Date and time Saturday, February 24, 2024 · 9am – 6pm PST

Location THE ATRIUM HOTEL 18700 MacArthur Blvd. Irvine, CA 92612 United States

Refund Policy Contact the organizer to request a refund. Eventbrite’s fee is nonrefundable.

About this event 9 hours Mobile eTicket

Discover the Latest Insight, News and Investment Strategies at Realty411’s National Investor Summit in Southern California.

Investors, we have exciting news, insight and networking at Realty411’s new in-person investor summit in Southern California. Our special one-day conference will host incredible educators from around the country, who are ready to share their valuable insight with our guests.

Since 2007, Realty411 has united thousands of investors from across the nation. Guests will receive our latest publication featuring wonderful resources, insightful news and educational articles.

While the mainstream media is focused on high interest rates, we know this is the best time to locate and purchase properties in California and around the nation. The money is made on the buy — by purchasing the right properties. Do you know what they are? We’ll teach you insight that only real estate investors with years of experience can share.

Be sure to download the latest Realty411 to learn more about real estate investing, CLICK HERE.

Now is the moment to grasp this opportunity — the chance to network with sophisticated investors from California and around the country. Upgrade as a VIP Guest ($49) and join us for a delicious buffet lunch as well.

Be sure to pencil this date now and join us in-person to gain specialized insight and knowledge. The information shared on this day could catapult your portfolio to new levels. Discover our new property portal, our VIP perks, plus connect with new and past industry resources.

This one-day conference has something for everyone regardless of their experience level in real estate. Join this memorable day and receive knowledge for a lifetime.

Learn the Latest Niches in Real Estate + Connect with Influential Investors from across the nation right here in Southern California.

Are you ready to Grow Your Real Estate Business, Portfolio and Network?

We want this VIP EVENT TO EXPAND YOUR MIND and help you succeed.

This is Your Chance to meet TOP Leaders in REI, Local & National Experts:

Learn from Leaders & Industry Pros

Meet Local PLUS Out-of-Area Investors

NON-Stop Tips for Real Estate Success

Bring Lots of Business Cards

This event is produced and hosted by Realty411.com. Our company is based in Central California. Since 2007, we have dedicated our time, resources and energy to help expand real estate investing knowledge and education by producing complimentary magazines, virtual conferences, webinars, podcasts, and live events.

We also produce REI Wealth magazine, which is the longest-running magazine for investors specifically developed for online readership. Our digital, interactive issue is designed to be read and viewed online, CLICK HERE.

INVEST YOUR TIME HERE FOR ONE SPECIAL DAY OF NETWORKING & MOTIVATION – TAKE YOUR REAL ESTATE KNOWLEDGE TO A WHOLE NEW LEVEL.

Learn from NEW speakers and new topics — What can expect?

Receive the latest REI knowledge from active investors

We feature the latest technology to expand your income

Meet other investors with common goals and mindsets

Develop relationships with leaders in the industry

Share your opportunities with potential clients

Learn how to save money with our Realty411VIP.com members’ network — must have a special code when ordering

Realty411’s publisher has owned national rentals for many decades

We will share life-changing information unavailable anywhere else

We host in-person events to meet our readers and to spread knowledge

Our mission is simple: To provide realty knowledge and resources so that everyone can learn about the benefits of investing.

OTHER SPECIAL BONUS PERKS INCLUDE:

Early-Bird Guests Receive Our Investment Magazines (while they last!)

Meet Local Leaders & Industry Giants – From Coast to Coast

Influential Real Estate People & Business Owners Are Attending

Learn How to Leverage and Meet Private Capital Lenders

Find Potential Partners, New Friends, Build Your Circle of Influence

Your Net Worth = Your Network — Don’t miss this event

Mingle with Leaders & Industry Professionals Here

Please bring LOTS OF BUSINESS CARDS, it’s time to Network! Learn more about our magazines and our company sponsors and resources, visit Realy411.com

Join Us to Meet with Fantastic Companies and Network with Experienced Real Estate Investors — Realty411 has Reached Thousands Since 2007

Date and time Saturday, February 17, 2024 · 9am – 3pm PST

Location The Cliffs Hotel & Spa 2757 Shell Beach Rd Pismo Beach, CA 93449 United States

Refund Policy Contact the organizer to request a refund. Eventbrite’s fee is nonrefundable.

About this event 6 hours Mobile eTicket

Discover the Latest Insight, News and Investment Strategies at Realty411’s National Investor Summit in Southern California.

Investors, join us for exciting news, insight and networking at Realty411’s new in-person investor summit in one of the most beautiful areas of California, the Central Coast. Our special one-day conference will host incredible educators from around the country, who are ready to share their valuable insight with our guests.

Since 2007, Realty411 has united thousands of investors from across the nation. Guests will receive our latest publication featuring wonderful resources, insightful news and educational articles.

While the mainstream media is focused on high interest rates, we know this is the best time to locate and purchase properties in California and around the nation. The money is made on the buy — by purchasing the right properties. Do you know what they are? We’ll teach you insight that only real estate investors with years of experience can share.

Be sure to download the latest Realty411 to learn more about real estate investing, CLICK HERE.

Now is the moment to grasp this opportunity — the chance to network with sophisticated investors from California and around the country. Ticket holders can upgrade as a VIP Guest ($27) and join us for a networking breakfast at 8:30 AM. The event begins promptly at 9:30 AM

Be sure to pencil this date now and join us in-person to gain specialized insight and knowledge. The information shared on this day could catapult your portfolio to new levels. Discover our new property portal, our VIP perks, plus connect with new and past industry resources.

This one-day conference has something for everyone regardless of their experience level in real estate. Join this memorable day and receive knowledge for a lifetime.

Learn the Latest Niches in Real Estate + Connect with Influential Investors from across the nation right here in Southern California.

Are you ready to Grow Your Real Estate Business, Portfolio and Network?

We want this VIP EVENT TO EXPAND YOUR MIND and help you succeed.

This is Your Chance to meet TOP Leaders in REI, Local & National Experts:

Learn from Leaders & Industry Pros

Meet Local PLUS Out-of-Area Investors

NON-Stop Tips for Real Estate Success

Bring Lots of Business Cards

This event is produced and hosted by Realty411.com. Our company is based in Central California. Since 2007, we have dedicated our time, resources and energy to help expand real estate investing knowledge and education by producing complimentary magazines, virtual conferences, webinars, podcasts, and live events.

We also produce REI Wealth magazine, which is the longest-running magazine for investors specifically developed for online readership. Our digital, interactive issue is designed to be read and viewed online, CLICK HERE.

INVEST YOUR TIME HERE FOR ONE SPECIAL DAY OF NETWORKING & MOTIVATION – TAKE YOUR REAL ESTATE KNOWLEDGE TO A WHOLE NEW LEVEL.

Learn from NEW speakers and new topics — What can expect?

Receive the latest REI knowledge from active investors

We feature the latest technology to expand your income

Meet other investors with common goals and mindsets

Develop relationships with leaders in the industry

Share your opportunities with potential clients

Learn how to save money with our Realty411VIP.com members’ network — must have a special code when ordering

Realty411’s publisher has owned national rentals for many decades

We will share life-changing information unavailable anywhere else

We host in-person events to meet our readers and to spread knowledge

Our mission is simple: To provide realty knowledge and resources so that everyone can learn about the benefits of investing.

OTHER SPECIAL BONUS PERKS INCLUDE:

Early-Bird Guests Receive Our Investment Magazines (while they last!)

Meet Local Leaders & Industry Giants – From Coast to Coast

Influential Real Estate People & Business Owners Are Attending

Learn How to Leverage and Meet Private Capital Lenders

Find Potential Partners, New Friends, Build Your Circle of Influence

Your Net Worth = Your Network — Don’t miss this event

Mingle with Leaders & Industry Professionals Here

Please bring LOTS OF BUSINESS CARDS, it’s time to Network! Learn more about our magazines and our company sponsors and resources:

Discounted parking available. Upgrade to a VIP ticket to enjoy special bonuses.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/11/Invest-in-Real-Estate.jpg470940dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-11-30 03:31:502024-04-17 02:50:22Realty411’s Central Coast Investor Summit – Connect & Learn with Experts

It is no surprise that mortgage rates have dramatically increased over the past year. In July 2022, 30-year fixed rates for both conforming and high-balance loans had reached 5.375%, according to sources such as Guaranteed Rate. This is up from the low 2% range in early 2021. Obviously, such an increase in rates can have a dramatic effect on house prices as would-be buyers try to buy a house they can afford.

article continues after advertisement

However, the rise in interest rates goes far beyond just what buyers can afford for a new purchase. First, adjustable-rate mortgages will climb dramatically, which will impact homeowners trying to make sure they keep up with their mortgages by not going into default. Next, the whole reason the Fed increased rates was to stave off even more inflation than the country had been experiencing since the change in presidency. Here is where we might see a rise in non-performing loans [NPLs], as homeowners fight to keep up with inflation as well as rising interest rates that impact mortgages and other borrowings [credit cards, auto loans, etc.].

During The Great Recession, the U.S. saw a huge wave of defaults with mortgages; primarily, this was due to a credit bubble, as lenders were too eager to make loans. Very little oversight was seen regarding these loans, and borrowers who should not have been granted loans still qualified. Fast forward 15 years, real estate prices have increased substantially to overcome the devastation of the previous drop.

Banks, thanks to Dodd-Frank, are now only allowed to make loans to borrowers who can demonstrate an ability to repay. All of this makes for a strong real estate market, and we should not experience the wave of foreclosures we previously saw; however, that does not mean we will not see them.

As noted above, when there is a spike in interest rates [and inflation] as we have recently experienced [and potentially more increases to come], homeowners can get behind in their mortgages, and without the government moratoriums that were in place during Covid, banks will have to start foreclosing, or sell off mortgages to keep within Federal guidelines of Reserve Requirements. The banks may try and work modifications or other remedies to assist homeowners, but there are times when there is not much the bank can do except file notices of default and start the foreclosure proceedings.

article continues after advertisement

One major difference in today’s real estate world as compared to The Great Recession is that, today, many homeowners have ample equity in their houses. This gives the homeowner the possibility of preserving some equity by selling their house rather than get foreclosed on. However, many homeowners around the country, mostly in the lower end market, will still lose their house in foreclosure. One reason is that the homeowner has not researched the value of their house; they just assume that if they cannot pay, they lose the house. Another is that some homeowners are headstrong about staying in their house and trying to fight a legal battle only to be on the wrong end and, by that time, it is too late to try and save their equity. These situations are unfortunate, as, even when the lender points these things out, many borrowers stick their head in the sand and let the chips fall where they may.

Investors have been clamoring for yield. So much so that even NPLs were commanding unheard of prices [as much as 85% of face value]. As the economy was doing well [pre-Covid], real estate prices were steadily increasing and there was confidence in the marketplace. However, in “normal” times, one might offer 50% +/- of the face of the NPL note, as there is a fair amount of work that goes into managing a NPL regarding foreclosure, forbearance, modifications, bankruptcies, and possible lawsuits by the borrowers. As interest rates rise and the supply of NPLs is sure to increase, one should expect the prices of the NPLs to decrease – – allowing investors to potentially pick up handsome profits.

In the early 1990s, the S&L crisis provided such opportunities to investors swooping up “bad loans”, as the S&Ls were directed to unload these mortgages into the market very quickly. As the dust settled, as it usually does after wide pendulum swings, these investors profited, as they picked up loans [or property if the foreclosure had already been completed, and the bank held the asset as an REO] at discounts that were previously only imaginable. Discounts of more than 60% were not uncommon. At such a discounted price, the investor appeared to not take any undue risk. There was so much room for error, almost any loan to be purchased was worth it.

We may not be in that same situation now due to restrictive banking regulations that have been imposed on banks for years, prohibiting them from making unreasonably risky loans and the fact that real estate has held its own since The Great Recession, but there should be plenty of opportunity for investors to pick up discounted loans with fairly large margins built in; however, the average investor is prohibited from participating in buying these loans due to the relatively large amount of capital needed to enter this space. For example, a large bank or hedge fund willing to unload NPLs may require a buyer to invest a minimum of $1,000,000 or more. If there is a bidding situation [auction], a refundable deposit is usually required, so the bank/hedge fund knows they are dealing with serious, wealthy buyers.

For those investors who have the wherewithal to participate in purchasing NPLs, they should have a sophisticated team to assist them, as there will be a need for analysts to do a deep dive in the values of the property to which the loans are secured, contractors to help facilitate potential rehabbing of the property if/when the property reverts to the investor, legal analysts dealing with the various foreclosure laws in the states where the properties are located, and good real estate sales people to not only give BPOs — but also help facilitate the eventual sale of the property or assist with the possible rental of the same [or find a good management company].

One strategy to consider is to approach the NPL borrower and try to re-write or modify the loan [of course, before doing so, consult with competent legal counsel to make sure that there are no legal issues that would compromise the collateral]. There are a few benefits to this strategy; first, turning a NPL into a performing loan brings immediate cash flow. Because of the discount that is obtained in the purchase, the new note holder has the flexibility of making the note more attractive for the borrower. For instance, if a note [that has a face value of $100,000] has 20 years to go and has a note rate of 6% was purchased for 60 cents on the dollar from the bank, the new note holder could offer to lower the balance to $90,000 and reduce the interest rate to 5% and have a great asset that can either be held for cash flow or sold in the secondary market.

One additional factor that may help in modifying the NPL’s notes is the fact that, according to Bank of America’s internal data, rents continue to rise. July 2022 year over year showed an increase in rents of 7.4%. Most people want to keep their home. If the lender can give them advantages to saving it, most homeowners will jump at the chance, especially when their alternative is to be thrown into a rising rent market. A question the lender has to contemplate is whether the strategy of keeping a homeowner in their home makes economic sense [ignoring the moral issue of eviction]. In some cases, evicting a homeowner and immediately selling the house may make sense.

In some cases, the lender may choose to invest money in rehabbing the property in hopes of additional gain, but there is uncertainty with this strategy; the time it takes to rehab, the expense, and the value of the house after rehab and time to sell [with expenses associated with the sale]. When a homeowner is going to get foreclosed on, there are avenues that can be taken to delay the inevitable, including filing bankruptcy. Due to court budgets, this delay may be prolonged more than the lender originally anticipated, especially in judicial-only states.

The time and expense for entering into foreclosure for the lender may not be worth the anticipated profit; however, the strategy of keeping the homeowner in place and working out a new deal can produce immediate cash flow, as the borrower will start making payments right away. In addition, the costs to modify a note are substantially less than what foreclosure costs would normally be.

The good news from the lender’s point of view is that, due to the purchase of these loans at steep discounts, rates of returns in excess of 15% are not uncommon. After the note is modified, the lender has the option to flip the note to a note buyer as a performing note [which will command a higher price than an NPL], or the lender may choose to keep the note for the cash flow. In the case of choosing to sell the note, the lender may be wise in waiting to experience six months of performance by the borrower, as most note holders desire to see notes that have at least six months’ seasoning; otherwise, they may discount the note for uncertainty reasons [lack of history] more than the lender desires.

MEET EDWARD BROWN

Edward Brown currently hosts two radio shows, The Best of Investing and Sports Econ 101. He is also in the Investor Relations department for Pacific Private Money, a private real estate lending company. Edward has published many articles in various financial magazines as well as been an expert on CNN, in addition to appearing as an expert witness and consultant in cases involving investments and analysis of financial statements and tax returns.

Edward Brown, Host The Best of Investing on KDOW AM1220 on Saturdays at noon.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.FacebookTwitterShare

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/11/non-performing-loans.jpg5001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-11-28 05:08:202023-11-28 05:08:23The Rise of Non-Performing Loans and Opportunity for Investors

Starting in the late 1970s and up through the 1990s pitchmen were all over television extolling the ease at which you could “become rich in your spare time” if you just followed their real estate investment “program.” After 52 years in the real estate investment business, I know of no one who became rich through real estate quickly (I am sure some investors got rich quickly through luck, but I have never met one).

I do know a lot of people who became rich using real estate as their vehicle. They all earned it by working hard and putting in years of devotion.

This article for Realty 411 is for all of you who have not yet become a millionaire in your “spare time.”

article continues after advertisement

What does all this have to do with cockroaches?

When it comes to being able to survive and expand its operations, nothing has ever surpassed the lowly cockroach. Despite chemical warfare, I often find them in my houses after tenants vacate. Some tenants seem to cohabitate with cockroaches intentionally (and quite well)!

In New York’s Museum of Natural History, they used to point tourists’ attention to a pickled roach between the toes of their biggest dinosaur to demonstrate that roaches have survived in the same form since the period before dinosaurs stalked the Earth.

This means that cockroaches lived on even after the mass extinction of the dinosaurs. For perspective, man has been on Earth during only 1% of the time that cockroaches have existed on the planet!

How have cockroaches survived?

How have cockroaches survived so successfully for millions of years? 1). It never challenges anything bigger than itself 2). It stays out of sight 3). It can survive for lengthy periods under adverse conditions or in a hostile environment 4). It is fast and elusive 5). It lives in the cracks of society never calling attention to itself 6). It reproduces quickly and with ease 7). It can make a meal out of about anything organic regardless of how unappetizing!

article continues after advertisement

What can we learn from the cockroach lifestyle?

We small investors must be adaptable, maintain a low profile, and be prepared to move quickly when either an opportunity or danger presents itself. We must be able to recognize opportunities, whether foreclosures, rehabs, discounted paper, single-family house opportunities, or value-added property prospects. We must also avoid hostile environments (and hostile tenants) which are high on risk and low on rewards.

You can skip “make a meal out of about anything organic”. I don’t recommend that.

About those Pitchmen

I knew a real estate guru once that bragged that he bought a property every month. He later confessed that he felt so obligated to follow through with that public statement that he would buy bad deals just to “keep up his image” as a monthly property buyer.

Be patient, be diligent, analyze, and then act. Some investors never succeed because they catch the “paralysis of analysis” fever. They buy books (sometimes they even read those books they buy), attend meetings, talk with other investors, analyze data, buy mentor programs, and never buy any real estate.

I encourage you to learn more by going to my FREE online training at www.landtrustwebinar.com/411 and text the word “reasons” to 206-203-2005 for my free booklet, Reasons to Use a Land Trust. You can also reach me the old-fashioned way by calling me at 217-355-1281. (I actually answer my own phone, unlike most other businesses in America today!)

Apply these lessons from a cockroach lifestyle and you WILL succeed!

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/11/cockroach.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-11-21 05:06:122023-11-21 05:06:15Behold the Cockroach – It has survived and thrived

It is a fact that it is hard to break out

of the middle class and become wealthy. There are many obstacles that must be

overcome. The good news is that most of these obstacles can be easily overcome

through education. Not formal education, high school, or college, but from

self-education.

I was born and raised middle class. The

strategies that the middle-class implement were engrained in my head.

article continues after advertisement

The strategy was to do well in high school,

go to college, get a job, scrimp, and save in an IRA or 401k, work for 45

years, retire, and live off of your savings. This was the map I was given. I

bet that map sounds familiar to you, doesn’t it? All middle-class people are

given this map. The problem is the map doesn’t work. Ninety-five percent of

Americans fail to retire by age 65 using this map. The average savings for a 65-year-old

is less than $200,000. No one can retire with that amount of money.

What opened my eyes was after working for

the same company 70 hours a week, for 5 years straight, I won a national sales

contest. They sent me to Hawaii for a week. When I got back, they cut my pay by

$20,000 a year. This woke me up that the map was wrong. I had to do something

different. I began self-educating. I bought every book and tape program off

late-night TV on real estate investing. Within 2 months I was making more money

than at my job. I quit the 70 hours a week immediately. It saved my marriage by

the way.

Here are six things that I learned that

keep the middle-class, middle-class.

Number 1:

Thinking you can

cheap your way through life and save enough to retire.

People cut coupons, conserve water and

electricity. They drive across town to save a dollar on tomatoes. They think

they can be cheap and save their way to retirement. This is just not true. You

may be able to save a few hundred dollars a month being cheap, but think about

it, can you live off a couple of hundred dollars a month in retirement?

Let’s do the math. Let’s say you work from

age 20 to 65 (45 years). You make an average of $100,000 a year. Less at the

beginning, more toward the end of your career. That is $4.5 million over the 45

years.

Let’s say your average expenses were $5000

a month. That is everything from food to mortgage.

How much could you save?

Income: $4.5 million

Taxes: @23% $1 million

Expenses: $5000 a month $2.7 million

Max Savings: $800,000

Using the 4% rule that would give you about

$32,000 a year in retirement plus your social security which would be around

$2000 a month. That would give you less than $5000 a month in retirement. You

would have no money for romance, travel, or anything fun. This would be a

horrible retirement by any definition.

It is nearly impossible to save your way to

retirement. The numbers just don’t work. What you need to understand is that

you don’t have an expense problem, you have an income problem. You just don’t

make enough money.

Put the coupons down and read a book on how

to make more money. That is why I started investing in real estate. I realized

the system was flawed. I focused not on saving money but making more money.

That is what is effective.

article continues after advertisement

Number 2:

Thinking a job is

there to build wealth.

The middle class think that a job is a way

to build wealth. It is not. They think they are going to climb the corporate

ladder to success. This success story is so rare, it is not even worth

mentioning. Waiting for people to die, get old, retire, or get fired so you can

move up is futile and ineffective.

Why do people think they can do this?

Because when someone does do it, they publicize it as the norm.

I used to look up to Jack Welch of GE. I

wanted to be like him. The press promoted him and bragged about his $100 plus

million paychecks. They did not let you know that he had 150,000 employees that

were just barely surviving.

This is much like the casinos that when

someone wins $1 million, they promote it all over the place not mentioning the

other 10,000 people that were losing money at the exact same time in the exact

same casino.

Plus, imagine playing Monopoly and just

circling the board and collecting your $200 paycheck every time you passed go.

Would you ever win the game? No. To win the game, you can’t just depend on a

paycheck. You must buy income-producing assets such as rail roads, utilities,

and real estate. It is the same in real life.

Number 3:

Thinking high

school and college teach you about building wealth.

The sad truth is neither high school nor

college teach you anything about building wealth. They teach you how to get a

job and nothing more. That is what they were designed to do.

You are responsible for your financial

education. Jim Rohn put it this way. “Formal

education will make you a living, self-education will make you a fortune.”

Seventy percent of Americans never read a

non-fiction book after high school or college. This is a huge mistake. They

think they know everything, and they end up broke at 65.

You must read, listen, and attend seminars

and workshops if you are going to learn the rules of money and wealth.

Number 4:

They waste massive

amounts of money trying to impress others.

The “keeping up with the Joneses’” costs

the middle-class billions a year. Constantly upgrading their clothes, watches,

cars, and homes to impress people who don’t even care.

Remember this point: “Dance like no one is

watching. They aren’t.” This is very true. They just don’t care. They have

their own lives and problems to worry about. They don’t care what kind of car

you drive or where you live. Stop trying to impress others. It is a waste of

time and money.

article continues after advertisement

Number 5:

Buying toys first

and assets second.

The middle-class has it backwards. The say

this to themselves. “I will buy all the things I want first, and then I will

start saving and investing.” It doesn’t work. By the time they buy the clothes,

watches, cars, and houses, they are living paycheck to paycheck. There is no

money left over to save and invest.

The people who end up wealthy buy assets

first, and with the profit from these assets, they buy the toys.

I have never made a payment on my boat, Ferrari,

or beach house. My assets pay for them.

Number 6:

They fall victim

to lifestyle creep.

Do you remember in your 20s and 30s when

you made very little money and lived paycheck to paycheck? Of course. You

didn’t make much money, so it makes sense.

However, it is 20 years later, and you are

making 3 times as much but you are still living paycheck to paycheck. Where did

that other money go? Lifestyle creep.

When you got your first raise, you decided

to buy your first home and took on a mortgage way higher than your apartment

rent.

You got your second raise and now you

needed a nicer car. Maybe a BMW.

You got your third raise and now your kids

are not in the right school district, so you must buy a more expensive home in

a nicer subdivision.

Are you starting to see what’s happening?

Every time you get more money, you are spending it to improve your lifestyle

leaving you continually living paycheck to paycheck.

These 6 things combine to keep the

middle-class middle-class. It is a sad situation but can be solved fairly

easily by stopping the madness.

Be aware, I did every one of these things

at one time or another and I turned my life around very quickly by stopping.

You can too.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/11/middle-class.jpg5001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-11-20 04:27:552023-11-20 04:39:55Why the Middle Class Tend to Stay Middle Class

The other day, you received an invitation to join me and my associate, Bruce Mack, for a LIVE webinar where you’ll learn how to solve that giant tax and asset protection problem facing ALL Real Estate Investors. Bruce is the perfect person to share this insight as he is a Licensed Financial Advisor, national speaker, author, and real estate investor.

Today, I want to give you one more nugget about this strategy.

They say that “the only guarantees in life are death and taxes.” Well medical advances have been able to postpone death for a while.

But what about overpaying taxes? Can you postpone them too?

Actually, Bruce says you can. (In fact, Bruce adds that you can defer most of your tax liability in perpetuity.) They have a solution that completely solves that giant tax problem for ALL Real Estate Investors.

Using their Trust, you cannot be classified as a Real Estate Dealer. Real Estate Dealers are taxed at ordinary income rates, plus self-employment @ 15.3%, Medicare Surtax & AMT. That could easily be over 50% of your profits. OUCH!!

This strategy uses the tax code to legally keep most of the money you were going to send to Uncle Sam this year in your bank account and is 100% IRS compliant.

On this critical must-attend webinar, Bruce will also reveal how you can protect yourself financially — right now — in today’s troubled and litigious times with bulletproof asset protection.

Reserve Your Seat here now! November 14, 2023 5pm PST / 6pm MST / 7pm CST/ 8pm EST

P.S.: Make sure you stay until the end of the webinar! Bruce will tell you how you can get a complimentary 1 on 1 consultation ($250 value).

P.P.S.: With this proprietary Trust Brice states you will also receive absolute asset protection for yourself and your business. LLCs can easily be pierced.

Join us for this LIVE webinar and learn if you qualify to defer a good portion of your tax burden … LEGALLY, without having to move to another country to do so. Don’t miss this informative webinar.

STOP Overpaying on Your Taxes and Get Absolute Asset Protection

Hello,

Real Estate Investors save 78% – 90% or more on their annual taxes and you can too!

Did I get your attention yet?

We have a solution that completely solves that giant tax problem for ALL Real Estate Investors.

In today’s real estate market, the only constant is volatile change…Your business is in a constant state of flux. Yet, there is one thing that’s not changing….Uncle Sam is still demanding his tax payments on your rental income and capital gains from your REI business including Flippers who get classified as Real Estate Dealers.

Using our Trust, you cannot be classified as a Real Estate Dealer. Real Estate Dealers are taxed at ordinary income rates, plus self-employment @ 15.3%, Medicare Surtax & AMT. That could easily be over 50% of your profits. OUCH!!

There is a new explosion of lawsuits because of the economy and people are getting desperate!

LLCs don’t protect you (in fact over 46% of the time when litigated the corporate veil is pierced) my special guest and nationally known speaker, author and real estate investor, Bruce Mack, is going to show you a superior solution to keep you lien, levy and judgment proof.

On this upcoming, MUST attend, LIVE webinar for your REI BUSINESS SURVIVAL, you’re going to get the solutions to both problems (you will be amazed at how simple the solution is!)…

Join me and my good friend, Licensed Financial Advisor Bruce Mack, for this LIVE Webinar.

Reserve Your Seat here now! November 14, 2023 5pm PST / 6pm MST / 7pm CST/ 8pm EST

Make sure you stay until the end of the webinar! Bruce will tell you how you can get a complimentary 1 on 1 consultation ($250 value) just for attending the webinar!

See you on the upcoming MUST attend webinar!

To Your Success!

Linda Pliagas Publisher/Editor/Investor

Realty411.com and REIWealthmag.com

P.S.: Join us for this LIVE webinar and learn if you qualify to defer 78% to 90% or more of your tax burden in perpetuity … LEGALLY, and without having to move to another country to do so!

-Advertisement-

Expand Your Knowledge of REI in NYC

Network and Learn in Manhattan

This special event will help investors gain specialized insight and knowledge about real estate investing, entrepreneurship, finance, and other life-changing subjects. The information shared on this day could catapult your real estate portfolio to new levels of success.

Are you ready to Grow Your Real Estate Business in the East Coast?

This is Your Chance to meet TOP Leaders in REI, Local & National Experts. Learn from Leaders & Industry Pros, NON-Stop Tips for Real Estate Success, Bring Lots of Business Cards!

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/11/ASSET-PROTECTION.jpg5001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-11-07 03:37:142023-11-07 04:19:33STOP Overpaying on Your Taxes and Get Absolute Asset Protection

As we welcome Fall and the near close of yet another year, we want to take an opportunity to thank you for being a part of our network.

We hope you had the opportunity to connect in person with us this year. So far, we have reached thousands of people in our database throughout the nation at our in-person events.

For those who were unable to attend one of our many in-person events, we want to give you the opportunity to connect and learn with us.

Investors, be sure to register for our new VIRTUAL event, which is conducted LIVE and in real time. On this new VIRTUAL Investor’s Summit, guests will have the opportunity to learn directly with top real estate leaders.

Plus, this educational event gives our guests the opportunity to ask questions after each presentation!

Be sure to attend this important online event where experienced educators will share their knowledge and strategies for a better understanding of the current real estate market. Gain the insight to implement a game plan for real estate success. Be sure to register below.

-Advertisement-

Expand Your Knowledge of REI in NYC

Network and Learn in Manhattan

This special event will help investors gain specialized insight and knowledge about real estate investing, entrepreneurship, finance, and other life-changing subjects. The information shared on this day could catapult your real estate portfolio to new levels of success.

Are you ready to Grow Your Real Estate Business in the East Coast?

This is Your Chance to meet TOP Leaders in REI, Local & National Experts. Learn from Leaders & Industry Pros, NON-Stop Tips for Real Estate Success, Bring Lots of Business Cards!

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/10/Realty411-new-events.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-10-30 06:28:362023-10-30 06:28:41New Events – Online and In Person

Realty411.com has assisted companies of all sizes expand their visibility and grow their business since 2007.

Contact us for a complimentary marketing session: CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/10/featured-image-UCC.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-10-27 04:35:232023-10-27 04:36:05Bridge Funding – $1M to $7M Available

A blended rate is a combination of interest rates on multiple loans for an individual or household and calculated as if they were just one rate.

Those very fortunate mortgage borrowers with existing 1st mortgage rates at or below 3% or 4% might be hesitant to choose a new cash-out refinance 1st loan to pay off their rising unpaid consumer debts that may vary between 10% and 30%+ each.

More than 40% of all U.S. mortgage borrowers funded their purchase or refinance loan in either 2020 or 2021 when rates were at or near historical lows, according to data published by Black Knight. Many homeowners don’t want to lose their record low rate by refinancing the mortgage debt or selling, which is akin to a lock-in effect.

article continues after advertisement

A blended rate analysis for an existing debt comparison to a new cash-out 1st or 2nd mortgage or HELOC (Home Equity Line of Credit) can be simplified by comparing the existing monthly debt obligations for the consumer with a proposed new cash-out mortgage or HELOC that pays off all of the existing mortgage and/or non-mortgage debt.

For example, the Jacksons have a $400,000 1st mortgage that has a 3% fixed rate for 30 years. They funded the loan near the all-time record low time period in early 2021 and now have just under 28 years remaining on the loan.

The Jacksons also have $50,000 in credit card debt that’s compounding at close to 30% and two used car loans which combine for another $50,000 that average near 12%. To simplify this calculation, I used the exact same balances for an easier interest rate calculation estimate of 21% (30% + 12% = 42% / 2 = 21%).

Let’s now add the $400,000 mortgage at 3% to the $100,000 in credit card and automobile loan debt at 21% for a grand total of $500,000. Four-fifths ($400,000) of the Jacksons’ monthly debt is at 3% while one-fifth ($100,000) is at 21%.

● $400,000 mortgage balance: 3% rate ● $50,000 credit card balances: 30% rate ● $50,000 automobile loan balances: 12% rate ● New blended interest rate for all debt: 6.6%

The Jacksons’ blended interest rate in this example is 6.6% for all of their monthly consumer debt when including their mortgage, credit card, and car payments.

The Jacksons explore their HELOC (Home Equity Line of Credit) options that would be recorded in second position behind their existing 3% fixed rate 30-year mortgage that they don’t want to lose.

As of October 18, 2023, the current average HELOC interest rate was 9.02 percent, as per Bankrate (all rates and fees are subject to change). Rates, fees, and APRs (Annual Percentage Rate) are all over the place, depending upon the lender, borrower’s creditworthiness, and daily financial market trends that may rise or fall.

With this HELOC rate estimate provided, we will explore both a 9% and 10% HELOC rate to get the Jacksons $100,000 to pay off their 30% credit card and 12% automobile loan rates.

● $400,000 mortgage balance: 3% rate ● A new $100,000 HELOC: 9% rate ● New blended interest rate for all debt: 4.2%

● $400,000 mortgage balance: 3% rate ● A new $100,000 HELOC: 10% rate ● New blended interest rate for all debt: 4.4%

Either way, a new HELOC that’s used to pay off consumer debt may decrease the total monthly blended rate for all monthly debt by at least 2% (6.6% blended rate – 4.2% or 4.4% blended rate = 2.4% to 2.2% blended rate improvement).

article continues after advertisement

My best HELOC programs (10-year interest only, 20-year amortizing) may be interest-only for the first 10 years while later adjusting to fully amortizing with principal and interest for a total loan term of 30 years. If I calculate these HELOC rates as interest-only for the first 10 years, the total blended rate payments would actually be even better.

To check your actual current blended rate debt as well as your potential future blended rate if you welcome a new HELOC loan, please enter your own consumer debt data (loan amount, rate, and number of individual loans) here to find out: Blended Rate Calculator.

The average borrower is in their home for about seven years, not 30 years. This is also about the average time period that a borrower holds one or two mortgage loans on their property before they later sell or refinance at a hopefully lower rate.

Snowballing or Compounding Credit Card Debt Examples

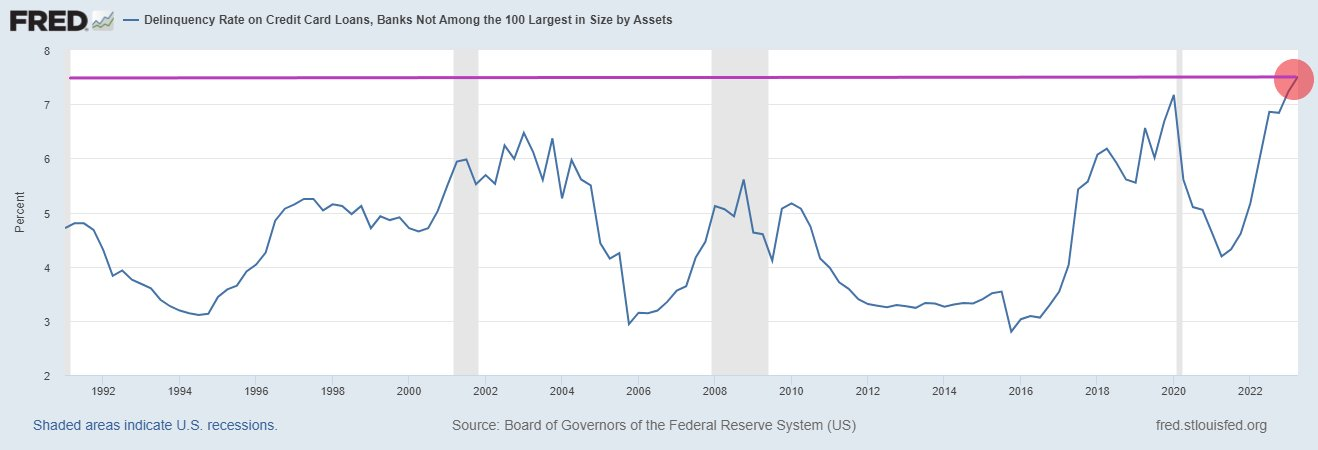

Credit card delinquency rates at small banks reached 7.51%, the highest level ever recorded according to the St. Louis Fed.

Average credit card rates surpassed 28% nationwide recently. However, retail store credit cards are now closer to 30%. By comparison, credit card rates averaged closer to 12% back in 2008.

In the 3rd quarter of 2023, new credit card delinquencies reached 7.2% according to the New York Fed Consumer Credit Panel and Equifax.

The average annual percentage rate (APR) for merchant cards, which many holiday shoppers will be using online or at nearby shopping malls, just hit 28.93%. This is a new all-time record, up from 26.72% in 2022, according to Bankrate.

Credit Card Debt Payoff Examples

Now, let’s compare how much time and interest is required to pay off a credit card debt balance of $20,000.

Many credit card issuers may have different minimum payment allowances which may vary from a minimal fixed dollar amount up to the interest plus 1% of the unpaid principal balance that’s paid monthly.

For example, let’s start with minimum payment example #1 that includes just interest-only with no principal paydown each month:

Credit card payment #1: Unpaid credit card balance: $20,000 Interest rate: 28.93% Annual interest paid for one year: $5,786 ($20,000 x 28.93%) Monthly interest-only payments: $482.17 ($5,786/12 months)

If the borrower just pays the absolute minimum interest-only payment of $482.17 per month, it will take 41 years and 7 months to pay off the unpaid balance. If so, this is 11 years and 7 months longer than a brand new 30-year fixed rate mortgage.

The total interest paid by the borrower over this time period would be $220,496.44 (11 times the original $20,000 balance). To verify yourself, here’s the specific credit card payment example #1 link on Calculator.net.

Credit card payment #2: Unpaid credit card balance: $20,000 Interest rate: 28.93% Payment option: Interest + 1% of principal balance Annual interest paid for one year: $5,786 ($20,000 x 28.93%) Monthly interest-only payments: $482.17 ($5,786/12 months) Payment of an extra $200 in principal ($20,000 x 1% = $200) Total minimum monthly payment (interest + 1% of principal): $682.17

The payment of the absolute minimum interest-only ($482.17/month) plus 1% of the original $20,000 unpaid principal amount ($200 in principal) for a grand total of $682.17 per month will take 4 years and 4 months to pay off the entire balance in full. The total interest paid will be $15,134.49. To confirm yourself, here’s the specific link for credit card payment example #2 on Calculator.net.

Student Loan Debt

U.S. student loan balance: $1.8 trillion (fourth quarter of 2023)

Just 500,000 borrowers out of 43.5 million student loan borrowers, a 1.15% payment rate, were paying on time prior to the October 1, 2023 payment restart date. Many of these average $500+ per month student loans are adjustable and are likely to increase over time, sadly.

The average federal student loan debt is $37,338 per borrower. Private student loan debt averages $54,921 per borrower. Twenty years after entering school, 50% of the student loan borrowers still owe more than $20,000 each on outstanding loan balances, according to the Education Data Initiative (May 22, 2023).

Just 90 days after the October 1, 2023 student loan payment restart date, any ongoing delinquent student loan payments may be shared with the credit bureaus as early as January 1, 2024. If so, the FICO credit scores for delinquent student loan borrowers may begin to fall as their borrowing costs for future loans may rise as well.

Worsening Automobile Loan Sector

In September 2023, Fitch Ratings reported that 6.11% of automobile loan borrowers were at least 60 days late on their payments. This is the highest delinquency rate since the early 1990s.

While a 30-day late can often be a mistake by a borrower who forgot about their payment, a 60-day later indicates possible significant financial challenges. Few people want their car repossessed, so it’s usually a top priority monthly debt obligation that a borrower will focus on to get paid each month. Without a car, how does someone get to school, work, or to visit friends and family if they don’t have access to affordable and convenient public transportation nearby?

Average subprime car loan rates are reaching the 17% – 22% loan rate range.

The percentage of subprime auto borrowers who are 60+ days past due on loans hit an all-time record high of 6.1% in September (#2 highest: 1994 – 6.0%; and #3 highest: 2008: 5.0%).

The average new car price is now higher than $48,000.

Average new car payment rates are near $750/month and the average student loan payment is just over $500/month. For consumers with both forms of debt, they are paying close to $1,250 per month for just their car and student loan while not counting insurance, gasoline, or maintenance for the car.

The average used car price now is $30,700 as compared with an average used car price just under $8,000 back in 2008.

The average loan-to-value ratio for a used car is 125% LTV (no money down + taxes, license, registration, warranty, other fees, and declining value over time).

There are now 20,000 car repossessions PER DAY (600,000 per month) while rising exponentially each consecutive month. If the same pace of rising and compounding car repos continues onward, there might be upwards of one million car repos PER MONTH in 2024 (yes, one million per month).

There are approximately 100 million car loans across our nation. However, there are an estimated 276 million automobiles nationwide, so the car loan-to-total cars nationwide ratio is just over 36% (100 million/276 million = 36.23%).

Moody’s recently warned about potential automobile loan and credit card default rates as high as 9% to 10% in 2024. If so, this might be equivalent to nine to 10 million car loan defaults or repos out of the total 100 million car loans. If proven true, a nine to 10 million car loan default rate would make the one million car repossession projection for 2024 seem much too conservative and only a fraction of how bad the car delinquency numbers may reach.

California Mortgages: 50-Year Analysis

Between April 1971 and September 2022, the average 30-year fixed mortgage rate was 7.76%. Today’s 30-year fixed rates for consumers are fairly close to this historical 50-year average, depending upon their creditworthiness and whether it’s a conventional, FHA, VA, or non-QM type of loan.

The 30-year fixed rate peaked near 18.6% in October 1981. In January 2022, some 30-year fixed rates temporarily reached the high 1% to low 2% rate range.

Over the past 50 years, the typical California homebuyer spent 43% of their income on house payments. Today, the average homeowner spends closer to 58% to65%+ of their monthly gross income on mortgage payments (principal, interest, taxes, insurance, and HOA, if applicable). After paying state and federal income taxes, many California homeowners are more likely paying closer to 70% to 80% of their net monthly income towards their monthly housing debt.

The median price of a California home over the past 50 years was $331,000. In September 2023, the median statewide price reached $843,340, according to the California Association of Realtors. This is almost more than double the median national home sales price that hit $431,000, as per the St. Louis Fed.

Over the past 50 years, the average monthly mortgage payment was $1,627 at 80% LTV with 20% cash down. In 2022, the average mortgage payment reached $4,043/month, a 148% increase.

In the fourth quarter of 2023, let’s review a potential new mortgage payment for a median home price in California that’s near $840,000:

Down payment percentage amount: 20% down payment (average is 6% down nationwide) Down payment dollar amount: $168,000 New loan amount (80% LTV): $672,000 30-year fixed mortgage rate: 8% (example only, subject to change) Monthly mortgage payment: $4,930.90 (principal and interest)

This example above does not include any monthly property taxes, insurance, or homeowners association (HOA) payments, if applicable.

The average household income for Californians over the past 50 years was $45,700. Today, the average income is closer to $84,000. This 84% increase in income isn’t enough to cover the 148% increase in mortgage payments, sadly.

A 20% down payment over the past half century for Californians was $66,000. In 2023, the average down payment increased to $168,000, which is a whopping $102,000 down payment increase.

Finding more affordable monthly blended rate payment options are what you should focus on these days as we all see consumer debt balances and interest rates either heading towards or surpassing all-time historic highs.

Please contact me today for a FREE blended rate analysis of your personal debt. You may be pleasantly surprised to learn how I can help reduce your overall blended rate, monthly payments, and possibly eliminate years or decades’ worth of extra debt payments.

Rick Tobin

Rick Tobin has worked in the real estate, financial, investment, and writing fields for the past 30+ years. He’s held eight (8) different real estate, securities, and mortgage brokerage licenses to date and is a graduate of the University of Southern California. He provides creative residential and commercial mortgage solutions for clients across the nation. He’s also written college textbooks and real estate licensing courses in most states for the two largest real estate publishers in the nation; the oldest real estate school in California; and the first online real estate school in California. Please visit his website at Realloans.com for financing options and his new investment group at So-Cal Real Estate Investors for more details.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/10/blended-rate.jpg5001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-10-26 05:50:182023-10-27 02:41:31What’s Your Blended Debt Rate?