By Tamera Aragon

Today, I wanted to share one message – Don’t Quit! That’s it. Don’t Give up! Wherever you’re at, whatever you are doing, If you have a dream or a goal and a life that just might seem too hard today… I am writing to tell you – Don’t quit!

Please enjoy the five-minute excerpt from the movie, ‘Facing the Giants’, it’s a piece of inspiration for anyone that is in the real estate investing game.

ADVERTISEMENT

In this video, a football coach teaches a valuable lesson about the limits we place on ourselves. And how important it is for you to NEVER GIVE UP as others watch you, as a leader.

Have you ever felt…. “I’m successful at my day job, but I’m failing at my new venture…” Then you will want to learn this mindset reset tip offered by my friend Doug.

“Sam had always been pretty good at most things she attempted, she was also great at her job, so when she was introduced to a money making opportunity, she figured ‘why not?’”

After investing a lot of time and money, Sam still wasn’t seeing the rewards she felt she’d been promised by the promoter. She said she knew there were other people that were creating success following the same things she’d learned, so she’d concluded that she must not be cut out for it. “I’d better just quit, I’ll never get the hang of this, I’m a failure” she complained.

I invited her to consider shifting her perspective on the matter. “Rather than assuming you’re a failure, would it be more correct to say that you’re a person with many successes under your belt who hasn’t yet mastered this particular skill?” She hesitated, “uh, yeah I guess that’s right.”

I could see the gears turning, so I went on, “and what would happen if rather than assuming you’re failing at this new venture, you decided your results were just feedback telling you what changes you need to make.” “What do you mean?”, she asked.

ADVERTISEMENT

I went on, “have you ever slipped on an icy sidewalk before?” “Yes, I’ve done that” she said sheepishly. I continued, “So did you conclude you’d failed at walking and that because of that you yourself were a failure so you should just probably hang the towel up on everything?” “Of course not, that would be silly,” she laughed.

“When you’re right, you’re right,” I smiled. “Whether you realize it or not, you implemented the feedback you got from the ice. You thought, hey, there’s slippery ice on the sidewalk and adjusted how you walked. Perhaps you stepped more carefully. Maybe you grabbed some sand or salt and spread that over the ice. Maybe you got off the sidewalk and walked around the ice. The point is, you changed what you were doing and successfully got to where you were going.”

Armed with this new perspective, Sam proceeded to pay careful attention to what she was doing and tracked her results. She then considered what things she could adjust that would affect her outcome, and get her the result she wanted. By implementing one change at a time to and tracking her activities, eventually, she figured out what tweaks she needed to make to achieve her outcome.

Remember, there is no failure, there’s only feedback.” ~ Doug O

In closing, here are some powerful words from the man whose life displayed this “don’t quit” attitude wholeheartedly…. Winston Churchill left us with these words of wisdom:

“Never give in. Never give in. Never, never, never, never—in nothing, great or small, large or petty—never give in, except to convictions of honor and good sense. Never yield to force. Never yield to the apparently overwhelming might of the enemy.”

Be Inspired…..

Tamera Aragon

Tamera Aragon is a professional online entrepreneur and has bought and sold over 300 properties, establishing her as an expert in the real estate investing field. Since 2003, she has purchased over 10 million dollars in real estate and currently holds properties all over the world. Tamera’s focus is on the booming Foreclosure market, buying Pre-foreclosures, REOs and Short Sales. Tamera who is a noted Author, Success Trainer, Speaker & Coach, shows her passion for helping others with the 17 websites she has created and several specialized products to support fellow investors throughout the world. When Tamara is not busy running her website, she is very involved with her Fiji joint ventures and investments. Tamera Aragon is one of the few trainers and coaches who is really “doing it” successfully in today’s market. Tamera’s experience has earned her a solid reputation in the industry as well as the respect and friendship of many of the top national real estate investment and internet marketing experts. Tamera Aragon believes her success has garnered her the financial freedom to fully enjoy her marriage and spend quality time with her children.

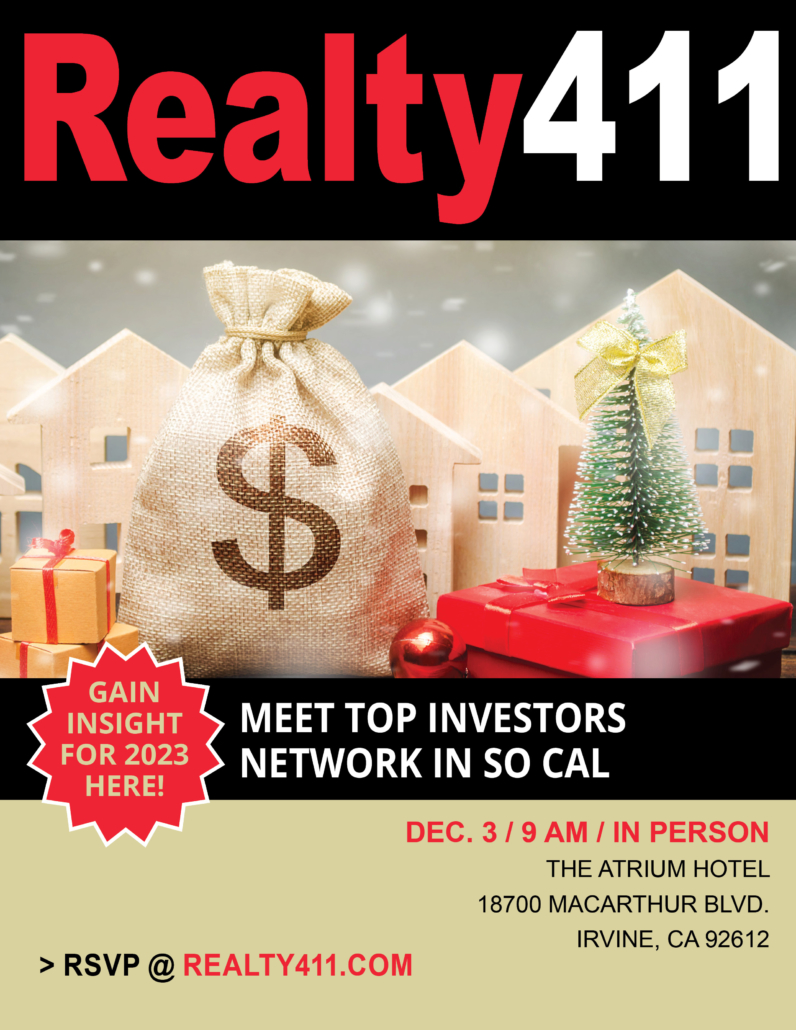

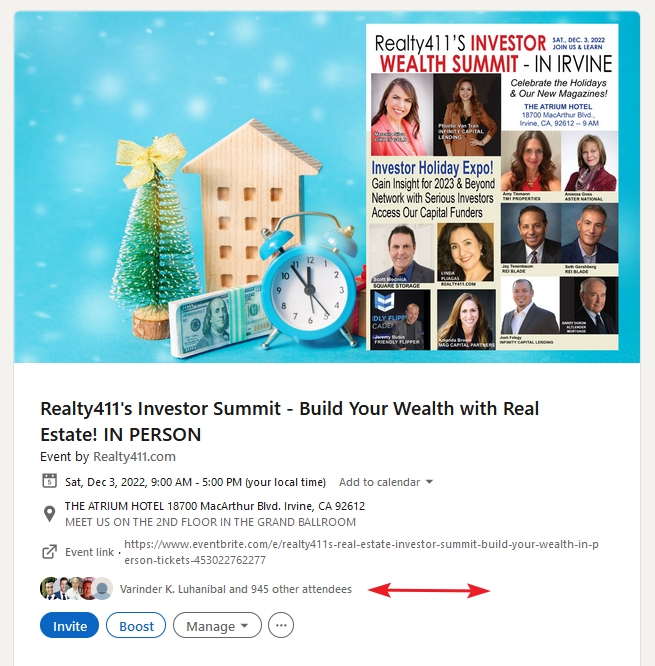

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.