focus On A Niche

A jack of all trades is a master of none. There are many different niches within real estate. Most investors fail by trying to tackle them all. Niches such as buy and hold, fix and flip, wholesaling, section 8, commercial, and much more are some of the many niches that an investor can get involved in when it comes to investing in real estate. Take the time to find a niche that aligns best with your goals and approach to investing. Once you’ve chosen your niche, take the time to master that niche. By being the best at one thing, you are setting yourself up for greater success.

Know Your Market

The best place to start investing is in your own backyard. Why? Because you already know the market. You are familiar with the good neighborhoods versus the bad. You know where all the public transportation is and all the best shopping. If you don’t live in the market you are investing in, then still become an expert. Every market is different. The more you know about a particular market empowers you to make better decisions and avoid costly ones. Take the time to truly understand your market and you will be able to spot better quality deals which in turn, will be much more profitable deals.

Joe Arias

Joe Arias and his partners have flipped hundreds of properties in the Southern California Region. He has developed cutting-edge systems to simplify and scale the entire remodel process that can easily be applied to flipping, rentals, wholesaling, and other passive income strategies. More recently, Joe founded a real estate investing education company called RealSuccess Investments, allowing him to share his tools and systems with hundreds of up-and-coming investors.

RealSuccess is focused on education on flipping, rentals, passive income, and wholesaling.

Joe is also a best-selling author. He has written 4 books: Finding your RealSuccess, First Steps to Flipping, R stands for Rentals and Retirement, and Wholesaling Real Estate.

“I came from Argentina when I was 20, I am 40 years old now. I didn’t know anyone, I am CERO generation, usually people say, I am first or second generation but I was the one that crossed the border, no language, no friends, no family, no money, nothing, nada… If I can do it, anyone can.”

From a young latino immigrant to a celebrated real estate investor, Joe is a true testament to hard work and discipline. As an investor, he has made it his mission to help others achieve financial freedom while enjoying living a life of passion, fulfillment, and empowerment.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/05/real-estate-key.png4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-05-22 05:07:082024-05-22 05:07:09KEYS TO BEING A GOOD REAL ESTATE INVESTOR

“Divide your portion to seven, or even to eight, for you do not know what misfortune may occur on the earth.” The Bible – Ecclesiastes 11:2

This is good advice as long as you don’t get so spread out that you are doing too many things but nothing with success. It’s important we understand the fine line between focusing on one real estate niche without putting all your eggs in one basket, (so to speak).

To simplify the terms of real estate investing, there are really only three ways for investors to make money in real estate:

Real Estate Appreciation and Equity

Cash flow while you own it

Assignments: Payment when you flip a real estate contract without owning it.

So where do you start? Let’s try to answer this question on every aspiring real estate investors mind. Since real estate investing encompasses so many types of exit strategies or I like to call profit centers, it’s important to study and pick those you are most passionate about. otherwise called exit strategies.

article continues after advertisement

The following is a summary of Ten of the Most Popular Real Estate Investment Strategies with their advantages and disadvantages.

1. Rentals or Cash flow Investment Property: These types of investment properties are the ones which generate rental income. These are mainly apartment buildings and rental houses.

Advantages:One of the easier ways to get started, and good long term return on investment while also earning monthly income.

Disadvantages: Risk of not renting property leaving you with the mortgage payment and no income. Property management can be a challenge. You typically will wait awhile to sell your property so payoff is slow.

2. Lease Option. This is when you buy a property, then sell to someone else via a rent-to-own arrangement.

Advantages:You get higher rent, and the buyer is usually responsible for maintenance. Cash flow can be good.

Disadvantages: Most rent to own buyers don’t complete the purchase (this can be an advantage too, but it does mean more work for you). Bookkeeping must be done properly and can be complicated.

3. Fixer Upper Investment Property. These types of investment properties are the ones which are in ugly condition and need renovation. These properties can be acquired to flip after fixing-up quickly or held to rent out.

Advantages:You can receive a quick return on your investment (months). You usually get below market value pricing on properties bringing you instant equity.

Disadvantages:Higher risk. (Many unpredictable expenses come up in construction). You get taxed heavily on the gain when you sell in under a year.

4. Vacant Land. Many options including just holding while appreciating. You can also split it and sell it.

Advantages:History has shown that land always appreciates in value (it’s the buildings on the land that go down. It is simpler than most real estate investments, with the possibility of great profits.

Disadvantages: It can take a long time to increase in value. You have expenses, but no cash flow while you wait unless you sell the contract before closing.

5. Commercial Real Estate. These are any building containing 5 units or over and/or buildings sited for commercial use.

Advantages: Long term triple-net leases mean little management and high returns. Lending is usually based on the value of the property vs. personal credit.

Disadvantages:Commercial property valuation requires a more complex method, taking into account the income potential of the property. This is recommended for the more experienced investors as there is a lot more involved to set up and maintenance.

6. Buy property with Forced Appreciation. Buy in the path of growth and holding until values rise. For instance buying a lot in a residential development prior to roads being completed.

Advantages: Can yield large profits, especially if you buy low to start.

Disadvantages:Future price is not predictable – the market can turn, the developer can go out of business. You have expenses with no income while you’re waiting.

7. Preconstruction Investment Property: These types of investment properties are acquired directly from a developer before the construction or renovation is completed.

Advantages: Low money out of pocket to tie up property while being built. If purchased in appreciating markets, you make money in equity at closing and can instantly re-sell at a profit.

Disadvantages: You can’t always predict what a market is going to do. If market depreciates, you have lost money. Also higher tax rates in selling quickly.

8. Pre-Foreclosure Investment Property: These types of investment properties are the ones which you buy from sellers who are behind in their payments and may lose their property to the bank via foreclosure.

Advantages:You have opportunities to buy properties at below value pricing – “Instant equity”.

Disadvantages: Legal liabilities are higher. Finding these properties requires a lot research and footwork to find a deal that works. You can do all the work and still not have a deal with enough equity to profit after expenses to sell, (taxes, realtors, etc).

9. Assignments: This strategy has you get into a property at a discount, preferably with a known buyer in place before you commit to your purchase. After you are in contract to purchase a property, you would sell your contract for a fee to someone else. For example you get into purchase contract to buy a $120K property for $100K. You turn it to an investor for $110K and profit $10K cash without the cost and hassles of ever closing on the deal.

Advantages:This is a great way to make quick cash with low or no upfront investment, low risk and fewer headaches from closing and ownership. This strategy creates a win win win outcome for everyone involved.

Disadvantages:This will only work if the property you are buying has equity so that you may buy it a discount. In declining markets, this type of property is harder to find. Also when dealing with banks on REO’s or Short Sales you will find they will not allow you assign your contract. However, there are ways to get around this if you plan and handle the contract correctly up front. Do you want to know how I have managed to get around not being able to assign a contract? I have purchased properties in the name of an LLC set up exclusively to buy properties. I then sold the LLC to someone, making them the owner of the LLC, therefore making them responsible for closing on the purchase contract and end buyer of the property.

10. Flipping – Wikipedia defines Flipping as is a term used primarily in the United States to describe practice of buying an asset and quickly reselling (or “flipping”) it for profit ..

This description pretty much explains property flipping, with there being a slight difference from that description of flipping assets. In real estate you can get into an agreement to flip a contract you have gotten into before you even buy it. This can be done with ease when you know exactly what your buyers want and with no money out of your pocket utilizing transactional funding. Flipping can also mean closing and quickly reselling your property, sometimes even doing both transactions the same day – this being subcategorized a “double closing”.

Advantages: My favorite strategy. You work the deal backwards. You create relationships with buyers who can close quickly with cash. Then you find a property meeting the needs of your buyers. This strategy allows you to profit literally from no money down, with lower risk and very little of your own time.

Disadvantages:The law requires you to disclose your intent to resell quickly to sellers. When dealing with banks, this can sometimes cause your offer to be rejected. You must buy properties in the name of an LLC in order to utilize transactional funding. Setting up and maintaining an LLC will cost you money. Though the intent of a buyer might be to close on the transaction, sometimes “life happens” and something causes the buyer to be unable to follow through. You may have to walk away from earnest money if you cannot find another buyer quickly

article continues after advertisement

Now that you that you have learned strategies to consider, you will need to consider the type of properties you want to go after, developing a marketing strategy to find motivated sellers of those deals. Over the next months I will be sharing steps and strategies on how to profit investing in real estate 12 different ways.

Please leave a comment if you have anything you would like add to what I have written here with the heart to support fellow real estate investors. (Any solicitations for business will not be published) I appreciate the feedback!

Tamera Aragon

Tamera Aragon is a professional online entrepreneur and has bought and sold over 300 properties, establishing her as an expert in the real estate investing field. Since 2003, she has purchased over 10 million dollars in real estate and currently holds properties all over the world. Tamera’s focus is on the booming Foreclosure market, buying Pre-foreclosures, REOs and Short Sales. Tamera who is a noted Author, Success Trainer, Speaker & Coach, shows her passion for helping others with the 17 websites she has created and several specialized products to support fellow investors throughout the world. When Tamara is not busy running her website, she is very involved with her Fiji joint ventures and investments. Tamera Aragon is one of the few trainers and coaches who is really “doing it” successfully in today’s market. Tamera’s experience has earned her a solid reputation in the industry as well as the respect and friendship of many of the top national real estate investment and internet marketing experts. Tamera Aragon believes her success has garnered her the financial freedom to fully enjoy her marriage and spend quality time with her children.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/05/multiple-investments.png4801200dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-05-17 03:58:102024-05-17 03:58:1110 Roads To Real Estate Investing Profits

Discover the Latest Insight, News and Investment Strategies at Realty411’s Real Estate Investor Summit in Southern California – Network with Sophisticated Investors.

A Slower Market Equals Increased Opportunity- Be Prepared for Real Estate Deals!”

Sophisticated investors and top producers take note, Realty411’s new in-person Real Estate Investor Summit in Southern California is scheduled for Saturday, August 3rd.

This highly-anticipated REI conference will take place from 9 am to 5 pm in Culver City, California. Doors open at 8:30 am, guests should arrive early for maximum networking.

Tickets for Realty411’s Investor Summit are now available, CLICK HERE. This special one-day conference will host incredible educators from around the country, who are ready to share their valuable insight with guests.

Realty411 has united thousands of investors from across the nation since 2007. Guests will receive our latest publications featuring wonderful resources, insightful news, and educational articles.

Let’s unite to network and learn in Southern California. Connect and learn from top real-estate investment educators. Subjects to be discussed include:

Now is the moment to grasp the opportunity to connect and learn from top educators, investors and service providers from around the nation! Be sure to upgrade as a VIP Guest to join us for a delicious lunch as well.

Pencil in this date now and join us in-person to gain specialized insight and knowledge. The information shared on this SPECIAL day could catapult your portfolio to new levels.

This one-day conference has something for everyone regardless of their experience level in real estate. Join this memorable day and receive knowledge for a lifetime. Agents/brokers, discover new ways to acquire solid leads and prosper in a competitive industry climate.

This is Your Chance to meet TOP Leaders in REI, Local & National Experts:

Learn from Leaders & Industry Pros

Meet Local PLUS Out-of-Area Investors

NON-Stop Tips for Real Estate Success

Bring Lots of Business Cards

This event is produced and hosted by Realty411.com. For over 17 years, we have dedicated our time, resources and energy to help expand real estate investing knowledge and education by producing magazines, virtual conferences, webinars, podcasts, and live events. Discover what Realty411 can do for you!

Meet Local Leaders & Industry Giants – From Coast to Coast

Influential Real Estate People & Business Owners Are Attending

Learn How to Leverage and Meet Private Capital Lenders

Find Potential Partners, New Friends, Build Your Circle of Influence

Your Net Worth = Your Network — Don’t miss this event

Mingle with Leaders & Industry Professionals Here

Please bring LOTS OF BUSINESS CARDS, it’s time to Network! Learn more about our magazines and our company sponsors and resources, visit Realy411.com

Discounted parking available for $4. Upgrade to a VIP ticket to enjoy special bonuses, including coffee and lunch.

Be sure to download the latest print Realty411 magazine to learn more about real estate investing, CLICK HERE. Since 2007, Realty411 has reached thousands of investors nationwide with their print publication.

We also produce a special edition digital magazine REI Wealth, which is the longest-running digital magazine for real estate investors. Our digital, interactive issue is designed to be read and viewed online, CLICK HERE.

An absentee owner is an owner that does not live in/on their property; most absentee owners utilize the services of property management companies to take care of their properties for rent.

These types of owners, can turn out to motivated sellers and are the most obvious. A lot of the time, they are also the most overlooked motivated sellers on the planet.

article continues after advertisement

Why this is a good niche to consider?

It is an untapped market.

Most investors don’t realize the impact that marketing to this group of prospects can have on your real estate business.

Most investors don’t know how to market effectively to absentee owners, focusing on their hot buttons.

The paperwork is simpler

All you need is a contract.

What are downsides of this niche?

Absentee Owners can sometimes be hard to find

You don’t know how motivated they are when you market to them. You could be marketing to someone who is not motivated to sell at all.

Good market conditions.

When there is a mid to high rental vacancy rates.

When the rental rates are low.

When Interest rates are high.

In a flat or steady market.

Bad market conditions.

When there are low rental vacancy rates.

When the rental rates are high.

Steps to do this Niche.

Get a list of Landlords from recommended sources below

Sort the list taking removing the following: *Duplicates & corporations *Square footage over 900 *Anyone who has owned their property less than 10 years.

Use direct mail postcards to inexpensively contact them.

Sellers will call your 24 hour hotline to listen to a 2-3 minute message.

Only the most interested ones you will call back and run comps

If owner is motivated then set time to see property and meet owner.

Tamera Aragon is a professional online entrepreneur and has bought and sold over 300 properties, establishing her as an expert in the real estate investing field. Since 2003, she has purchased over 10 million dollars in real estate and currently holds properties all over the world. Tamera’s focus is on the booming Foreclosure market, buying Pre-foreclosures, REOs and Short Sales. Tamera who is a noted Author, Success Trainer, Speaker & Coach, shows her passion for helping others with the 17 websites she has created and several specialized products to support fellow investors throughout the world. When Tamara is not busy running her website, she is very involved with her Fiji joint ventures and investments. Tamera Aragon is one of the few trainers and coaches who is really “doing it” successfully in today’s market. Tamera’s experience has earned her a solid reputation in the industry as well as the respect and friendship of many of the top national real estate investment and internet marketing experts. Tamera Aragon believes her success has garnered her the financial freedom to fully enjoy her marriage and spend quality time with her children.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/05/wealth.png4801200dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-05-13 04:29:002024-05-13 04:29:01Niches That Bring Your Riches: Absentee Owners

Want to make money without having to put in a lot of work? You may want to consider passive real estate investing. It is the perfect solution for an aspiring investor who may have other time commitments like a full-time jobs that does not allow much time to be a property manager or a home flipper. Each of those activities requires at least a little bit of time on your part. You have to collect rent, market your property for rent, make repairs, and so forth.

With passive real estate investing, you basically write a check and then sit back and collect money over time. There are a couple of different options when you get into passive real estate investing, each comes with its own risks and varied amounts of returns. They are pretty easy to get in to and do not require a lot of knowledge in the real estate industry to be successful. Here are several passive real estate options worth looking into:

article continues after advertisement

What is Passive Real Estate Investing?

Before we jump into what types of passive real estate options are out there, let’s first look at what passive real estate investing is.

In simplest terms, passive real estate investing is investing in real estate without requiring hands-on effort or active participation. Passive real estate investing can either be direct or indirect. The main difference between the two is the amount of work you have to contribute to each investment.

Why Is Passive Investing a Good Idea?

When you are a passive real estate investor, you will earn money without having to actively work for it. Basically, you pay someone an agreed upon amount of money and they do all the hard work for you. Here are some ways you can put your passive income to use:

Build a retirement fund.

Pay off your debts.

Increase your savings account.

While there are non-real estate related ways to earn passive income, let’s just focus on those that do involve real estate in some form. Here are a few ideas for you on how to invest in passive real estate:

Direct passive real estate investing

In this case, an investor will purchase a property, which is then rented out to a tenant. This can be done in the form of short-term or long-term rentals. In order to simplify the process, many investors will hire a property management company to do time-consuming duties like maintenance, rent collection, or any other situations that may arise. This allows the investor to have very little active responsibility in their investment, making it a passive investment.

Indirect passive real estate investing

Suppose you want something that requires even less involvement than being a landlord and renting out a property to a tenant. In that case, you can invest in an indirect passive real estate investment by investing in a real estate investment trust (REIT). You will have no day-to-day tasks related to this form of investment and do not need to have very much real estate knowledge to be successful. You will still collect income in the form of returns and dividends.

Different Types of REITs

Real estate investment trusts are made up of corporations, trusts, or associations. These groups invest in large income-producing real estate like commercial buildings, hotels, data centers, or apartment complexes. Investing in a REIT is usually a low-risk investment and is traded like a stock.

There are three types of REITs you can invest in:

Exchange-traded: Registered with the SEC and listed on exchanges like the NYSE.

Non-traded: Registered with the SEC, but do not trade publicly. These tend to be more stable since they do not fluctuate with the market.

Private: Not registered with the SEC or traded on exchanges. They raise funds through private investors.

article continues after advertisement

A well-managed REIT lessens risk by including large groups of properties rather than individual properties. One good thing about them from an investment standpoint is that they provide annual dividend income as well as long-term appreciation. You are usually able to withdraw money from the REIT when you need it, but will be subject to paying taxes on your returns.

There are a couple of downsides to investing in REITs. They are required to distribute 90% of their profits annually, which means they are not able to reinvest funds annually, which can prevent long-term growth. You also don’t have a tangible asset and cannot control any part of the decisions made related to your investment.

Tax Liens

Another passive real estate option is investing in tax liens. According to the National Tax Lien Association, $14 billion in property taxes go unpaid each year. When a homeowner falls behind on their property taxes, the county or municipality where the property is located will issue a tax lien against the property, which the tax assessor’s office usually issues.

These tax liens can be auctioned off to investors. If you win a tax lien auction, you will earn interest until the homeowner pays off the outstanding taxes. You receive your share and accrued interest when the homeowner sends the county a tax payment.

Interest rates on a tax lien can be as high as 12%, which would give you a very nice return on investment. In very rare cases, you may even be able to foreclose on and acquire the property for an incredibly low price.

Tax lien investing can be confusing and may be more work than a passive real estate investor is willing to commit to. Depending on the state you purchase the tax lien from, you may be required to notify the homeowner frequently in an attempt to collect the debt. This is certainly not for everyone.

Crowdfunding

Another type of passive real estate investing is crowdfunding. With real estate crowdfunding, groups of investors combine their money to purchase commercial properties, apartment complexes, and single-family home portfolios. These are mostly managed and executed through online platforms where investors are able to view progress and send payments.

Crowdfunding is very popular because it is so easy and does not require a large investment. Neighborhood Ventures is a Phoenix-based real estate crowdfunding company. Their projects are usually funded in a matter of days. They buy old apartment buildings, renovate them and then rent them to tenants. They take on projects in their own neighborhoods in an attempt to keep their investment dollars local and improve the communities where they live and work. Investors can very easily and quickly create an online account, upload their funds – as little as $1,000, choose a project, and watch their money grow.

Crowdfunding is another very hands-off investment. Since there are so many crowdfunding companies that are very transparent in the properties they will be purchasing, you do have the ability to choose a project in a real estate market with the potential for large returns. With a company like Neighborhood Ventures, you would be investing in the Phoenix Metro area, which is one of the hottest real estate markets in the country, seeing double-digit returns each year.

Many real estate crowd funders do require holding your money for a specified period of time. This ties up your money and makes it difficult or impossible to cash out at a moment’s notice in the case of an emergency.

Passive Real Estate Investment or Stocks? Which is the Better Investment?

Deciding between real estate or stock investments is a personal choice that depends on your financial situation, risk tolerance, and goals. You can make money two ways with stocks: value appreciation as the company’s stock increases and dividends. Your returns are based on stock market activity as well as the company’s earning.

Real estate has proven to bring in higher returns in a shorter period of time in most major real estate markets. According to the S&P 500 Index, the average return on investment in the U.S. real estate market is 10.6%. Comparatively, the average annual return for the S&P Index over the past 20 years is only 8.6%. Real estate also tends to be less volatile than the stock market. REITs and crowdfunding reduce the risk further since you are able to enter into the investment for little money out of pocket.

Overall, real estate and stocks both present risks and rewards. There is no right way to invest and people have seen both huge returns as well as huge losses by investing with each.

Risks in Passive Real Estate Investing

Every investment comes with a series of risks, and passive real estate investing is no different; you carry the ongoing threat of losing your principal. First, if you are hoping to make a lot of money through passive real estate investing, you may be disappointed. Something else to be aware of is that there are a lot of passive real estate investment opportunities out there, and they are not all created the same. Always do your due diligence before investing, as no investment can guarantee you either a return or even protection of all your principal. Performing your own due diligence can help you find safer and possibly more profitable investments for your capital.

Here are some things to look out for when considering investing:

What is the company’s track record? You could take a look to see their past projects and how much money they made. If the company is consistently failing to complete projects or are not generating the returns they advertise, you may want to pass.

How much debt is the company in, and what are the details? Look to see if their debt is due to mismanagement. If so, this is another red flag, and you should probably pass.

What do other investors say about the company? You should be able to find online reviews about them.

Do they communicate with their investors? It is usually not a good sign if you invest money and then have no idea what the project’s progress is.

The Bottom Line

Many investors have made a lot of money through passive real estate investing. If you find the right REIT or crowdfunding or other passive real estate investment company to invest in, you can make money while you sleep. So, if you are looking for an easy, low-cost investment, passive real estate investment may be your best bet.

Joe Arias and his partners have flipped hundreds of properties in the Southern California region. He has developed cutting-edge systems to simplify and scale the entire remodel process that can easily be applied to flipping, rentals, wholesaling, and other passive income strategies. More recently, Joe founded a real estate investing education company called RealSuccess Investments, allowing him to share his tools and systems with hundreds of up-and-coming investors.

RealSuccess is focused on education on flipping, rentals, passive income, and wholesaling.

Joe is also a best-selling author. He has written four books: Finding your RealSuccess, First Steps to Flipping, R stands for Rentals and Retirement, and Wholesaling Real Estate.

“I came from Argentina when I was 20, I am 40 years old now. I didn’t know anyone. I had no friends, no family, no money, nothing, nada. If I can do it, anyone can.”

From a young Latino immigrant to a celebrated real estate investor, Joe is a true testament to hard work and discipline. As an investor, he has made it his mission to help others achieve financial freedom while enjoying living a life of passion, fulfillment, and empowerment.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/05/passive-income.jpg4801200dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-05-09 03:18:172024-12-05 04:25:16PASSIVE REAL ESTATE INVESTING

The purchasing power of the dollar continues to rapidly decline, sadly. This weakening dollar trend hasn’t just happened in recent years. Rather, it’s been going on since the formation of the Federal Reserve back in 1913. One dollar in 1913 now has the equivalent purchasing power of about 2 cents today.

Yet, the purchasing power has rapidly decreased at a seemingly accelerated pace since 2020 when the worldwide pandemic declaration began.

As per a home unaffordability study shared by Redfin and Visual Capitalist on April 4, 2024, an “unaffordable” home is defined as a new listing with a monthly mortgage payment that is no more than 30% of the median monthly income in its county.

article continues after advertisement

Here are the findings from this unaffordability report:

Only 16% of U.S. homes for sale were affordable in 2023, which was an all-time record low.

By comparison in 2021, 39% of listed properties were considered affordable.

With just 0.3% of home listings deemed affordable, Los Angeles has the lowest share of affordable listings in America.

By contrast, Detroit had the highest share of affordable listings with over 51% of homes.

Let’s take a look at how the unaffordable housing numbers have rapidly fallen over the past 10 years:

Seventeen of the top 20 most unaffordable U.S. cities to buy a home are located in either the counties of Los Angeles, Orange, or San Diego in Southern California. The other three cities are in Northern California. This is a national study created by the real estate tracking agency Construction Coverage, not just for California.

This data report compiled by Construction Coverage took a closer look at cities of all sizes, while focusing on the ratio of home prices to household income as the core basis for determining how affordable a region is these days.

The Top 3 most unaffordable cities in this study were as follows:

1. Newport Beach, CA: Median home price of $3.23 million; median household income of $127,353; and a home price-to-household income ratio of 25.4.

2. Palo Alto, CA: Median home price of $3.41 million; median household income of $179,707; and a home price-to-household income ratio of 19.

3. Glendale, CA: Median home price of $1.17 million; median household income of $77,483; and a home price-to-household income ratio of 15.2.

There are many regions across the nation with median home prices much higher than these Top 3 unaffordable housing regions. However, those regions generally have much higher household income to make the home price-to-household income much lower.

The California cities in the top 20 of the report are: 1. Newport Beach 2. Palo Alto 3. Glendale 4. Los Angeles 5. El Monte 6. Costa Mesa 7. El Cajon 8. Inglewood 9. Hawthorne 10. Sunnyvale 11. Irvine 12. Huntington Beach 13. Torrance 14. Garden Grove 15. San Jose 16. Anaheim 17. Long Beach 18. East Los Angeles 19. Carlsbad 20. Tustin

article continues after advertisement

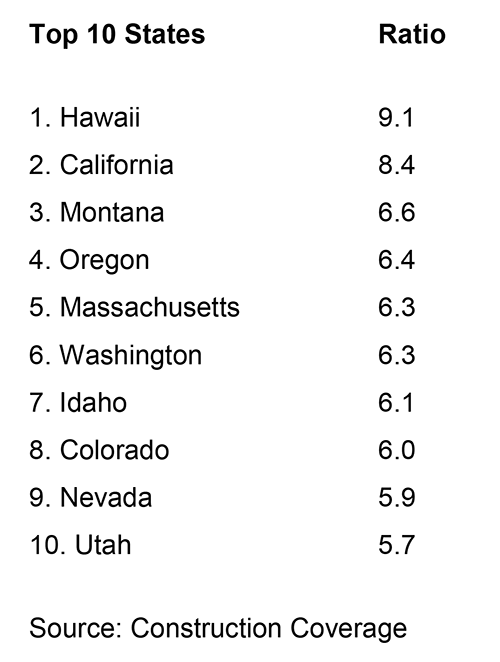

States With the Highest Home Price-to-Income Ratios

Toughest Regions to Save Money

The national personal savings rate has dropped from record highs of over 20% in 2020 and 2021 to 3.8% as of January 2024, according to Forbes. Many Americans these days couldn’t come up with $400 in cash for an unexpected emergency, partly due to rising grocery, gas, utilities, housing (own or rent), clothing, restaurant, entertainment costs, and how high or not the state income taxes are there.

Let’s focus on how high certain foods have risen since 2019 to better understand why things seem so much more unaffordable these days:

The Riverside-San Bernardino-Ontario metropolitan area is ranked as the #1 most challenging place in America to save money with the Los Angeles-Long-Anaheim metropolitan region ranking second.

The list of America’s hardest metropolitan regions areas to save money in is listed below:

1. Riverside-San Bernardino-Ontario 2. Los Angeles-Long Beach-Anaheim 3. Miami-Fort Lauderdale-Pompano Beach, FL 4. New York-Newark-Jersey City, NY-NJ-PA 5. Atlanta-Sandy Springs-Alpharetta, GA Sources: Forbes Advisor and KTLA

The top ten most difficult states to save money in can be viewed below: 1. California 2. Hawaii 3. Nevada 4. Oregon 5. Maryland 6. Florida 7. New York 8. South Carolina 9. Colorado 10. Louisiana Source: Forbes Advisor and KTLA

Rental housing changes: According to data shared by Zillow and NerdWallet, the average U.S. rent was $1,958 in January 2024. This is +29.4% more expensive than before the pandemic declaration in March 2020.

Rising Taxation Risks

Our federal government debt surpassed $34 trillion earlier this year. It’s now growing at a pace of an additional $1 trillion every 90 days, which is an annual new debt pace of $4 trillion per year. For comparison purposes, it took 10 years for the federal debt to increase by $2 trillion between 1980 and 1990.

The White House is seeking to raise another $5 trillion in tax revenues starting next year in 2025 to help offset the increasing size of our budget deficits. For real estate investors, you and your tax advisors should stay focused on these proposals that may more than double the capital gains rate and possibly eliminate the 1031 tax-deferred exchange option, which helps to defer capital gains taxes over a much longer period of time.

If this 2025 budget proposal is enacted, California residents will be looking at upwards of a 59% federal-state capital gains income tax rate starting in 2025. It also may make significant negative changes to the “death tax” for heirs. Don’t be surprised if Americans start selling assets here in 2024 on a larger scale to avoid these much higher capital gains taxes next year.

Additionally, the White House’s 2025 budget proposal includes the creation of a minimum tax equal to 25% of an individual’s taxable income and unrealized capital gains for assets that weren’t even sold for certain higher income people, as per multiple sources including Quoth The Raven.

The combination of increasing all types of taxes (state, federal, capital gains, and possible unrealized tax gains) plus the potential elimination of the 1031 tax-deferred exchange for rental properties will hurt real estate values at some point.

All-Time Record Credit Card

Credit card and overall consumer debt are at all-time record highs along with the total rates and fees (APRs). Credit card defaults are now at the highest level ever or at least since 2012, when the Fed started tracking this data.

Average APRs are fluctuating between 27% and 33% these days for many consumers. It wasn’t that long ago when credit card APRs were closer to 12% about 10 years ago or so.

All stages of credit card delinquency (30, 60, and 90+ days) rose during the fourth quarter of 2023, according to data shared by the Federal Reserve Bank of Philadelphia.

Freddie Mac Bailouts for 2nds

Freddie Mac may soon start purchasing funded home equity lines of credit (HELOCs) in the secondary market, as per multiple sources including HousingWire.

A new multi-trillion dollar stimulus package of up to $2 trillion is being prepared, by way of the government-backed Freddie Mac entity, so that it’s easier for banks and mortgage companies to offer 2nd loans, which will then be quickly sold off to Freddie Mac.

In recent years, a larger number of banks and mortgage companies stopped offering HELOCs due to the perceived risk, especially for liens in 2nd position. If lenders may soon be able to quickly unload the funded HELOCs over to Freddie Mac, they may be inspired to offer these types of riskier loans again.

Whether it’s a federal bailout of lenders, homeowners, small businesses, billion-dollar corporations, or consumers drowning in credit card or student loan debt, all of these actions are inflationary and will likely make the dollar weaker and weaker.

Because government spending is likely to keep exceeding all-time record highs, these inflationary actions may help boost real estate values that are generally hedged against inflation.

Please try to pay off any double-digit consumer debt, set aside cash for you and your family if possible, and keep your eyes wide open for potential discounted real estate bargains in a neighborhood near you.

Rick Tobin

Rick Tobin has worked in the real estate, financial, investment, and writing fields for the past 30+ years. He’s held eight (8) different real estate, securities, and mortgage brokerage licenses to date and is a graduate of the University of Southern California. He provides creative residential and commercial mortgage solutions for clients across the nation. He’s also written college textbooks and real estate licensing courses in most states for the two largest real estate publishers in the nation; the oldest real estate school in California; and the first online real estate school in California. Please visit his website at Realloans.com for financing options and his new investment group at So-Cal Real Estate Investors for more details.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/05/house-graph.jpg4801200dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-05-07 03:04:192024-05-07 03:04:20Unaffordable Housing, Taxation, and Consumer Debt Trends

“Real estate is definitely a path to be seriously considered in building your wealth. Where to invest varies depending on the location of the investment as well as market timing. My investment choices change as often as the market does. Being sensitive and aware of changing market trends is helpful to know where to invest and the most profitable strategy to follow”.

What was just quoted was a highlight to part of this real estate investing article series of minimizing risks and maximizing profits for investors. You can review the first 3 rules here: “Top 7 Tips To Minimize Your Risk & Maximize Your Profits P1”.

article continues after advertisement

Top 7 Tips To Minimize Your Risk & Maximize Your Profits

Rule #4 – Use a Tried and True Strategy

Why make all of the mistakes others have already made if you don’t have to? Find a good investment strategy that works with your goals and stick to it. You will be tempted and pulled in many directions by all the different gurus out there saying their way is best.

Find a mentor and coach with experience in today’s market and then follow where they lead. After all, why would you walk through a mine field alone if there was someone else familiar with the route who could lead you safely through?

Rule #5 – Have Attorney Review Contracts

Hire a professional real estate attorney to review all your processes and paperwork before utilizing it in your market. Because most trainers and coaches are not attorneys, as much as we try, we cannot be experts on laws in every state in the U.S. For this reason, it is vital for you to make sure the contracts and steps you are taking are not going to lead you to the courthouse.

Anyone can sue anyone these days. The way to avoid this is to first of all, always be nice and come from a place of caring in your dealings with others. Don’t avoid dealing with situations personally or you may find a costly summons to court forcing you to deal with things the expensive way. A second way to avoid litigation is to assure your paperwork and procedures are legal to the best of your ability.

I know attorneys can be expensive which is why I signed up to use a service that offers me unlimited consultations and a certain number of document reviews for only $50.00 a month. I recommend this way to be the most cost effective resource to be able to accept advice from a licensed real estate attorney in any state.

Rule #6 – Have Basic Computer Skills

You will want to know how to use email, internet and office products like Microsoft Word and Excel (Google had free versions of these). It is helpful to know how to create graphics but not necessary. You will need high speed internet to enjoy utilizing this wonderful tool and avoid the frustration of being unable to watch videos and waiting for pages to load.

You can do your entire real estate business from a computer. You will absolutely need to type contracts and do research and there is no faster, easier way than this. If you do not know how to use email, the internet and basic word on a computer, find a class you can take to learn the skills you lack. If you have tried to do business without these tools, you will find them to turbo-charge your business once you have them.

article continues after advertisement

Rule #7 – Diversify Your Investments

Don’t put it all into one area or one type of real estate. So how did I go from having no money to the prosperity I enjoy today? It started with a book called the “One Minute Millionaire” by Mark Victor Hansen and Robert G. Allen. This book showed me I could really have the kind of lifestyle I desired, if I would diversify my income, while at the same time making wise investments.

I studied this philosophy on money found in this book as well as in others like it. Then, I did something many are too afraid to do, “I put what I learned to work in my life”. I currently divide my income into various investment strategies such as real estate, stocks, business ownership, savings, Money Market, IRA’s, and others.

However, since I see that 40% of today’s billionaires made it in real estate, I have chosen to place a large percentage of my time and money into this strategy. What type of real estate do I invest in? This varies about every 6 months depending on the market conditions as I mentioned earlier. I also have relationships with “power team” of experts so we have all the correct data to consider our strategy as the market changes.

In summary, there is no hard fast rule that applies to all investing – except one. That is this. In order to profit from your investments, we have found it important to diversify them. Consider different types, different areas and different strategies that make the most sense, therefore bringing you the highest return on your investment.

Tamera Aragon

Tamera Aragon is a professional online entrepreneur and has bought and sold over 300 properties, establishing her as an expert in the real estate investing field. Since 2003, she has purchased over 10 million dollars in real estate and currently holds properties all over the world. Tamera’s focus is on the booming Foreclosure market, buying Pre-foreclosures, REOs and Short Sales. Tamera who is a noted Author, Success Trainer, Speaker & Coach, shows her passion for helping others with the 17 websites she has created and several specialized products to support fellow investors throughout the world. When Tamara is not busy running her website, she is very involved with her Fiji joint ventures and investments. Tamera Aragon is one of the few trainers and coaches who is really “doing it” successfully in today’s market. Tamera’s experience has earned her a solid reputation in the industry as well as the respect and friendship of many of the top national real estate investment and internet marketing experts. Tamera Aragon believes her success has garnered her the financial freedom to fully enjoy her marriage and spend quality time with her children.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/04/real-estate-investment.png4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-04-22 04:57:292024-04-22 04:57:31Tips To Minimize Your Risk & Maximize Your Profits (Part 2)

It’s time for our educational Virtual Investing Summit uniting readers for an amazing day.

Investors, don’t forget to register for our NEW Virtual Investing Summit on Friday, April 26th, from 9 AM to 2 PM PT (East coast time: 12 PM to 5 PM ET) and Saturday, April 27th, from 9 AM to 2 PM PT as well.

Guests can join Realty411‘s complimentary VIRTUAL Investing Summit and learn from experts sharing important knowledge, strategies and insight.

Realty411 will virtually unite some of the most successful, knowledgeable and savvy investors in the REI (Real Estate Investing) industry to help our readers make educated and informed decisions.

Join us for an amazing day of real estate education. Every online event we produce is unique, so be sure to reserve this day for REI learning at its best.

Some of our special educators are listed below, more experts to follow.

“Without effort, you cannot be prosperous. Though the land be good, you cannot have an abundant crop without cultivation.” – Plato

article continues after advertisement

Real Estate As a Path To Wealth & Freedom

Forbes magazine lists the top 400 wealthiest people every September. In September 2007, 40 of the 400 people on that list made their billions specifically in real estate. Many of these people started with nothing, some immigrants even, to move up into this category. Real estate is definitely a path to be seriously considered in building your wealth. Did you know that most of those 40 billionaire real estate investors are only doing their real estate part time? And do you realize they can run their real estate investing business from anywhere in the world?

Freedom… Just the sound of that word brings a smile to my face. Real Estate investing offers you the freedom to make your own choices about how and where you spend your time along with who you spend it with. Financial and time freedom is definitely something successful real estate investors enjoy.But what about the risks you say? Of course for every “tit” there is a “tat”, for every high a low, for every good a bad. Yes, unfortunately like any entrepreneurial venture, there are risks. My husband owns a retail store and he risks every day that someone is going to trip and fall and sue him. He risks that he may not sell enough to pay his bills, etc. I think you get the point. However there are steps you can take to minimize your risks and maximize your profits.

Top 7 Tips To Minimize Your Risk & Maximize Your Profits

Rule #1 – You Do Not Need To Re-Invent “The REI Wheel”

You will need to get training and have a mentor or coach, (or maybe several), in order to succeed. Even the best athletes in the world have a coach. Why? Because a coach will keep you on track. Don’t try to do it on your own. That school of hard knocks is going to cost you way more than good training and an experienced coach. I believe this to be the first step in minimizing your risks and maximizing your profits.

Rule #2 – Do Your Due Diligence (or as I say, “Do the Due”)

Would you buy a car without checking the engine, tires, brakes, or interior? Would you marry someone without learning all you can about them and knowing their flaws and good things before you take the plunge? I hope not!! Then why do so many real estate “investors” buy a property without doing the proper due diligence before they get into a contract?Answer: Many simply lack the knowledge of what to look for in a property when considering it for investment purposes. In other words, you don’t know… what you don’t know, right? So here’s what you need to know. Before you ever buy a piece of real estate you should check it out from top to bottom so you know exactly what you are getting into. A little bit of work upfront will save you huge headaches and money down the road.

article continues after advertisement

People often ask me, “What should I look for before committing to buy a property?” There are two ways to make money in real estate. If the property is going to supply these profits for you, you would want to consider it.

When the property brings you cash flow from monthly rents while also appreciating.

When you make a profit re-selling the property through appreciation.

Now keep in mind, you can profit from appreciation two ways.

Market appreciation – the economy is causing properties to increase in value.

Forced appreciation – when you either buy property cheaper than what you can resell it for or you can do some improvements to increase the value more than what you spend.

Here are Three Most Important Questions I ask myself before I consider a property for investing?

Would we buy it for ourselves?

Would we want to tell our friends and family?

Is this a good deal for other real estate investors?

The most important outcome to consider is if the answer to this question is yes, “Will my money put into this property make me more money?”I call what I do real estate “investing”, not real estate “divesting”. You will always want to do the same. How do you know if it is going to make money? You do your due diligence before you commit to buy any property. Of course, as you know, there are never any guarantees in life.

However, if you have certain criteria every property needs to meet in order to profit and how to evaluate a property for those qualities, the likelihood that you will succeed are much greater. It’s very easy to get caught up in wanting to help people if they need to sell their house. Or you may just personally think a property is good looking. But those are not the only reasons you would want to buy. To avoid getting emotionally involved in a property purchase, I have created a due diligence checklist. I have provided a tool that has saved many people from both passing on deals they should take as well as taking deals they should pass.

I took from my own trials and errors & created a checklist – The Real Estate Investing “Before You Commit” Due Diligence Checklist. Keep in mind every one of mine or your personal due diligence items on that “checklist” do not need to be followed on every deal you consider. However, it’s a great list to follow and assure you have remembered to consider all that can affect the outcome of your purchase. Your due diligence makes all the difference on whether your purchase of property brings you a profit or a loss.

Rule #3 – Invest Using the Strategies that Make Sense and the Location That Makes Sense for the Current Market Conditions

I always say invest where it makes sense and dollars. You don’t need to invest in your home town, because you live there…nor do you need to go all over the country investing everywhere else. Do your homework and invest in locations that align with the real estate investing niche you chose using the strategy that is a fit.

For example, three years ago I was investing nationally in pre-construction in most strong appreciating markets. That strategy made sense at the time. It would not make sense in a depreciating market.

Today I live in a town that has been on the top 5 most foreclosures list for over 2 years. Why would I need to invest nationally when there are more than enough leads right in my own backyard? Where to invest varies depending on the location of the investment as well as market timing.

My investment choices change as often as the market does. Being sensitive and aware of changing market trends is helpful to know where to invest and the most profitable strategy to follow. The last four rules of the “Top 7 Tips To Minimize Your Risk & Maximize Your Profits” will be concluded in Part 2.

Tamera Aragon

Tamera Aragon is a professional online entrepreneur and has bought and sold over 300 properties, establishing her as an expert in the real estate investing field. Since 2003, she has purchased over 10 million dollars in real estate and currently holds properties all over the world. Tamera’s focus is on the booming Foreclosure market, buying Pre-foreclosures, REOs and Short Sales. Tamera who is a noted Author, Success Trainer, Speaker & Coach, shows her passion for helping others with the 17 websites she has created and several specialized products to support fellow investors throughout the world. When Tamara is not busy running her website, she is very involved with her Fiji joint ventures and investments. Tamera Aragon is one of the few trainers and coaches who is really “doing it” successfully in today’s market. Tamera’s experience has earned her a solid reputation in the industry as well as the respect and friendship of many of the top national real estate investment and internet marketing experts. Tamera Aragon believes her success has garnered her the financial freedom to fully enjoy her marriage and spend quality time with her children.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/04/profit.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-04-16 05:07:072024-04-16 05:07:09Tips To Minimize Your Risk & Maximize Your Profits (Part 1)

Realty411.com has assisted companies of all sizes expand their visibility and grow their business since 2007. Contact us for a complimentary marketing session: CLICK HERE.

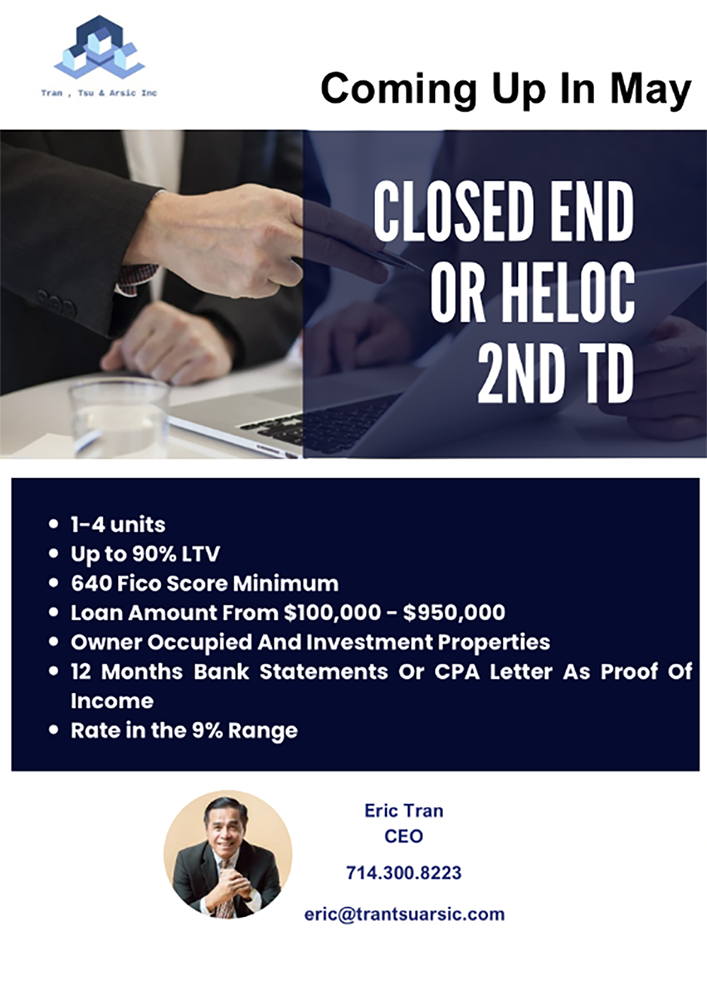

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/04/TD.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-04-10 02:26:282024-04-11 00:15:07Learn About Our 2nd TD Option