Date and time: November 3rd (Friday) and November 4th (Saturday), 2023 9 AM to 3 PM PT (East coast time: 12 PM to 6 PM ET)

Location: Online

article continues after advertisement

About this event

Attention savvy real estate investors, it’s time for another educational and exciting Realty411 Virtual Investing Summit uniting readers for an amazing day of information and motivation.

Register for Our NEW Virtual Investing Summit being held on Friday, November 3rd and Saturday, November 4th, 2023, from 9 AM to 3 PM PT (East coast time: 12 PM to 6 PM ET).

Guests can join Realty411’s complimentary investing summit and learn from experts sharing important knowledge, strategies, and insight.

Realty411 will virtually unite some of the most successful, knowledgeable and savvy investors in the REI (Real Estate Investing) industry to help our readers make educated and informed decisions. These educators have joined our in-person events in the past as well.

Since 2007, Realty411 has produced real estate-investing events and expos throughout the nation.

Our mission is to educate and empower individuals to invest in real estate. Our virtual events have united thousands of new and sophisticated investors in real-time from 47 states so far — in total representing 375 cities across the United States.

Join us for an amazing day of real estate education. Every online event we produce is unique, be sure to reserve this day for REI learning at its best.

article continues after advertisement

OUR COMPLIMENTARY VIRTUAL CONFERENCES HAVE REACHED THOUSANDS OF INVESTORS – THIS IS YOUR CHANCE TO LEARN EXPERT STRATEGIES ONLINE.

* Learn from Leaders & Industry Pros

* Chat with Local + Out-of-Area Investors

* NON-Stop Tips for Real Estate Success

* Learn with Long-Term leaders in the REI Industry

* Receive the Latest REI Knowledge from Real Investors

* Discover the Power of Leverage with OPM and Creative REI

* Save money with Realty411VIP.com’s Merchant Discounts

We Have Been Sharing Life-Changing Information for 17 Years!

RSVP for this awesome event today, additional details, as well as speaker information and updates, will be shared after registering for this event. A Zoom link will be shared with registrants prior to the event.

Join from a PC, Mac, iPad, iPhone or Android device – Schedule will be sent to all guests. Thank you.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

Date and time: Thursday, October 26 · 2:30 – 3:30am AWST

Location: Online

About this event: 1 hour Mobile eTicket

WELCOME REAL ESTATE AGENTS AND BROKERS

Our NEW VIRTUAL event is for existing agents and brokers curious about learning more about the fastest-growing nationwide brokerage, REAL.

Join Realty411 and REAL agent/investor, Hugh Zaretsky, for a special one-hour meeting sharing the benefits of joining The REAL Brokerage.

At this online event, guests will learn about the 9 Ways REAL Agents and Brokers Can Get Paid. You can invite your contacts or team to this informative webinar to learn more about REAL as well — all active agents/brokers are invited.

Be sure to join our Zoom meeting at 11:30 AM PT / 2:30 PM ET, register for this event and a Zoom link will be sent, thank you.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/10/featured-1.jpg470940dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-10-20 02:34:402023-12-14 01:52:11Intro for Curious Agents – 9 Ways to Get Paid with Real + Our National Team

EXECUTIVE VP WITH THE NATION’S LARGEST DISTRESSED MARKETPLACE TO SPEAK ABOUT EXISTING INVESTMENT CLIMATE AT 4TH ANNUAL LA REAL ESTATE GRAND EXPO

Steve Price, Executive Vice President of Foreclosure Auction Services, with Auction.com is scheduled to be the featured Keynote Speaker at the 4th Annual Los Angeles Real Estate GRAND Expo this Saturday, October 21st.

The Expo, which now begins at 8 AM PT, is scheduled to attract over 700 investors from around the nation for one special day of learning, networking and collaboration.

The event is being held in West Los Angeles, California, and features 15 educating speakers and dozens of exhibitor tables from leading real-estate companies.

article continues after advertisement

Guests at this complimentary community real estate event will gain insight into today’s realty investment market from one of the nation’s top leading REI companies.

To put into perspective the impact that Auction.com has on the existing local and national real estate investment landscape, investors can take note that Auction.com is the nation’s largest distressed real estate marketplace.

We are very excited to announce our 4th Annual Los Angeles Real Estate Grand Expo. The Grand Expo returns on Saturday, October 21, 2023, 9:00 am to 6:00 pm. We’re taking over the entire Iman Cultural Center for the day – it’s all ours!

The North Hall (vendor exhibition area), the South Hall (workshops), and the middle parking lot (loaded with workshop tents and food trucks). The theme of this year’s Grand Expo will be “Hedge Inflation – Buy Real Estate”.

Last year, the Grand Expo was the largest real estate event in Southern California. We had over 800 investors, 64 vendors, and 12 national speakers…this year will be even BIGGER!

An entire day celebrating real estate investing and you can be involved. Best of all, the Grand Expo will be FREE to attend. This Expo is going to be big, really BIG! We are hosting investors from around the nation once again.

article continues after advertisement

EDUCATORS. There will be national guest speakers (in three breakout rooms). Here is a partial list of our top educators:

1. Jonah Dew – “The Money Multiplier”

2. Eddie Speed – “Buying Discounted notes”

3. Rusty Tweed – “1031 Tax-Deferred Exchanges”

4. Joe Arias – “How to Get Started Investing”

5. Christopher Meza – “Developing Raw Land”

6. Tony Watson – “Tax Advantages for R.E. Investors”

8. Abbas Mohammed – “Investing in Multi-Residential Properties”

9. Marco Kozlowski – “How to Buy Lots and Lots of Houses”

10. Amanda Brown – “Invest in Commercial Real Estate”

11. Shawn Tiberio – “Marketing for Real Estate Investors”

12. Joseph Scorese – “How to Finance Your Next Deal”

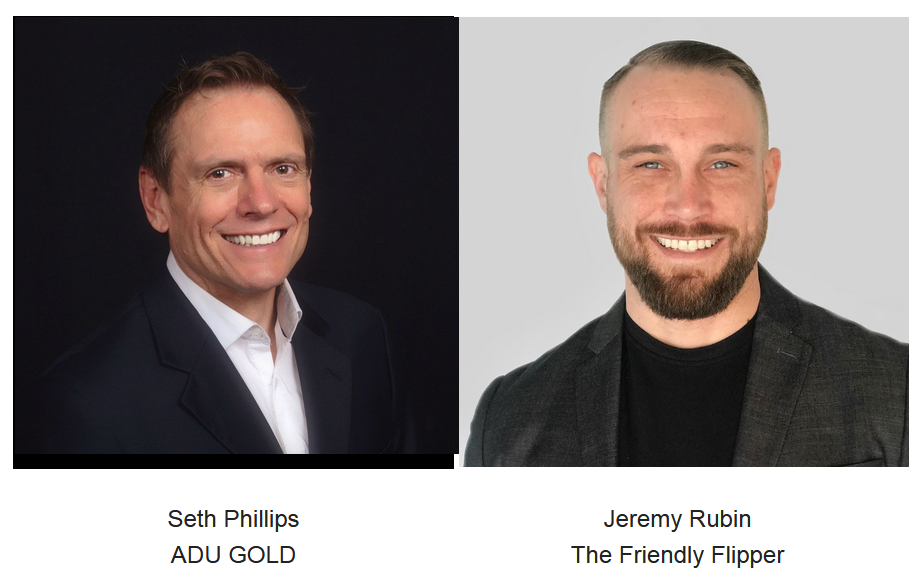

13. Jeremy Rubin — “From Employee to $100M in Flips”

14. Steve Price (Keynote) – Vice President at Auction.com

15 Seth Phillips – BONUS AT 8 AM – “Meet Mr. ADU”

INVESTMENT EDUCATION. An all-day in-depth educational extravaganza celebrating real estate investing. Most importantly, this will NOT be a sales pitch. So regardless of whether you are a new investor, already own properties, or are very experienced, our Grand Expo is for you!

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/10/participants.jpg6601280dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-10-19 04:07:572024-04-17 02:50:34Auction.com’s Executive Vice President to Be Keynote Speaker at the 4th Annual LA Real Estate GRAND Expo – Learn More

The online sale will open October 21 with over 900 properties starting as low as $1,664

LOS ANGELES, Oct. 12, 2023 — The Los Angeles County, California Treasurer’s office will conduct its latest tax sale with a leading online auction platform for distressed real estate sales, Bid4Assets, the leading online auction platform for distressed real estate sales. The sale will feature a mix of vacant land of various sizes and acreage. All auctions will have no reserve price, meaning the highest bid at or above the minimum will win the auction.

article continues after advertisement

By conducting the sale online, Los Angeles County is exposing the sale to Bid4Assets’ national buyer base in order to return a greater amount of distressed properties to the tax rolls. Funds generated from the sale support essential county services, which can face shortfalls when taxes go unpaid.

Los Angeles County previously hosted a virtual tax delinquent property sale in April 2023 on Bid4Assets. This sale resulted in 335 properties being sold at auction, with 202 properties being withdrawn from the auction and $13,051,137 generated in sales proceeds. Bid4Assets has been conducting online auctions for Los Angeles County since 2014.

article continues after advertisement

“We’re honored to serve Los Angeles County and help bring greater levels of efficiency to their tax foreclosure sale process,” says Bid4Assets President Jesse Loomis, “Our format is proven to boost local participation, increase auction sales and free-up staff to dedicate more time towards assisting property owners seeking to redeem their property.”

Auctions will open October 21 beginning at 3:00 PM PT and begin closing at staggered times between 8:00 AM PT and 3:00 PM PT on October 24. A free Bid4Assets account is required to participate in the sale. Bidders must submit a $5,000 deposit to qualify for bidding. Deposits are due by October 17. To view a list of available properties, visit www.bid4assets.com/lasale.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/10/online-auction.jpg5001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-10-13 02:34:232023-10-13 02:34:29Bid4Assets to Host Online Tax-Defaulted Property Auction for Los Angeles County Treasurer’s Office

Are you looking into how to buy a mobile home for real estate investing? First, you need to understand whether or not buying a mobile home will be a worthwhile investment. If you follow the proper steps for mobile home investing, it can certainly be a profitable business venture. Before getting into the steps you need to take to have a profitable mobile home real estate company, let’s first look at the pros and cons of investing in these types of properties.

article continues after advertisement

Pros of Investing in Mobile Homes

Mobile homes are advantageous because

they are cheaper than investing in other types of real estate. Because

they are mass-produced and not built one-by-one like homes, they cost

much less than traditional houses.

Because they are less expensive, you

may be able to invest more money in making them a little more modern.

You can add things like granite counter, hardwood floors, and updated

appliances with the money you save from buying mobile homes. This

increases the value and helps get them rented or sold faster.

As house prices rise across the

country, more and more people are looking for affordable options. As a

mobile home real estate investor, this puts you in a uniquely profitable

situation. Mobile homes are beginning to be seen as a viable option to

replace a more expensive traditional house. Even better, mobile home

tenants tend to rent for more extended periods of time than those in

apartments or traditional homes. This helps you avoid lost rent between

tenants.

Cons of Investing in Mobile Homes

Unfortunately, many people view

mobile homes in a negative light. They do not see them as respectable

options for homes. This view is slowly changing, but it is something to

keep in mind. You simply won’t have the same demand for mobile homes as

you would a traditional property.

Mobile homes can quickly become

costly if you invest in the wrong property. Some mobile homes may

require you to buy the land you want to keep it on. This is something

you need to keep in mind when determining your expenses and return on

investment. You should also note that, unlike houses, mobile homes

depreciate in value relatively quickly. This is great if you want to buy

an old mobile home and fit it up, but not great for resale value if you

ever want to get rid of the property.

Finally, you may run into trouble

trying to finance your mobile home. Traditional lenders often won’t fund

you the way they would if you were buying a traditional house. If the

mobile home you are buying does not already come with land, it’s likely

you will not receive financing. This is something you need to consider

before jumping into buying a mobile home.

Now that we’ve got the benefits and

drawbacks out of the way, we can look at improvements you can make to

mobile homes. These will help raise property value and allow you to

charge more for the mobile home. This can help you develop a good

revenue stream and allow you to grow your real estate investment

portfolio.

article continues after advertisement

Improvements to Increase the Value of Your Mobile Home

Attic

The attic of a mobile home is

probably the most overlooked area, but it has some great potential. Even

if you don’t have the room to build a full-sized building on top of

your home, you can easily create a multi-level living area by installing adequate insulation

on the interior walls. One way to boost your home’s value is to build

an attic loft and add an elevator or stairway connecting it to the

ground floor.

Conversion

A second option for upgrading your

home is to convert it to a larger house. In this scenario, you would

tear out the interior walls and put in new ones. The following are some

other types of conversions that can be beneficial: A sunroom (to create

more living space), an addition on the side (to add more bedrooms), a

deck area (to create outdoor living space), and a basement expansion (so

you have a place to keep all of your possessions that aren’t stored in

the attic).

Upgrades

A third option is a simple upgrade of

the home’s interior. The first thing to do is keep the original ceiling

and replace it with a higher-quality material, such as wood. Some other

upgrades that can be made to the structure include vinyl and natural

flooring, new bathroom and kitchen fixtures, new doors, appliances, and

cabinets.

Landscaping

If you are looking to make your

mobile home more appealing, you should focus on the building’s exterior.

There are plenty of ways that you can upgrade your property to make it

more attractive. You can change out the landscaping, which will provide

an area of privacy and allow for greater land value. One way to make

landscaping more appealing is to add a deck or patio area to have a

designated area for outdoor living space.

Exterior lighting

Another significant exterior

improvement is the addition of outdoor lighting. Lighting can also boost

your home’s value because many buyers prefer homes with street lights,

walkways, and security lights. Your home’s lighting should be made up of

high-quality, energy-efficient HID bulbs to ensure that it is both safe

and functional.

Front Porch

The front porch is a large area that

can be made into a place to entertain or relax. Adding a new roofing

material to your home’s exterior above the porch can give it a facelift

while also bringing in some more value. There are many types of roofing

materials, but the most popular is asphalt shingle. Be sure to get a

warranty with the roofing installation, so if something goes wrong with

it, you can fix it.

Fencing

The final exterior upgrade is

fencing. Fences are a great way to increase the value of your home while

also giving it some privacy and protection. A fence can be made from

many materials, but most are either wood or vinyl.

These are just a few of the ways that

you can go about upgrading your mobile home and making it more

valuable. Just remember to keep the safety of your customers in mind.

Advantages of Mobile Home Investing

There are several advantages to

investing in a mobile home. As stated before, they are cheaper than

investing in another type of real estate. They are easy to find and can

be located in more appealing areas. They can be bought for less than

they cost new. If you don’t have the money to buy your home new, you can

get one that is pretty close to new for a lower price. In addition, you

can find mobile homes that are in great condition and ready for someone

else to move into. That is a rare opportunity to buy a piece of real

estate and have someone else pay you to live in it.

What Determines a Good Property Investment

There are many important factors to consider and evaluate when determining whether or not a home is a good investment:

The property must be located in a strong, healthy real estate market.

The property must offer the potential for both upside and downside growth with a low vacancy rate of tenants.

The property must be professionally managed to keep vacancy rates low and the property in good shape.

The property should be purchased below market value (what it would cost you to build, if ever).

The cash flow should exceed at least 5% per month, preferably more like 15% or 20% per month.

For most people, the ideal investment

would be a home that provides long-term value growth (appreciation) but

with modest increases in monthly income (cash flow).

Tips for Buying Used Mobile Homes

There are several tips that you can

follow if you want to be successful when it comes to buying used mobile

homes. First, make sure you take lots of pictures of the mobile home and

its surroundings so that you can genuinely get a good idea of what it

looks like. Additionally, don’t go into negotiations thinking that the

seller will give you a good deal. Instead, make an offer that you think

is fair, and you can live with. Lastly, remember to avoid being taken

advantage of by people trying to sell you used mobile homes for a lot

more than they are worth. When considering a price that seems fair, look

into recent sales on comparable mobile homes in the area. Take into

account what you plan to make through renting it or reselling it, and

make sure the return on investment is high enough.

Tips for Selling Used Mobile Homes

The following tips will help you

maximize the profit in your mobile home. First, make sure that there is

nothing that needs to be repaired before you sell it. Make any necessary

repairs or changes to ensure that it sells for a profitable and fair

price. Additionally, make sure that you clean out the mobile home of any

personal items. If it is presented as clean and not in need of any

repairs, it will be easy to get someone to pay you a fair price. Lastly,

be entirely transparent about the mobile home and anything they need to

know about it. Buyers who view you as untrustworthy will not want to

buy from you.

Process of Buying a Mobile Home

Conducting a simple investigation

online can help you learn how to buy a mobile home, which is relatively

easy. Once you find a mobile home, you can sign a contract immediately

to ensure that the mobile home doesn’t get sold to anyone else. Once

the contract is signed, the seller will need to provide information

about the property. This information includes details such as who owns

the property and if there are any liens against it. Once all of this

information has been collected, the title will be transferred, and the

buyer will have control over the mobile home.

Summary

When you are looking for a mobile

home, it can be a daunting task. However, if you remember to think about

your needs first and then look at the available mobile homes, it will

make the experience much more enjoyable. Additionally, remember not to

fall victim to scams while looking at mobile homes. Do your research to

find good areas to invest in mobile homes. Understand the best

investments that work with your capital and what you expect to make from

your investments.

Joe Arias and his partners have flipped hundreds of properties in the Southern California Region. He has developed cutting-edge systems to simplify and scale the entire remodel process that can easily be applied to flipping, rentals, wholesaling, and other passive income strategies. More recently, Joe founded a real estate investing education company called RealSuccess Investments, allowing him to share his tools and systems with hundreds of up-and-coming investors.

RealSuccess is focused on education on flipping, rentals, passive income, and wholesaling.

Joe is also a best-selling author. He has written 4 books: Finding your RealSuccess, First Steps to Flipping, R stands for Rentals and Retirement, and Wholesaling Real Estate.

“I came from Argentina when I was 20, I am 40 years old now. I didn’t know anyone, I am CERO generation, usually people say, I am first or second generation but I was the one that crossed the border, no language, no friends, no family, no money, nothing, nada… If I can do it, anyone can.”

From a young latino immigrant to a celebrated real estate investor, Joe is a true testament to hard work and discipline. As an investor, he has made it his mission to help others achieve financial freedom while enjoying living a life of passion, fulfillment, and empowerment.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/10/mobile-homes.jpg5001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-10-12 02:29:582023-10-12 02:30:03How to Buy a Mobile Home for Real Estate Investing

I have been buying and selling residential real estate as a real estate investor for almost 7 years now. I have invested in just about every avenue of real estate investing from Pre-construction, Assignments, Tax liens, Rehabbing, Probate, Bankruptcies, Pre-foreclosures, Short Sales, Foreclosures and REOs, Buy & Hold, and FSBO’s. I have profited from literally all of these strategies and showed others how to as well.

However, lately I have learned about a twist to an old strategy, one that I had heard about, but never done. Buying land and re-selling it via owner financing for a monthly profit, is the new real estate investing strategy. It goes even further, after you buy it and sell it with owner financing you can then eventually flip this property to another buyer. I picked this up from Jack Bosch, who has closed over 5400 land deals himself and I think he is on to something!

article continues after advertisement

I have found the biggest stopping points for many of my new real estate investing students are usually:

#1 – The risk of getting into something they cannot find funding for and letting people down #2 – Getting into a deal and finding out later something was missed, causing financial loss.

Many new real estate investors are frozen stiff because of these fears. It is for this reason I’ve listed some of the reasons a real estate investor might want to add land flipping to their portfolio of investments.

Why Land Flipping Might Be Better

There is virtually no competition for land, especially rural land. This area of investing is over flowing with a lot of opportunity – there is an abundance of forgotten land out there that sells for cheap! You can purchase land for literally pennies on the dollar.

With land you do not have to know as much about real estate like construction, termites, mold and all the other things of that nature that you must know when investing in houses.Here are some compelling reasons to add land flipping to your real estate investing portfolio:

Very low, (or sometimes none), acquisition costs

Lower risk – limited money down to lose

Lower inspection requirements

Quicker closings

Less initial capital output

Buyers are usually more savvy investors

Good Potential for monthly residual income with your owner financing

Usually no upkeep required

Usually low holding costs (no fire insurance, fix up, utilities involved)

Higher number of buyers are repeat buyers (compared to home end buyers)

Why Houses Flipping might be Better

For some real estate investors flipping houses might have been the first investing niche that they started in. Let’s list the major reasons why house flipping is a good investing strategy:

More potential to generate income while you hold it – owner financing or renting

Everyone needs a house since shelter is a basic necessity of life. Not everyone needs vacant land

Potential to profit big doing just one good deal

Potential for higher monthly residual income per property

A lot more home owners in desperate situations than there are landowners.

Compared to the land flipping, house flipping might seem better, but the acquisition and maintenance cost are much higher for house flipping. Another thing to note is that land flipping profits on average, are lower than house flipping, and you must do more deals to profit higher dollars.

article continues after advertisement

Research the Region

Look for these market positives when investing in both land and housing deals:

Unemployment rate in the area of purchase is low compared to the national unemployment rate

Be sure to keep your ears open for news of major business expansions

General area & its population is growing and expanding. If it is, best if the area is expanding in the direction of the property you are interested in buying

Talk to the city and county planning and zoning agencies where the property is located; they will be able to give you valuable information about area growth and building projections.

6 Ways to Minimize Investing Risks

Here is a list on how to lower your risks for investing in houses or land before closing on any deal:

Run necessary tests and inspections depending on specific area and property

Check with county records to verify no complaints or notices for required repairs are filed

Make sure you work with contract escape clauses to assure you can walk away for any reason.

Avoid giving check or cash money down until you are positive you are going to close.

Make sure that your purchase contract is worded in such a way that it allows you to only transfer cash at the time of closing.

Make sure the title is not “cloudy” and property is marketable. Remember IRS liens have to be paid! If you buy a property with those liens, that bill becomes yours. Do your due diligence in running a title report before closing.

Land and House Flipping Similarities

In summary, you can follow a lot of the same strategies marketing to land owners as I’ve always done buying & selling to home owners. The best type of deal, whether land or houses, is when the seller, for one reason or another, wants a quick & easy way out of the obligation of owning their house or land – leaving you the opportunity to buy at a discount and profit in the short and/or long term depending on your goals!

Real estate investing, just like most things in life, has benefits and risks no matter how you look at it. There are always those unknown and unexpected circumstances. In the scheme of things, you need to decide…are you able to live a peaceful, joyful life as you are building your wealth through real estate investing in land and/or houses. Your personal risk tolerance is what only you can decide. I am doing both wholesale land and house flipping and holding, looking at each deal individually. Because most importantly, it is all about profitability and the bottom line!

Most Important!

Universally, success is about having a system, a RE power team and a mentor to help you down the path of real estate investing. Those are the keys to your success. Surround yourself with experienced people who are doing real estate investing successfully – they already have figured out the “code”. You can learn from them so – “Why re-invent the wheel?”, as they say.

Knowing you have experience at your side alleviates those fears of the unknowns, increasing the chances for a faster, easier and happier ride to the peak of real estate investing success. I would like to leave you with a quote:

“Perhaps the very best question that you can memorize and repeat, over and over, is, ‘what is the most valuable use of my time right now?’” – Brian Tracy: Professional Development Author & Speaker

Tamera Aragon

Tamera Aragon is a professional online entrepreneur and has bought and sold over 300 properties, establishing her as an expert in the real estate investing field. Since 2003, she has purchased over 10 million dollars in real estate and currently holds properties all over the world. Tamera’s focus is on the booming Foreclosure market, buying Pre-foreclosures, REOs and Short Sales. Tamera who is a noted Author, Success Trainer, Speaker & Coach, shows her passion for helping others with the 17 websites she has created and several specialized products to support fellow investors throughout the world. When Tamara is not busy running her website, she is very involved with her Fiji joint ventures and investments. Tamera Aragon is one of the few trainers and coaches who is really “doing it” successfully in today’s market. Tamera’s experience has earned her a solid reputation in the industry as well as the respect and friendship of many of the top national real estate investment and internet marketing experts. Tamera Aragon believes her success has garnered her the financial freedom to fully enjoy her marriage and spend quality time with her children.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/10/land-flipping-vs-house-flipping.jpg5001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-10-11 03:09:022023-10-11 03:09:06Land Flipping & House Flipping – Are They Different?

We are very excited to announce our 4th Annual Los Angeles Real Estate Grand Expo. The Grand Expo returns on Saturday, October 21, 2023, 9:00 am to 6:00 pm. We’re taking over the entire Iman Cultural Center for the day – it’s all ours! The North Hall (vendor exhibition area), the South Hall (workshops), and the middle parking lot (loaded with workshop tents and food trucks). The theme of this year’s Grand Expo will be “Hedge Inflation – Buy Real Estate”.

Last year, the Grand Expo was the largest real estate event in Southern California. We had over 800 investors, 64 vendors, and 12 national speakers…this year will be even BIGGER! An entire day celebrating real estate investing and you can be involved. Best of all, the Grand Expo will be FREE to attend. This Expo is going to be big, really BIG!

article continues after advertisement

SPEAKERS. There will be national guest speakers (in three breakout rooms). Here is a partial list of our top educators:

1. Jonah Dew – “The Money Multiplier” 2. Eddie Speed – “Buying Discounted notes” 3. Rusty Tweed – “1031 Tax-Deferred Exchanges” 4. Joe Arias – “How to Get Started Investing” 5. Christopher Meza – “Developing Raw Land” 6. Tony Watson – “Tax Advantages for R.E. Investors” 7. Dani & Flip Robison – “Fixing & Flipping Houses” 8. Abbas Mohammed – “Investing in Multi-Residential Properties” 9. Marco Kozlowski – “How to Buy Lots and Lots of Houses” 10. Amanda Brown – “Invest in Commercial Real Estate” 11. Shawn Tiberio – “Marketing for Real Estate Investors” 12. Joseph Scorese – “How to Finance Your Next Deal” 13. Jeremy Rubin – “From Corporate Employee to $100M in Flips” 14. Steve Price (Keynote) – VP at Auction.com

INVESTMENT EDUCATION. An all-day in-depth educational extravaganza celebrating real estate investing. Most importantly, this will NOT be a sales pitch. So regardless of whether you are a new investor, already own properties, or are very experienced, our Grand Expo is for you!

AMAZING NEW EDUCATORS ADDED!

article continues after advertisement

Expand Your Knowledge of REI in NYC

Network and Learn in Manhattan

This special event will help investors gain specialized insight and knowledge about real estate investing, entrepreneurship, finance and other life-changing subjects. The information shared on this day could catapult your real estate portfolio to new levels of success!

Are you ready to Grow Your Real Estate Business in the East Coast?

This is Your Chance to meet TOP Leaders in REI, Local & National Experts. Learn from Leaders & Industry Pros, NON-Stop Tips for Real Estate Success, Bring Lots of Business Cards!

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/10/FEATURED.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-10-07 06:10:372023-10-07 06:10:42New Educators Added – Get the Latest 411

Please review this important post from our sponsor, thank you.

Hey friend,

What I am about to say will probably offend some people and if you are one of them I am sorry.

However it is unfortunately true so here it is:

The reason tenants complain so much about security deposits is the landlord’s fault.

Yep, that is an unpopular concept among investors but hear me out.

I recently did a survey among thousands of tenants and investors and found some very interesting data.

Nearly 60% of tenants are concerned about getting their deposit back and feel the landlord will try to take unfair deductions.

But after digging in a bit further it turned out that only 19% have actually had unfair deductions in the past (per them).

Wild that so many complain but only a small amount actually experienced it!

We have all had to deal with tenant complaints and arguments on the deductions but why are they actually complaining so much?

As investors we are not “out to get” the tenants as they may think. Sure we are in it for a profit but not to put them on the streets…

So why all the noise?

I can tell you I found the reason and it is quite a shocker, even for me:

By survey, 59% of leases had no inspection done or no photos taken.

Yep, that’s right. The majority of leases didn’t even have photos prior to the move in.

So how do we expect to have any sort of agreement on deductions when it is based on what the tenant remembers it to be? Naturally there is going to be a difference of opinion.

Of course the logical answer is that tenants should take photos for themselves but do we really expect them to do that? Not likely. And it is actually our property so it is in our interest to property document it.

This was the problem I was running into and I created a simple solution for it which I wanted to share with others.

And if you are already using another property management software then I have a solution for that as well.

I took the inspection feature and made it into a separate app that is super simple that you can use to do inspections. Not free but very cost effective and will save untold misery…. (free account creation so you can look around).

I am sharing these as I found them helpful with my rentals and I think you will too!

Enjoy!

Sean Tanner

RE Investor & CEO of Lease Protector

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/10/dont-read-this.jpg5001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-10-06 11:33:122023-10-06 11:33:16Don’t read this (it will make a lot of people angry)

Asset-Based Lending Can Boost Your Borrowing Capacity

A real estate investor can get financing for an investment property through asset-based lending. This kind of loan is determined by the borrower’s liquid assets and credit score, not by their income or employment history.

When compared to dealing with institutional banks, the asset-based loan application process is typically quicker, requires less paperwork, and results in cash in hand sooner, allowing you to make larger purchases and advance as a real estate entrepreneur. Asset-based loans are a specific type of bridge loan (12-24 months) used only for investment and commercial properties.

article continues after advertisement

If you have a foreclosure on your record or poor credit and are having problems securing a loan from conventional banks, asset-based lending can be advantageous. It is particularly beneficial if your real estate investing business is expanding quickly and you need money to keep going.

How Do Asset-Based Loans Work?

Hard money lenders in asset-based lending use your collateral, in this case real estate, to assist you in getting more money to finance additional real estate projects. If your money is invested in real estate, it is not liquid, and if your business is expanding quickly, it’s likely that you need more money to keep expanding. Hard money lending can help in this situation.

Compared to traditional banking institutions, hard money lenders can provide you cash faster, with less red tape and more flexibility. A hard money lender will consider your accounts receivable, equipment, and inventory in addition to the equity in your current real estate assets to determine the amount of your loan. Hard money lenders typically charge a higher interest rate than standard banks because the real estate is not liquid and you are not borrowing against your own income.

What Are The Benefits of Asset-Based Lending?

Asset-based financing has a number of advantages, whether you’re attempting to find out how to fund a multi-family property or require a commercial loan.

These loans often close more quickly and with less paperwork than traditional loans. These loans have less stringent underwriting requirements and higher interest rates, but they also close more quickly than term loans.

The gap between expenses and incoming cash receipts for your company can be filled by cash flow asset-based lending solutions.

article continues after advertisement

The loan amount is unrestricted, so you are free to utilize it however you see fit (such as equipment purchase.)

Stratton Equities will make it simple for you to convert your collateral into cash through asset-based financing so you can fund your next big idea. Call Stratton Equities at 800-962-6613, send us an email, or fill out an application for loan pre-qualification right away if you have an investment or commercial property and would like to talk with one of our Loan Officers.

Michael Mikhail, CEO Stratton Equities

Michael Mikhail is the Founder and CEO of Stratton Equities, the nation’s leading hard money-lender to national real estate investors, with the largest variety of mortgage loans and programs nationwide.

Having launched Stratton Equities in early 2017, Michael has always been an entrepreneur and innovator in the real estate market, purchasing his first home at 19.

A serial entrepreneur with a foresight for business opportunities, Michael had a slew of small businesses prior to launching Stratton Equities. One of his most prolific ventures was a car wash connected to a gym he was affiliated with in Florida during 2001-2002 while attending college.

It wasn’t until he graduated from Florida State University with a degree in Business, that he officially joined the mortgage industry in 2003 and decided to travel to explore his options globally.

After travelling to 19 countries in 5 years, Michael knew two things; he wanted to start his own business and launch it in the United States. He knew that moving back to the states was the best place he could start something small and grow it into something infinite.

In 2017, Michael noticed how the mortgage industry had transformed after the regulations presented from 2008-2012, and knew it was time to set out something on his own, thus creating Stratton Equities.

Under Michael’s leadership, Stratton Equities has grown into one of the biggest leaders in the Mortgage and Real Estate industry across genres and platforms.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/10/interest-rates.jpg5001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-10-05 02:55:402023-10-05 02:55:44How To Win at Real Estate Investing Despite Sky-High Interest Rates

If you are thinking about getting into the real estate investment business, you might consider starting a property management company. A good deal of experience and knowledge is required, but it can be quite lucrative if you succeed in setting up a profitable property management company. This article will go over the necessary steps to set up a successful property management company and start making money through real estate investing.

Decide What Type of Legal Entity You Are

If you’re interested in setting up a property management company, you’ll need to establish a legal entity. Many different legal entities can be used in the real estate investment business, but the most common is a limited liability company (LLC). An LLC can be a good choice because it allows you to operate an enterprise as an individual or with partners without worrying about filing forms and going through the costs of becoming an S Corporation. An LLC might not be the right choice for everyone, so it’s important to talk with your attorney to determine the best option for you.

Obtain a License

You need to complete one more important step before you can begin your property management company. You’ll have to get a real estate license. Each state has different requirements for getting a real estate broker’s license, so you’ll have to check your state’s licensing and regulation department to determine the specific requirements. A real estate license will allow you to perform transactions on behalf of a property owner as a property manager and will enable you to handle all related paperwork. Depending on your state, you may also have to get a property management license, limiting you exclusively to property management.

Brand Your Business

Now that you’ve established your legal entity and obtained a license, it’s time to brand your business. Decide on a company name and logo. You may even decide to hire a professional to help you determine your branding. You may not realize it, but font choices and color go a long way in establishing yourself as a reputable, trusted company.

Separate Your Finances

It’s essential to open a bank account for your business to keep it separate from your personal expenses. This will help you keep track of your business and avoid any trouble when doing taxes.

article continues after advertisement

Create a Website for Your Business

Once you’ve established your legal entity and obtained a real estate license, it’s time to create a website for your property management company. Many property management companies use websites to establish their brand, conduct business online, and keep records of interactions with clients. A good website will cost some money, but if you choose the right web developer, you can create a great-looking site that is optimized for Google. This will ensure that anyone looking for a property management company will come across you before your competitors.

In today’s world, it’s more important than ever to have an online presence. Your website needs to be filled with important keywords that your clients could be searching for. These will help you show up in their Google search results and will lead to more business. Knowing what you are doing online makes you appear more reputable and will help gain trust and credibility. If you don’t know where to start, consider hiring someone to take care of your digital marketing.

Hire a Real Estate Team

Any good real estate investor knows that you’re only as good as the team you work with. As a property management company, you will want to create a solid real estate team to help you succeed. Starting off, the three most important professionals you will need are an accountant, a real estate lawyer, and a trustworthy contractor. An accountant will be necessary to manage the day-to-day accounting related to your company’s operations. A real estate lawyer will play a key role in handling any legal issues that might come up. And a contractor will be necessary for everything from mowing lawns to painting houses. Each of these professionals can represent you at public meetings, so you don’t have to attend them all the time personally.

Set Up Property Management Technology

When you’re running a property management company, it’s crucial to have a good system for keeping track of everything that’s going on. A few years ago, this would have been much harder to do, but you can set up an entire system just using the internet with today’s technology. There are specially designed services for companies looking to increase efficiency and cut down on expenses through technology. From customer and vendor management tools to marketing solutions, you can find what you need through an online service. If you plan to manage short-term rentals, you will need management software that helps you keep track of all check-ins and check-outs, as they will be more frequent and hard to keep track of on your own.

article continues after advertisement

Establish a Pricing Structure

Once you have the basic nuts and bolts of your business taken care of, it’s time to establish pricing. Your pricing structure will differ based on the type of real estate that you’re managing. For instance, if you manage properties in a city where there is a lot of demand for affordable housing, you may be able to charge less than if you were managing high-end condos in a neighborhood with very little retail space. An excellent first step if you are just starting off is checking and seeing what competitors are charging in your area. Some fees to consider when creating your pricing structure are:

– Setup Fee: This is a one-time fee that is charged to new clients as soon as you take the job.

– Property Management Fee: This is the monthly amount that you charge for managing each property on your list.

– Real Estate Commissions: This is the percentage of your client’s total rent that goes directly to you. Technically, it’s called a ”total real estate charge,” but most property managers call it a “fee.

– Ongoing Management Fee: This is a percentage of the total rent that you charge each month to have you manage your client’s property.

– Maintenance Fee: This is an hourly fee that you charge your clients for any maintenance or repairs that need to be done at their property.

– Multiple Management Fee: If a client is also using another property management company, then you can charge the rental amount of one of the properties as a multiple management fee for your services.

– Leasing Fee: This is a fee that occurs when there is a vacancy that you need to fill. It covers the cost of staging, listing, showing, and eventually renting the unit. It typically comes out to about one month’s rent.

– Insurance Fee: If you take on a bigger job that requires higher insurance coverage, then you can charge an additional fee per month to cover the extra cost of the insurance.

– Renewal Fee: If there are any fees associated with renewing a rental agreement, then you can charge your client an additional renewal fee as part of your monthly management fee.

– Eviction Fee: If you need to evict a tenant for violation of the lease, then the landlord can charge the tenant an additional fee as part of your management fee.

– Deposits: If your clients are required to pay a deposit when they sign their property management contract, then you can collect a monthly percentage of that deposit.

– Pet Fee: If the property is set up for pets and has pet deposits, then you can collect an additional fee from those who choose to rent with pets.

Pursue a Marketing Strategy

Regardless of what marketing strategies you choose, you need to make sure they are appropriate for your business. For instance, if you’re just starting out, you might want to focus on word-of-mouth referrals from existing clients. If you already have several clients or a steady number of people coming into your business, then it might be best to focus on local advertising through classifieds.

If you’re just starting out, you’ll need to work a lot harder than the more established property management companies. The best time to start marketing your business is when you are still very new and unsure of the business. Don’t ever take on too much at the same time. Let your current clients know what your services are and how this will benefit their rental property. Then start new accounts by providing referrals from other potential clients in your area.

For a more modern marketing approach, take advantage of social media and digital ads. Create a Facebook page and an Instagram and update it often. Since the same parent company owns the two social networks, you can run ads across both platforms for a reasonable amount of money. Facebook ads can be adjusted to target specific demographics, locations, and niche interests. You will also want to either learn how to run Google ads or hire a company specializing in them. Investing a few dollars per day into some high-ranking keywords in your field may help you pull in leads and get your first few clients.

Network

Many people find the most effective way to market their business is to get to know their potential customers simply. This means going out and meeting them, but it also means making a personal connection through social media. Once you’ve established a rapport with someone, you might be able to refer them to your business later.

Summary

Once you learn how to start a real estate property management company, the next step is to make it successful. Even the best business plan doesn’t mean much if you can’t market it correctly. It’s essential to understand your target audience and have some marketing strategies in place before you set out on meeting people and renting out properties. Moving forward, be sure to track your progress. Keep a log of all important numbers, such as contact information for people who expressed interest in your business, how many units you rented out, etc. Keeping tabs on your company’s progress might help you if you decide to apply for bank loans or seek investors in the future. If you have trouble getting started, find a mentor who already runs a property management company and learn through them before you are ready to get started on your own.

To learn more about a career in real estate investment, make sure to sign up for our investment seminars.

Joe Arias and his partners have flipped hundreds of properties in the Southern California Region. He has developed cutting-edge systems to simplify and scale the entire remodel process that can easily be applied to flipping, rentals, wholesaling, and other passive income strategies. More recently, Joe founded a real estate investing education company called RealSuccess Investments, allowing him to share his tools and systems with hundreds of up-and-coming investors.

RealSuccess is focused on education on flipping, rentals, passive income, and wholesaling.

Joe is also a best-selling author. He has written 4 books: Finding your RealSuccess, First Steps to Flipping, R stands for Rentals and Retirement, and Wholesaling Real Estate.

“I came from Argentina when I was 20, I am 40 years old now. I didn’t know anyone, I am CERO generation, usually people say, I am first or second generation but I was the one that crossed the border, no language, no friends, no family, no money, nothing, nada… If I can do it, anyone can.”

From a young latino immigrant to a celebrated real estate investor, Joe is a true testament to hard work and discipline. As an investor, he has made it his mission to help others achieve financial freedom while enjoying living a life of passion, fulfillment, and empowerment.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/10/property-management.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-10-04 03:06:272023-10-04 03:06:34How to Start a Property Management Company