ORLANDO, FL – New Home National Title, a forward-thinking company transforming the real estate industry with cutting-edge technology and services, is excited to announce its upcoming feature on the Boom America TV show hosted by the iconic Kevin Harrington. Boom America is a distinguished platform that spotlights groundbreaking companies and their influential innovations. The feature of New Home National Title emphasizes its game-changing approach to real estate transactions, particularly its emphasis on mobile earnest money delivery and cryptocurrency payments.

article continues after advertisement

New Home National Title is spearheading advancements in the real estate sector by providing seamless and faster closing processes through its state-of-the-art technology. This includes unique features like mobile earnest money delivery and the acceptance of cryptocurrency payments, offering unparalleled convenience in home purchases. The company’s robust suite of title and escrow services cater to both residential and commercial sectors, making them a trusted ally for leading real estate and banking institutions nationwide.

“Being showcased on Boom America is a significant achievement,” said Richard Simon, owner & founder of New Home National Title. “We’re eager to introduce our modern and innovative approach to real estate transactions to a wider audience, inspiring more individuals and businesses to experience the unmatched efficiency and dedication we bring to each deal. Through our feature on Boom America, we aim to highlight how New Home National Title is setting new standards in the real estate sector.”

The feature of New Home National Title on Boom America reinforces its leadership position in the real estate industry. With its commitment to innovation, personalized user-friendly service, and a seasoned team of real property experts, New Home National Title is redefining the experience of real estate transactions. Their mission of infusing a personalized touch into every deal, regardless of its scale, underscores their customer-centric philosophy.

New Home National Title is disrupting the real estate market by using the most advanced and secure technology to streamline the closing process, including mobile earnest money delivery and crypto currency payments, making home purchases faster and more efficient than ever. New Home National Title offers a full slate of title and escrow services for both residential and commercial markets and is a trusted partner to the top real estate and banking organizations throughout the country.

Boom America is a life-changing show hosted by none other than the legendary Kevin Harrington. A pioneer of the infomercial industry and an original star of the hit TV series Shark Tank, Kevin leads a powerhouse team of business experts on a mission to take various innovative companies to new heights. The real work begins as the chosen companies embark on a journey of explosive growth, guided every step of the way by the seasoned professionals of Kevin’s team. Get ready for a game-changing ride in 2023!

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/09/New-Home-National-Title.jpg5001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-09-08 04:35:292023-09-08 04:35:34Boom America TV Show Highlights New Home National Title: Revolutionizing Real Estate Transactions

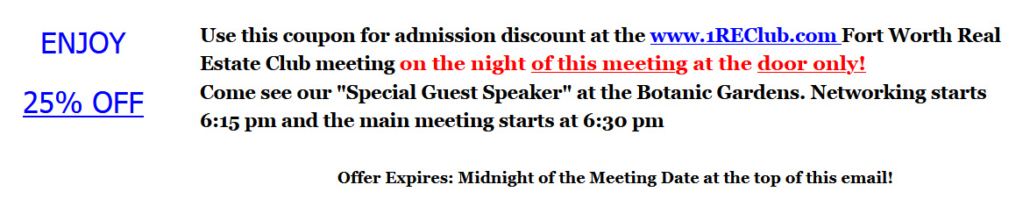

Come Network Thursday September14, 2023 6:15 PM at the Fort Worth Real Estate Club with us and our Guest Speaker. Linda Pliagas

Real Estate Generational Wealth!

And the Realty 411 Expo on Sept 16th in Arlington, TX.

LINDA PLIAGAS, CEO, REALTY411 .COM

Linda Pliagas is the CEO and publisher of Realty411, which she founded in 2007. Linda has personally owned and managed rental properties in five states, all by the age of thirty-eight. Linda and her husband have purchased single family homes, multifamily units, vacation rentals, probates, REOs, and short sales. She has worked simultaneously in media and real estate for decades.

She holds a bachelor’s degree in print journalism from California State University, Long Beach. She was a recipient of the Bobit Magazine Scholarship for her accomplishment in publishing her first national magazine while still at CSULB. She also studied real estate, accounting, and general studies at Santa Monica College. As a journalist, Linda has freelanced for numerous national magazines, local newspapers, and global websites. Her mission is to empower average Americans to build generational wealth for their families by investing in real estate. Her website is Realty411.com.

Some of the things Linda will be Talking on at this Event:

We will be doing this Meeting Interview Style!

The Interviews have been such a Favorite of Attendees we are doing it again.

We will have Questions about Generational Wealth via Real Estate

What to Expect at the Expo 2 Days after this meeting.

How to Get Started investing on the Fast Track!

How to get the Most out of the Expo & the Power of Networking at the Expo.

The 411 & REI Magazines that can help you succeed with a Coast to Coast Network.

Marketing in those Magazines for Success!

And so Much More!

Bring your Questions you need Answers to!

Be Prepared to take a lot of Notes!

If you are not a Member read below on how to become one, and then watch the meeting any time along with other meetings since April of 2020.

There are only 2 ways for you to hear this information packed segment.

Becoming an Annual Member to watch it online from the comfort of your Home OR

Coming out to our in Person Meeting at the Botanic Gardens!

YES WE ARE BACK!!! LIVE COME OUT & NETWORK!!!

New Schedule!!! Doors open at 6:15pm Main Meeting Starts a 6:30 Sharp and ends at 8:30, Then More Networking after the Meeting!

For the Fort Worth / DFW Area Real Estate Investors Club’s Monthly meeting at the Fort Worth Botanic Gardens.

Networking with local investors starts at 6:15 pm and the Main meeting starts at 6:30 pm. Come out and meet our Preferred Vendors and let them answer any questions you have about real estate investing.

*So come out and bring plenty of business cards, flyers, anything you need to network! Also if you have properties for sale then make sure to print up some info sheets on them and put them on our “Deal Table” each month along with your Networking Materials!

NOW!! just $20 to attend & Memberships are available at a discount! The club is all about providing value, which is why we bring in vendors and speakers who are here to make your life as an investor easier and more lucrative.

If you are Serious about Real Estate Investing then you need to attend this Real Estate meeting at the Botanic Gardens.

See Ya There! Jimmy Reed

Proverbs 13:20 Walk with the wise and become wise, for a companion of fools suffers harm

Also check out our Facebook page for the club. Click Link Below to see it!

You can watch some videos from past meetings. Also see some pictures of all the things we do at the club!

Annual Membership now gives you 1 year admission to the club along with 1 year access via our Private Facebook Group. So if you ever cant make a meeting you can watch it online Live, or the next day!

Just Click Either Button for Single or Double Membership! CHECK OUT THE NEW 2022 SPECIAL PRICES!

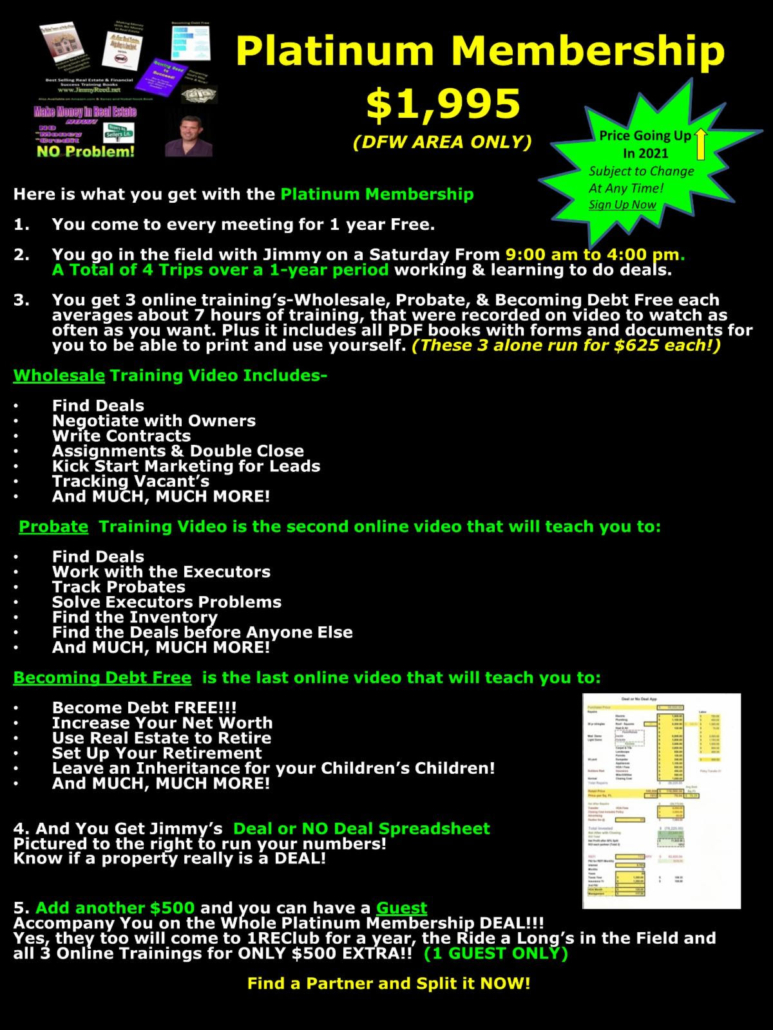

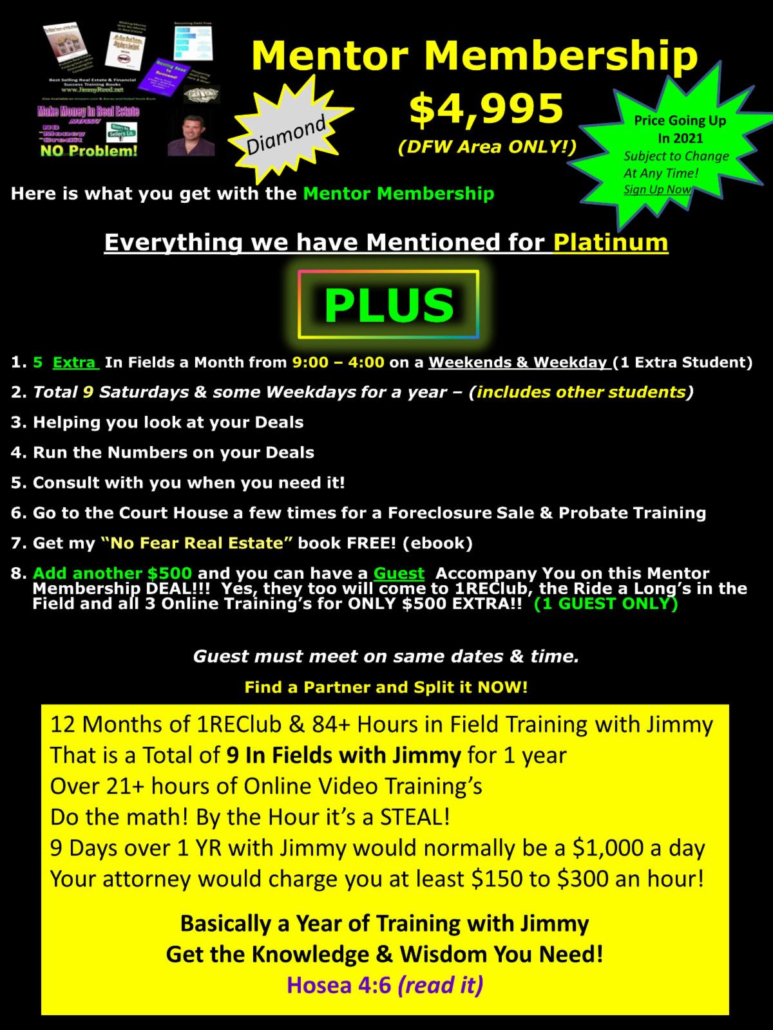

Other Memberships that Include Infield Training’s with Jimmy! Click on the Brochure for More Info.

Platinum Membership

Mentor “Diamond” Membership

For “Platinum” & Mentor “Diamond” Memberships Click Below to Start Training Now!

Check out these Videos on the Real Estate Club & Training’s we have available to help you get started Today!

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/09/Linda-featured.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-09-07 08:23:052023-09-07 09:08:35Founder of Realty 411 & REI Wealth Linda Pliagas & The Texas EXPO!

Please review this important message from our sponsor, thank you.

In today’s fast-paced world, we all understand the value of hard work. But how about working smarter instead of harder? What if you could let your money do the hard work for you?

This is the fundamental idea behind passive income, and it’s one of the key reasons why real estate syndication is such a powerful wealth-building tool.

Here’s how it works:

1. Consistent Cash Flow: When you invest in real estate syndication, you’re purchasing a share of a rental property. This property generates rental income, which is distributed among investors – like yourself – providing a consistent stream of cash flow.

2. Minimal Time and Effort: With syndication, you don’t have to worry about the day-to-day management of the property. That’s handled by us, the syndicators. You can sit back and enjoy the returns without the hassle of being a landlord.

3. Wealth Accumulation Over Time: As your passive income streams contribute to your wealth, you have the opportunity to reinvest that income, effectively putting your money to work to generate even more income.

4. Financial Freedom: Passive income can provide financial security and freedom. With a steady income flow independent of your regular job, you could potentially retire earlier or have the financial cushion to pursue what you love.

At Apex Real Estate Investments, we specialize in creating opportunities for investors to generate passive income through real estate syndication.

Our aim is to help you put your money to work, so you don’t have to work as hard. Ultimately this serves to free up your time — the most valuable asset of all.

In upcoming emails, we will explore more about how to create passive income and the role of real estate syndication in this process. Stay tuned!

As always, if you have any questions or need further information, don’t hesitate to get in touch.

Best Regards,

Joseph Kimbrough 469-458-9295 CEO & Founder Apex Real Estate Investments

Learn from Joseph Kimbrough at the Lone Star Investor Wealth Summit, RSVP NOW

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/09/money-rain.jpg5001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-09-07 05:21:022023-09-07 05:21:07Let Your Money Do the Hard Work for You

Whether you are an experienced Real Estate Investor (REIer) or are a newbie in this industry, there exist many innovative funding techniques you can use to finance current and future deals. Generally referred to as creative financing, these terms refer to alternative or unconventional approaches that REIers may choose to utilize to acquire investment properties, using OPM: Other People’s Money.

In today’s unpredictable real estate investor landscape, it is very important to have a range of funding options at the ready before you dive into a property investment deal. Let’s face it, to be a successful REIer takes money. It does not necessarily have to be YOUR money, but before you can successfully pull off a deal, chances are SOMEONE’s funds are going to have to be brought to the table. Plan ahead. Line up funds before you need them because they have to come from somewhere.

article continues after advertisement

Make sure, before you commit to any real estate deal, that you have all your web-footed waterfowl neatly arranged in a linear fashion.

A. Lease Option: You may encounter a situation where you are not ready yet (either experience- or financial-wise) to purchase a property, either for your own personal use or as an investor. That is where the lease option can work best. Doing so provides the opportunity to purchase a property at the conclusion of a pre-arranged leasing-type agreement. This approach allows you to potentially build up equity through monthly rent payments.

The landlord benefits by earning monthly revenue. Typically, and depending on specific contract terms, a portion of the monthly rent payment is credited toward the future down payment on the house. This technique normally works best in a buyer’s market.

B. Down Payment Assistance (DPA). Many REIers are finding themselves caught in a new type of financial squeeze when it comes to the percentage of the purchase price that hard money and private lenders require that they bring to closing, i.e. “Skin-In-The-Game” (SITG) cash.

Until recently, it was possible to secure, say a 90% loan from such lenders, with the borrower required to contribute the other 10% as their SITG capital. And while those terms are still available in some cases, many REIers are waking up to a new reality: They need to bring closer to 20%-30% SITG cash to closing in terms of actual down payment money, with a general average of around 25% DP money currently required.

Upping the SITG percentage is a risk-reduction strategy employed by lenders in response to what they perceive as new uncertainties in the real estate investment marketplace, on a go-forward basis. The reality for REIers caught in this new “liquidity squeeze” is that they now may need to potentially come up with tens of thousands or even hundreds of thousands in new (SITG) investment capital above what was previously required.

Without new SITG capital, the REIer cannot close on the deal. A potential solution to this new dilemma is what we refer to as “Down Payment Assistance (equity) funding”: This is where a third party provides the needed extra SITG/DP cash in return for a modest share of the profits. See below for info about DPA.

C. Seller carryback loan. Plainly speaking, this is simply owner-provided financing. The seller acts as the lender or bank, i.e. he carries a mortgage–usually a second position loan–on the property and collects monthly payments from the buyer. Such an arrangement can be a win-win for both the buyer and the seller. Often the buyer (an REIer in this case) may be willing to pay more than the asking price in trade for advantageous loan terms on a seller carryback mortgage.

Further, the buyer is often willing to pay a higher interest rate on the seller carryback loan than the seller could earn from a CD from their local bank. Also, should the buyer default, the (previous) seller can always initiate foreclosure action and take the house back from the second position. The buyer benefits since they don’t have to go through the arduous and time-consuming chore of trying to get a bank loan; this is especially true if the buyer has a low FICO score or other credit or background issues.

article continues after advertisement

D. Buying a property “Subject-To”. What this means is that the REIer essentially takes over the seller’s remaining mortgage balance (thereby effectively “assuming the loan”) without making it official with the lender. This is a popular strategy among REIers, especially in an era of rising interest rates, since the loan being assumed probably carries a lower interest rate compared to a new (bank) loan.

Savvy REIers often employ the Subject-To method to take the place of a hard money loan. However, most REIers limit the use of Subject-To loans to relatively short-term time frames, i.e. for a few months until the REIer can either refi the loan or sell the property as part of a fix-flip strategy.

E. Hard Money: A hard money loan refers to asset-based financing where the borrower receives funds that are secured by real property. In most cases, private investors are the biggest suppliers of hard money capital, which are then funneled through hard money brokers.

While the terms (interest rate, points, time frames) of hard money loans may vary, there are several common characteristics: they are usually easier to obtain vs. a conventional bank loan; credit scores and income verification are not as important as the asset value involved; they are usually for shorter time frames (say for 6-24 months); while they charge higher interest rates, the good news is that they often can fund pretty quickly if the deal is right. They usually focus on the ARV (After Repair Value) to determine the loan terms, including important factors such as the rehab blueprints, scope of work, etc. They usually prefer to work with experienced rehabbers who have a clear plan to repay the loan within the specified time frame.

F. Cross collateral loan. This REI method assumes you already own a rental property free and clear. You want to buy another rental property. A cross collateral loan allows you to use the 100% equity in the existing property as leverage to acquire the new property you want to purchase. With cross-collateralization, the lender places a lien on both the new property and your existing property. In this way, the lender receives adequate security should you default on the loan. Basically, cross-collateralization allows you to sidestep the normal down payment requirement and/or having to take out a brand new (bank) loan.

G. Retirement accounts: Use your self-directed IRA, Roth IRA, 401-K, corporate plans as investment capital, where it is legal, prudent and appropriate to do so. Utilizing a self-directed retirement plan can empower a REIer by boosting their retirement savings, one deal at a time. Since we are talking about your retirement money, an extra degree of caution is called for. You need to possess excellent due diligence and underwriting skills in order to properly assess the potential risks involved.

H. Cash-Out Refinance. If your personal residence has a good amount of equity in it, you can unlock that equity via a cash-out refinance by tapping some of that equity. Make sure you fully understand the implications of such a loan should things not go well with your anticipated new investment. A cash-out refi may feature (more) favorable interest rates compared to a hard money loan. Also, the interest you pay is tax deductible. You need to do a risk/benefit analysis before going down this road. Regardless, if a REI deal looks very promising, and you require fast capital to make it happen, a cash-out finance can be a good way to go.

I. 203-K Loan: This unique FHA mortgage enables you to finance both the purchase (or refinancing) of a house and the cost of its rehabilitation through a single mortgage or to finance the rehabilitation of their existing home.

1. Pros:

a. Lower credit score allowed b. Smaller down payment requirements (as low as 3.5%) c. Can provide temporary housing while a home is being repaired d. Lower potential interest rates, compared to similar loan types e. Ability to combine home purchase and renovations into a single loan

f. Low down payment and credit score requirements

2. Cons:

a. FHA mortgage insurance required b. FHA loan rates may be higher compared to conventional loans c. Process may require meeting with a 203(k) repair consultant d. More extensive repairs require more paperwork e. Potential for the additional cost of architectural assessments f. Property must be your primary residence g. You must live in the home for 12 months before selling or renting it out

J. More creative financing methods to consider include:

1. Approach friends, relatives, etc. Options can include debt or equity.

2. Equity investors. The advantage here is that you do not have to make monthly payments because there is no loan. When the deal is done, some sort of profit split is made to compensate the investor(s).

3. Credit card advances. This can be an expensive gambit. It is only to be undertaken when you are very sure of positive, short-term outcomes. The bank may charge several points and up to 29% interest rates, so be very careful with this one.

4. Joint venture: you bring the deal, they bring the money, split the profits at the end. This is a variation on an equity-type investment.

5. Hypothecate (borrow against) a mortgage note you own. Basically, you take out a loan by pledging the note, thereby using it as collateral to secure the loan.

6. Personal asset loans: pawn some jewelry; get a car title loan, etc.

Down Payment Assistance Funding Program

Are you a Real Estate Investor Pro (REI Pro) who has a property you want to buy, with a 70% LTV or better, but you lack some of the Down Payment (DP) money needed to close the deal? You need say, 25% DP, but can only come up with 10% and need 15% more (DP money.

The good news is if your deal meets our standard criteria (70% LTV or better = 30% or more equity in the deal, etc.), CTF can provide the missing 15% in DP funding. By not having to put out all your own capital into DPs–especially if you are low on cash–you’ll be able to do more deals. With your DP source already in place, it will shorten your time for getting positive confirmation from your primary lender, and for getting more deals successfully closed.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

Are you tired of playing it safe with your investments? Want to spice things up and take on a potentially lucrative option? Real estate syndication may be just what you’re looking for, and as a limited partner (LP), you can reap some benefits.

In this article, we’re going to explore the world of real estate syndication and why being an LP can be a fun and rewarding way to invest in real estate. From higher returns to less hassle, being an LP has some unique advantages worth considering. So put on your investor hat, and let’s dive in!

article continues after advertisement

1. Limited Liability

A key benefit is the limited liability protection from investing as an LP in a real estate syndication. It protects the investor from personal liability if the investment fails or incurs liabilities. So, for example, if a tenant slips and falls on a property owned by the syndication, the LP investor’s personal assets will not be at risk. Instead, the GP will be responsible for any losses or liabilities incurred by the partnership.

A National Bureau of Economic Research study states limited liability protection is critical in encouraging entrepreneurship and investments. The study found that limited liability is associated with a higher likelihood of investments and a more significant number of firms being created.

2. Passive Investments

Investing as an LP in a real estate syndication is a passive activity, meaning that the investor does not have to be actively involved in the day-to-day management of the real estate assets. Instead, the GP is responsible for managing the assets, and the LP investor receives a share of the proceeds based on the percentage of their investments.

According to a National Multifamily Housing Council report, passive investing in real estate is becoming increasingly popular, with many investors seeking to diversify their portfolios beyond traditional assets such as stocks and bonds. In addition, the report found that passive investing in real estate syndications can provide a steady stream of wealth and long-term capital appreciation.

3. Connect to Larger and Diversified Investments

Investing in a real estate syndication as an LP provides investors a connection to more extensive and diversified real estate projects that they may have yet to be able to approach on their own. The GP is responsible for identifying, acquiring, and managing the real estate assets, while the LP investor provides the funds.

According to a report by the Urban Land Institute, investing in real estate syndications provides a door to a wide range of real estate assets, including commercial properties, multifamily buildings, industrial properties, and more. In addition, the report found that investing in real estate syndications can provide diversification benefits to investors by allowing them to invest in various assets with different risk and return profiles.

article continues after advertisement

4. Potential for Higher Returns

Investing as an LP in a real estate syndication can provide higher returns than traditional investment vehicles, such as stocks, bonds, and mutual funds. The potential for higher returns is due to the GP’s ability to manage the real estate assets and maximize the return on investments.

According to a National Council of Real Estate Investments Fiduciaries report, real estate investments have historically provided higher returns than other traditional investment vehicles. For example, the report found that from 1999 to 2019, the total annualized return for real estate investments was 9.5 %, compared to 6.2 % for stocks and 5.3 % for bonds.

5. Tax Benefits

Investing as an LP in a real estate syndication can provide various tax benefits, including depreciation deductions, passive activity loss deductions, and capital gains tax deferral. These tax benefits can reduce the investor’s tax liability and increase their after-tax return on investments.

According to a report by PwC, real estate investments can provide various tax benefits to investors. For example, depreciation deductions can offset taxable wealth, and passive activity losses can be deducted against other passive wealth sources. Additionally, a 1031 exchange can defer capital gains taxes by reinvesting the proceeds from selling real estate assets in other qualifying real estate investments.

Investing as an LP in a real estate syndication can also provide specific advantages for busy professionals who may not have the time or expertise to manage real estate investments actively. Some additional advantages include the following:

6. Time Savings

Investing in real estate syndications as an LP can be a time-efficient investments strategy for busy professionals. The GP is responsible for identifying, acquiring, and managing the real estate assets, while the LP investor provides the funds. This allows LP investors to focus on their careers and other activities while still earning a return on their investments.

7. Expert Management

Real estate syndication allows LP investors to benefit from the expertise of the GP in managing real estate assets. The GP typically has experience and knowledge in real estate investments and can use this expertise to maximize the return on investments for the LP investors. This can be especially beneficial for busy professionals who may not have the time or expertise to manage real estate investments actively.

8. Limited Involvement

Investing in real estate syndications as an LP can provide limited involvement for busy professionals. The LP investor does not have to be actively involved in the day-to-day management of the real estate assets, allowing them to focus on their career and other activities. The GP is responsible for managing the assets, and the LP investor receives a share of the returns based on the percentage of their investments.

9. Diversification

Investing in real estate syndications as an LP can provide diversification benefits for busy professionals. The GP is responsible for identifying, acquiring, and managing various real estate assets, allowing the LP investor to invest in a diversified portfolio of assets. This can reduce investment risk and provide a more stable return on investments.

10. An Entry to Exclusive Deals

Real estate syndication can provide LP investors with a way to exclusive real estate deals that may not be available to the general public. In addition, the GP typically has a network of contacts in the real estate industry and can use this network to identify and acquire exclusive real estate assets. This can provide LP investors with unique creation wealth opportunities and higher returns.

Overall, investing as an LP in a real estate syndication can be a time-efficient, low-involvement, and diversification investments strategy for busy professionals. In addition, the expertise of the GP in managing real estate assets can help maximize the return on investments for the LP investors. At the same time, limited liability protection can provide additional security for their assets.

At Blueocean Capital, we offer a unique opportunity for investors to become limited partners (LPs) in our real estate syndication projects. As an LP, you get to enjoy the benefits of investing in larger real estate projects without having to worry about the details of managing the property. You can trust that our experienced team of professionals will handle all the work while you sit back and collect passive income from your investment. Plus, by investing with us, you can benefit from potentially higher returns compared to traditional real estate investments.

So why not consider becoming an LP with Blueocean Capital? It’s a great way to diversify your portfolio, earn passive income, and potentially achieve long-term financial goals. Join us today and let us show you how being an LP can be a rewarding investment opportunity!

You can also schedule a with us to learn more about our investment opportunities and how you can become a Limited Partner. Our team will be happy to answer any questions you have and guide you through the process.

Let’s start building your investment portfolio together!

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/09/Bigger-Better-Hassle-Free.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-09-05 05:23:092023-09-05 05:23:13Why Limited Partners Love Real Estate Syndication

We are very excited to announce our 4th Annual Los Angeles Real Estate Grand Expo. The Grand Expo returns on Saturday, October 21, 2023, 9:00 am to 6:00 pm. We’re taking over the entire Iman Cultural Center for the day – it’s all ours!

The North Hall (vendor exhibition area), the South Hall (workshops), and the middle parking lot (loaded with workshop tents and food trucks). The theme of this year’s Grand Expo will be “Hedge Inflation – Buy Real Estate”.

Last year, the Grand Expo was the largest real estate event in Southern California. We had over 800 investors, 64 vendors, and 12 national speakers…this year will be even BIGGER! An entire day celebrating real estate investing and you can be involved. Best of all, the Grand Expo will be FREE to attend.

This Expo is going to be big, really BIG! We are hosting investors from around the nation once again.

EDUCATORS. There will be national guest speakers (in three breakout rooms). Here is a partial list of our top educators:

1. Jonah Dew – “The Money Multiplier” 2. Eddie Speed – “Buying Discounted notes” 3. Rusty Tweed – “1031 Tax-Deferred Exchanges” 4. Joe Arias – “How to Get Started Investing” 5. Christopher Meza – “Developing Raw Land” 6. Tony Watson – “Tax Advantages for R.E. Investors” 7. Dani & Flip Robison – “Fixing & Flipping Houses” 8. Abbas Mohammed – “Investing in Multi-Residential Properties” 9. Marco Kozlowski – “How to Buy Lots and Lots of Houses” 10. Amanda Brown – “Invest in Commercial Real Estate” 11. Shawn Tiberio – “Marketing for Real Estate Investors” 12. Joeseph Scorese – “How to Finance Your Next Deal” 13. Jeremy Rubin – “From Employee to $100M in Flips” 14. Steve Price (Keynote) – Vice President at Auction.com

INVESTMENT EDUCATION. An all-day in-depth educational extravaganza celebrating real estate investing. Most importantly, this will NOT be a sales pitch. So regardless of whether you are a new investor, already own properties, or are very experienced, our Grand Expo is for you!

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/09/Grand-Expo-speakers.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-09-04 03:53:172024-04-17 02:50:46Join Us for Education, Motivation and Collaborate – RSVP Now!

NEW YORK, NY — B+E, the first brokerage and technology platform for net lease real estate, today announced the addition of Max Sabino as an Associate Director in the New York B+E office.

Max Sabino

“We are excited to welcome Max to the B+E team,” said B+E CEO Camille Renshaw. “He is a results-driven sales professional with a proven track record in net lease sales and is skilled in conducting market research, analyzing client requirements, and tailoring solutions to meet their needs.”

article continues after advertisement

Max focuses on the execution of sale-leaseback programs and asset disposition/acquisition programs for private family offices, franchisors, franchisees, developers, and other large institutions.

Most recently with SRS Real Estate Partners, Max was a part of the division’s most successful net lease team, based in Newport Beach, CA. During his time there, he gained deep net lease knowledge, including understanding inherent real estate value, market conditions, tenant/credit underwriting, site-level performance metrics, and lease economics. Max Sabino

article continues after advertisement

Prior to SRS Real Estate Partners, he was a broker at Aspect Real Estate Partners. While there, he was the top individual contributor and made partner with the three Max Sabinofounding principals.

About B+E

B+E is a modern investment brokerage firm, specializing in net lease real estate. The firm helps clients buy and sell single tenant real estate. Founded by deeply experienced brokers, B+E redefines trading through an intuitive end-to-end transaction platform consisting of user-friendly dashboards and an AI-driven exchange — all leveraging the largest data set in the net lease industry. With offices in New York, Chicago, Atlanta, Tampa, Charlotte, Dallas, Orange County, and San Francisco, its brokers trade property for clients across the US.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/shake-hands.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-31 02:53:592023-08-31 02:54:03Max Sabino Joins B+E’s New York Office as Associate Director

Join Us for 1 Special Day and Learn How to Grow Wealth with Real Estate – Our Network Owns Properties Across the Nation!

Date and time: Saturday, November 11 · 9am – 5pm EST Location: Estonian House 243 East 34th Street New York, NY 10016 United States

article continues after advertisement

Learn Real Estate Investing with Realty411 – Join Us for Our In-Person Event in New York City!

Investors, take a moment and grasp this opportunity — the chance to network with sophisticated real estate investors joining us from throughout Texas — as well as from around the nation!

This summit will help you gain specialized insight and knowledge about real estate investing, entrepreneurship, finance and other life-changing insight. The information shared on this day could catapult your real estate portfolio to new levels.

This one-day conference has something for everyone regardless of their experience level in real estate. Join us for this memorable day and receive knowledge for a lifetime.

Learn the Latest Niches in Real Estate + Connect with Influential Investors from across the nation in Manhattan. We expect guests from around the nation to join us.

Registration begins at 8:30 am. The education begins promptly at 9 am.

Are you ready to Grow Your Real Estate Business, Portfolio and Network?

This is Your Chance to meet TOP Leaders in REI, Local & National Experts.

Learn from Leaders & Industry Pros

Meet Local PLUS Out-of-Area Investors

NON-Stop Tips for Real Estate Success

Bring Lots of Business Cards

This special and life-changing Real Estate Summit is produced and hosted by Realty411.com. Since 2007, we have dedicated our time, resources and energy to help expand real estate investing knowledge and education by producing complimentary magazines, virtual conferences, webinars, podcasts, and live events. We have reached thousands of real estate investors across the nation in person.

We also produce REI Wealth magazine, which is the longest-running magazine for investors specifically developed for online readership. Our digital, interactive issue is designed to be read and viewed online. We now also print copies of this fabulous publication as well. Download our latest issue, CLICK HERE.

INVEST YOUR TIME HERE FOR ONE SPECIAL DAY OF NETWORKING & MOTIVATION – TAKE YOUR REAL ESTATE KNOWLEDGE TO A WHOLE NEW LEVEL.

article continues after advertisement

Learn with PROVEN Leaders in the Industry:

Receive the latest REI knowledge from active investors

We feature the latest technology to expand your income

Meet other investors with common goals and mindsets

Develop relationships with leaders in the industry

Share your opportunities with potential clients

Learn how to save money with our Realty411VIP.com members’ network

Realty411’s publisher has owned national rentals for many decades

We will share life-changing information unavailable anywhere else

We host real estate events to meet our readers and to spread industry updates

Our mission is simple: To provide realty knowledge and resources so that everyone can learn about the benefits of investing. We hope you to see you in person soon. Please register today to receive information about our speakers, sponsors and special updates.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/Manhattan.png4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-30 04:27:002024-04-17 02:50:51Realty411’s Investor Summit in New York City – Mingle in Manhattan

Don’t miss the opportunity to connect in Philadelphia, Pennsylvania once again for an educational boot camp. At this event, guests will have the opportunity to learn directly with top business and real estate leaders. Experienced educators will share their knowledge and strategies for guests to have a better understanding of the current real estate market. Join us and gain the insight to implement a game plan for success. This boot camp will include top-level industry information and fantastic networking.

Date: October 7th, 2023 Time: 10am-3pm Location: Philadelphia School of Massage & Bodywork, 263 N Lawrence St, Philadelphia, PA 19106 Mindset: ‘Education, Networking & Creating Opportunities a Workshop Setting’ Registration Cost: $99.00 Person – Includes Breakfast, Snacks & Lunch

Mike Lautensack

Owner at Del Val Property Management LLC

TOPIC: The 10 Reasons Why Real Estate Investors Should BRRRR with Professional Property Management for Maximum Wealth

Stephen Chatto & Roland Jefferson

TOPIC: Wholesaling Real Estate as the foundation to success in all areas of real estate investing.

Overview: A dive into the nuts and bolts of what real estate wholesaling is and is not. This presentation will be real, diving into what is involved, good and bad, in running a successful wholesale business from two full-time real estate investors with hundreds of transactions closed. Not only will you understand and learn the real ins and outs of real estate wholesaling, but you will also learn how the lessons learned operating a wholesaling business translate into effectively running real estate businesses across many niches.

Bob Chessick

Chesspin Corporation

TOPIC:Business Strategy Without The B.S.

Incorporating for Real Estate 101 with Bob Chessick

? The Corporate Transparency Act is coming, and it impacts your LLC – Is your LLC ready for 2022?

? Topics will include:

✔ Types of companies

✔ Tax implications

✔ Use of multi-company structures

✔ The new Corporate Transparency Act

article continues after advertisement

Eric Mauz

Owner, MB Capital Solutions

TOPIC: Expand Your Real Estate Business with Unsecured Business Lines of Credit

3 types of Unsecured Business Lines of Credit

Credit Guidelines to Qualify

R.E. Investor Client Case Study – How clients have used their credit lines for BRRRR Method and Fix & Flip Project

Joseph V. Scorese

National Sales Director, BRRRR Loans

TOPIC: Leveraging Direct Private Lending

Leveraging Direct Private Lending can be a great way to create passive income from real estate and understand Lending Options owning rental properties. But there is a lot to learn before diving in! This Presentation has everything you need to know to provide better knowledge to Real Estate Professionals, Agents & Services in the Investment Space on Direct Private Lending!

article continues after advertisement

We will cover:

• Rentals Loans

• Fix & Flip Loans

• Portfolio Rental Loans

• Multi-Family Bridge Loans

• New Construction Loans

• Fix to Rent Loans

• Blanket Loan Programs

• 5+ Multi Family & Mixed-Use

• DSCR & Bank Statement Loans

• Non-Recourse & Recourse Options

• Unsecured Business Lines of Credit

• Foreign National Loans

YOUR HOST: This educational boot camp is hosted by Joseph V. Scorese. Mr. Scorese is a mortgage industry professional who is committed to helping his clients. He has more than 20+ years of successful experience in loan origination. Joseph continues to work in the mortgage lending industry and has built a career as a talented and reliable Mortgage Banker.

Real estate lending encompasses both real estate and securities laws.

A) Deeds of trust and mortgage instruments are securities:

Promissory notes secured by deeds of trust or mortgages are security instruments. These contracts represent evidence of indebtedness. Ownership is a security under the Federal Securities Act of 1933.

The definition of security under federal law is as follows:

a) Property given or pledged to guarantee the performance of an obligation. b) An instrument that functions as proof of a security interest in a public or private body.

article continues after advertisement

Parties in a loan transaction:

Borrowers and private-party lenders are the principals in a transaction. A borrower will sign a promise to pay called a promissory note and the security instrument called a deed of trust. The deed of trust is an instrument recorded at the county recorder’s office, which becomes a matter of public notice of the charging lien against the property.

The note and deed of trust are contracts between the borrower and private-party lenders. After the loan closing, the investors/lenders, or the servicing agents of the investors, will retain the executed and recorded documents as evidence of the investment.

Promissory notes and deeds of trust (or mortgages) are considered personal rather than real property.

B) Deeds of trust and mortgage investments are securities requiring federal or state registrations unless there are applicable exemptions from registration.

Each state in the U.S. has its own securities laws and regulations. State statutes, known as Blue Sky laws, are designed to establish safeguards against fraud for investors. Each state passed separate securities laws to protect the public from fraudulent schemes as far back as 1911 in Kansas. The term “blue sky law” originated in the early 1900s, gaining widespread use when a Kansas Supreme Court justice declared his desire to protect investors from speculative ventures that had “no more basis than so many feet of ‘blue sky.’”

What does securities registration mean?

Registration occurs when a company files the required documents with the Securities and Exchange Commission (SEC). The extensive process involves approving disclosures and other information related to the offering. There will usually be quarterly and annual reporting requirements.

Unregistered securities have fewer protections than registered securities. Companies can only sell unregistered shares to a limited number of qualified or high-income and high-net-worth investors.

Securities overview:

Federal and state securities exemptions from registration are common and available.

Federal Exemptions:

Federal exemptions for privately funded loan transactions and loan pooled investors are referenced in Regulation D, Rule 506 section 4(a)(2), and 506(b), Regulation A, and Rules 147 and 147A. Information about these regulations can be found at:

Definitions and exemptions are on the www.sec.gov website.

article continues after advertisement

State securities exemptions:

Each state has its own securities laws and exemptions.

I am using California as an example because that is my state of origin. However, those involved with loans and investors in other states should identify their dominion’s relevant state securities statutes.

California Corporate Codes relating to securities are 25000-31516

California Corporate Securities Law of 1968 regulates all offerings and sales of securities in California. All securities offered or sold must be qualified by the Department of Financial Protection and Innovation Commissioner or exempted from qualification and registration by a specific law or corporate rule. Securities references include 10CCR, Chapter 3, Sections 260.115 and 260.204.1, California Corporate Securities rules 25206, 25100 (p), 25102, (e) (f) (n), and 25102.5 which refers to the multi-lender rules.

a) 25100 (p), is referred to as a whole note exemption, one note purchased by one party

(p) This is a promissory note secured by a lien on real property which is neither a series of notes of equal priority secured by interests in the same real property nor a note in which beneficial interests are sold to more than one person or entity.

b) 25102 for state offerings exemption

c) 25102 (e)

Under Section 25102 (e, f,), an exemption from the qualification requirement for issuer transactions is available for any offer of sale of evidence of indebtedness, a partnership, a joint venture, and certain participating interest in railroad rolling stock, or other equipment, if the transaction does not involve a public offering.

California state exemptions for fractional trust deeds are 25102(e), 25102(f), and 25102.5, which cover multiple investors who invest in real estate loan transactions. 25102(e) and 25102.5 allow a maximum of 10 investors. Both exemptions, 25102 (e) and 25102.5 contemplate lending on California properties with California-based investors. Family members are considered as one in the same household.

d) 25102.5is referred to as the fractional note exemption.

California rules are promulgated in the Business & Professions Code 10237-10238, 10232.3, 10232.4, 10232.5, Civil Code 2941.9, and many others.

Under the 25102 (e) and 25102.5 exemptions, ten private investors can co-invest into a single trust deed as tenants-in-common. The difference between 25102 (e) and 25102.5 is that “e” requires disclosure documents in the form of an offering circular, subscription agreements, and a suitability questionnaire. 25102.5 provides a framework for suitability and investor disclosures within 10237-10238 of the Business & Professions code. Interested parties should consult a real estate or securities lawyer specialist

e) 25102(f) private offering exemption.

The Corporations code sets forth an exemption from the qualification requirement for transactions where (1) the sale is to 35 or fewer persons, (2) each purchaser has a preexisting relationship with the securities issuer, (3) each purchaser represents the purchase is for the person’s own account, (4) the offer or sale is not accomplished through advertising, and (5) the issuer files a notice with the Department of Corporations, within 15 dates from of the issuance. Corporate commissioner’s rule 260.102.14 provides instructions for filing the notice and paying a fee. Failure to file the notice on time negates the exemption.

25102 (f) allows up to 35 investors, with conditions. 25102 (f) does not require California investors or California properties for a particular loan request. Discuss with counsel.

There are three instances when a 25102 (f) exemption may be helpful. (1) when a trust deed requires more than ten investors, (2) when an occasional (accredited investor) out of state party invests in a trust deed on a California property, (3) when a California real estate lender makes a loan on an out of state property.

(f) 25113 provides a path to eligibility for qualification by a permit process. An issuer may apply for a permit to operate under this section and provide the accompanying documentation as required by the commissioner. These permits are usually renewable annually. Caution: Applying appropriate securities exemptions and actions to remain in regulatory compliance is most likely accomplished by consultation with a qualified securities attorney. The above is a general but not all-inclusive overview of securities compliance.

2) California Corporate Commissioners rule 25206.

A broker licensed by the Real Estate Commissioner is exempt from the provisionsof Section 25210(broker-dealers) when engaged in transactions in any interest in any general or limited partnership, joint venture, unincorporated association, or similar organization (but not a corporation) owned beneficially by no more than 100 persons and formed for the sole purpose of, and engaged solely in, investment in or gain from an interest in real property, including, but not limited to a sale, exchange, trade, or development. An interest held by a husband and wife shall be owned by one person for this section.

article continues after advertisement

3) California Code of Regulations, Section 260.204.1

An exemption from the provisions of Section 25210 of the Code is hereby granted, as is necessary and appropriate in the public interest and for the protection of investors, to any person who is a real estate broker as defined in Section 10131of the Business and Professions Code, duly licensed to engage in the business of a real estate broker in this state, and whose business as a broker-dealer, in addition to any transactions within Section 25206 of the Code, is limited to any or all of the following:

(d) Transactions in a series of notes secured by interests

in the same real property, or undivided interests in a note secured by

real property, according to qualification under Section 25110,

Section 25120, or Section 25130

of the Code or according to the exemption contained in Section25102(e),

Section 25102(if) or Section 25102.5, other than an offering which is

made under a registration under the Securities Act of 1933 or a

Regulation

“A” exemption under that Act ( 17 CFR 230.231 et seq.).

California is highly regulated, with other laws passed and pending future legislative bills that diminish property ownership rights and lessen processionary benefits. Real property ownership rights and benefits continue to be eroded.

There are hundreds of code sections about licensing, fiduciary obligations, operation of real estate and mortgage companies, and disclosure requirements for both borrowers and trust deed investors. I omitted the abundantly extensive list of all the code sections because the number is significant. Therein lies the continuous employment of lending consultants, expert witnesses, real estate lawyers, and securities lawyers.

C) Disclosure requirements for trust deed Investors.

A California mortgage broker soliciting an investor to purchase all, or a fractional share of a trust deed must provide a lender/purchaser disclosure statement before taking funds.

A lender/purchaser, disclosure statement 851-C, revised 7/2018

Investor disclosures are in 10232.3 &10232.5 of the California Business and Professions Code.

Business and Professions Codes 10232.3 and 10232.5 outline the disclosure requirements the funding lender must adhere to for a real estate licensee. I am highly familiar with these requirements since I co-sponsored Senate Bill SB 1554 in 1998 and wrote a portion of the language that resulted in adopting the code.

The purpose is to provide the investors with written disclosures to make them aware of the material facts and risks and to enable them to make an informed investment decision.

Address or other means of identification of the real property that is to be the security for the borrower’s obligation.

Estimated fair market value

of the securing property as determined by an independent appraisal, a

copy provided to the lender. However, a lender may waive the

requirement of an independent assessment in writing on a case-by-case

basis, in which case, the real estate broker shall provide the broker’s

reported estimated fair market value of the securing property, which

shall include the objective data upon which the broker’s estimate is

based. A broker has the option of issuing

broker’s opinion of value.”

Age, size, type of construction, and a description of improvements to the property if contained in the appraisal or as represented to the broker by the prospective borrower.

Borrower(s) Identity, occupation, employment, income, and credit data as represented to the broker.

Terms of the loan transaction.

Liens and encumbrances:

pertinent information concerning all liens and encumbrances against the

securing property and, to the extent of actual knowledge of the broker,

relevant information about other loans that the borrower expects

or anticipates will result in a lien recorded against the collateral

property securing the promissory note, created in favor of the

prospective lender. As used in this paragraph, actual knowledge

concerning any anticipated loans means knowledge gained by

the broker through arranging the subject loan or other loans on behalf

of the borrower.

Title insurance: The broker

shall provide the prospective lender with the option to purchase a title

insurance policy or an endorsement of an existing title insurance

policy covering the securing property.

Written loan application (signed) loan application.

Credit report.

Loan servicing provisions: including disposition of the late charge and prepayment penalty fees paid by the borrower.

Industry standards and best practices may expand investor disclosures. Here are recommended guidelines on data accumulation.

Individuals/entities: The borrower may be one or

more individuals or an entity such as a family trust, limited liability

company, or corporation. The procuring loan broker should be able to

articulate who the borrower is and provide

a brief background.

Collateral property:

Describe the property and its uses, along with the address. Describe the

tenancy, income stream, and vacancy if the property is

income-producing. Describe the condition of the property and its

strengths and

weaknesses. Will the property be improved because of this loan?

Purpose of loan:

What is the intended use of the loan proceeds? What other debts are to

be paid as part of the loan? How much net proceeds will the borrower

receive? What will the net proceeds be used for? Will the majority of

the loan proceeds be used for consumer or business purposes?

Some lenders operate under a pooled limited liability format with a California Finance Lenders license. Others operate under a Bureau of Real Estate broker’s license. Some real estate brokers also create pools using one of the various federal and state securities exemptions. Three questions arise: (1) does the entity or the security issuer have a fiduciary obligation to the investors? (2) is the entity required to follow real estate law? (3) can the entity or issuer wave or disregard reasonable and prudent underwriting processes without violating fiduciary or breaking the law?

D) Private-party investors:

Private-party investors may invest by purchasing 100% of a loan, co-invest fractionally, with a small group as tenants-in-common, or in a pooled entity format with other investors. Private-party investors include individuals, family trusts, corporations, IRAs, and pension plans.

Most investors invest with multiple ownership methods (holding titles), such as a family trust for a portion and an IRA custodian for a portion. I have noticed various titles for couples who establish a family trust for themselves and their descendants and invest in each. Multiple family members living in the same home are considered one investor for ten investors or less.

The entire trust deed investment percentage represents the investor’s beneficial interest portion of ownership. For example, if the trust deed investment is for $1,000,000 and the investor purchased $200,000, they would own a 20% undivided interest as tenants-in-common. A $100,000 investor would hold a 10% undivided interest as tenants-in-common with other investors.

article continues after advertisement

Private-party Investors who desire to invest in trust deeds with their available capital understand that they are securing their investment by accepting a signed promissory note from a borrower, a signed and notarized recorded deed of trust on the security property. Investors’ names are affixed on a recorded trust deed as beneficiaries. Investors will also assume there is a title insurance policy with their names connected as beneficiaries.

Trust deed investments usually provide for receiving monthly interest payments from the borrower and are distributed to the investors. The annualized yields are comparatively reasonable. Investor distributions are generally a tiny fraction less due to being charged a servicing fee.

Interested parties should seek loan broker professionals who understand required regulatory compliance, best practices process & underwriting, and correct documentation. Lastly, interested parties should seek someone with an experienced track record as their agent and source of trust deed investments.

Thank You,

Dan Harkey.

Dan Harkey

Dan Harkey is a contributing author to Weekly Real Estate News and is a Business & Financial Consultant. He can be contacted at 949-533-8315 or [email protected].

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/08/mortgage-investments.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-08-25 01:04:382023-08-25 01:04:43Deed of Trusts and Mortgage Investments