It’s time for our educational Virtual Investing Summit uniting readers for an amazing day.

Investors, don’t forget to register for our NEW Virtual Investing Summit on Friday, April 26th, from 9 AM to 2 PM PT (East coast time: 12 PM to 5 PM ET) and Saturday, April 27th, from 9 AM to 2 PM PT as well.

Guests can join Realty411‘s complimentary VIRTUAL Investing Summit and learn from experts sharing important knowledge, strategies and insight.

Realty411 will virtually unite some of the most successful, knowledgeable and savvy investors in the REI (Real Estate Investing) industry to help our readers make educated and informed decisions.

Join us for an amazing day of real estate education. Every online event we produce is unique, so be sure to reserve this day for REI learning at its best.

Some of our special educators are listed below, more experts to follow.

“Without effort, you cannot be prosperous. Though the land be good, you cannot have an abundant crop without cultivation.” – Plato

article continues after advertisement

Real Estate As a Path To Wealth & Freedom

Forbes magazine lists the top 400 wealthiest people every September. In September 2007, 40 of the 400 people on that list made their billions specifically in real estate. Many of these people started with nothing, some immigrants even, to move up into this category. Real estate is definitely a path to be seriously considered in building your wealth. Did you know that most of those 40 billionaire real estate investors are only doing their real estate part time? And do you realize they can run their real estate investing business from anywhere in the world?

Freedom… Just the sound of that word brings a smile to my face. Real Estate investing offers you the freedom to make your own choices about how and where you spend your time along with who you spend it with. Financial and time freedom is definitely something successful real estate investors enjoy.But what about the risks you say? Of course for every “tit” there is a “tat”, for every high a low, for every good a bad. Yes, unfortunately like any entrepreneurial venture, there are risks. My husband owns a retail store and he risks every day that someone is going to trip and fall and sue him. He risks that he may not sell enough to pay his bills, etc. I think you get the point. However there are steps you can take to minimize your risks and maximize your profits.

Top 7 Tips To Minimize Your Risk & Maximize Your Profits

Rule #1 – You Do Not Need To Re-Invent “The REI Wheel”

You will need to get training and have a mentor or coach, (or maybe several), in order to succeed. Even the best athletes in the world have a coach. Why? Because a coach will keep you on track. Don’t try to do it on your own. That school of hard knocks is going to cost you way more than good training and an experienced coach. I believe this to be the first step in minimizing your risks and maximizing your profits.

Rule #2 – Do Your Due Diligence (or as I say, “Do the Due”)

Would you buy a car without checking the engine, tires, brakes, or interior? Would you marry someone without learning all you can about them and knowing their flaws and good things before you take the plunge? I hope not!! Then why do so many real estate “investors” buy a property without doing the proper due diligence before they get into a contract?Answer: Many simply lack the knowledge of what to look for in a property when considering it for investment purposes. In other words, you don’t know… what you don’t know, right? So here’s what you need to know. Before you ever buy a piece of real estate you should check it out from top to bottom so you know exactly what you are getting into. A little bit of work upfront will save you huge headaches and money down the road.

article continues after advertisement

People often ask me, “What should I look for before committing to buy a property?” There are two ways to make money in real estate. If the property is going to supply these profits for you, you would want to consider it.

When the property brings you cash flow from monthly rents while also appreciating.

When you make a profit re-selling the property through appreciation.

Now keep in mind, you can profit from appreciation two ways.

Market appreciation – the economy is causing properties to increase in value.

Forced appreciation – when you either buy property cheaper than what you can resell it for or you can do some improvements to increase the value more than what you spend.

Here are Three Most Important Questions I ask myself before I consider a property for investing?

Would we buy it for ourselves?

Would we want to tell our friends and family?

Is this a good deal for other real estate investors?

The most important outcome to consider is if the answer to this question is yes, “Will my money put into this property make me more money?”I call what I do real estate “investing”, not real estate “divesting”. You will always want to do the same. How do you know if it is going to make money? You do your due diligence before you commit to buy any property. Of course, as you know, there are never any guarantees in life.

However, if you have certain criteria every property needs to meet in order to profit and how to evaluate a property for those qualities, the likelihood that you will succeed are much greater. It’s very easy to get caught up in wanting to help people if they need to sell their house. Or you may just personally think a property is good looking. But those are not the only reasons you would want to buy. To avoid getting emotionally involved in a property purchase, I have created a due diligence checklist. I have provided a tool that has saved many people from both passing on deals they should take as well as taking deals they should pass.

I took from my own trials and errors & created a checklist – The Real Estate Investing “Before You Commit” Due Diligence Checklist. Keep in mind every one of mine or your personal due diligence items on that “checklist” do not need to be followed on every deal you consider. However, it’s a great list to follow and assure you have remembered to consider all that can affect the outcome of your purchase. Your due diligence makes all the difference on whether your purchase of property brings you a profit or a loss.

Rule #3 – Invest Using the Strategies that Make Sense and the Location That Makes Sense for the Current Market Conditions

I always say invest where it makes sense and dollars. You don’t need to invest in your home town, because you live there…nor do you need to go all over the country investing everywhere else. Do your homework and invest in locations that align with the real estate investing niche you chose using the strategy that is a fit.

For example, three years ago I was investing nationally in pre-construction in most strong appreciating markets. That strategy made sense at the time. It would not make sense in a depreciating market.

Today I live in a town that has been on the top 5 most foreclosures list for over 2 years. Why would I need to invest nationally when there are more than enough leads right in my own backyard? Where to invest varies depending on the location of the investment as well as market timing.

My investment choices change as often as the market does. Being sensitive and aware of changing market trends is helpful to know where to invest and the most profitable strategy to follow. The last four rules of the “Top 7 Tips To Minimize Your Risk & Maximize Your Profits” will be concluded in Part 2.

Tamera Aragon

Tamera Aragon is a professional online entrepreneur and has bought and sold over 300 properties, establishing her as an expert in the real estate investing field. Since 2003, she has purchased over 10 million dollars in real estate and currently holds properties all over the world. Tamera’s focus is on the booming Foreclosure market, buying Pre-foreclosures, REOs and Short Sales. Tamera who is a noted Author, Success Trainer, Speaker & Coach, shows her passion for helping others with the 17 websites she has created and several specialized products to support fellow investors throughout the world. When Tamara is not busy running her website, she is very involved with her Fiji joint ventures and investments. Tamera Aragon is one of the few trainers and coaches who is really “doing it” successfully in today’s market. Tamera’s experience has earned her a solid reputation in the industry as well as the respect and friendship of many of the top national real estate investment and internet marketing experts. Tamera Aragon believes her success has garnered her the financial freedom to fully enjoy her marriage and spend quality time with her children.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/04/profit.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-04-16 05:07:072024-04-16 05:07:09Tips To Minimize Your Risk & Maximize Your Profits (Part 1)

It’s no surprise to hear that investing in real estate is one of the best ways to build wealth and gain financial freedom. So many successful people have figured out how to make millions in real estate. When you work hard, constantly aim to learn and grow, and network efficiently, you can also make millions in real estate. Unfortunately, many people go into real estate expecting to make a ton of money without putting in the work. If you do not go about it correctly, you can lose money in real estate instead of gaining it.

Tips for How to Make Millions in Real Estate Investing

Focus on One Method at a Time

There are so many different methods to make millions in real estate investing. But you can’t do it if you are spread too thin. You have to master one thing and get good at it if you want to make money doing it. It’s also important to focus on one method so you can fully understand your goals. If you have multiple methods happening simultaneously, your goals could start to get a little murky.

Not to mention, trying to do everything at once can lead to costly mistakes. You simply won’t have the time, energy, or knowledge to follow through on every avenue.

Many people who are just starting off in real estate investing choose to do either real estate wholesaling or invest in rental properties. Real estate wholesaling is great for beginners because it requires very little to no capital to get started. It can be a little tricky at first getting the connections for your first sale, but it’s an excellent way to get your feet wet with little risk on your end. Investing in rental properties is another great investment when starting off because it’s generally pretty simple and, if done correctly, will result in a steady flow of cash each month. That cash can be reinvested into more real estate investments. As you continue to profit and buy more properties, your portfolio will grow, and you will be that much closing to being able to make millions in real estate.

article continues after advertisement

Establish Your Goals

Once you have narrowed down the method of real estate investing you want to focus on, you must establish your goals. Consider questions like: What are your short-term goals? What are your long-term goals? What types of properties do you want to invest in? Without goals, you will never make it to becoming a millionaire through real estate. When you know what you want out of your investments and your career, you can begin to make smart business choices that align with your goals. You will have an easier time choosing the investments that help you achieve success. You’ll also have an easier time deciding what types of properties you want to invest in, how you plan to finance them, and how to manage them properly.

Break Down Your Goals Into Steps

Of course, it’s essential to think big when setting your personal and professional goals. You also need to be realistic on what you can accomplish based on your experience, capital, and time. You cannot make millions in real estate overnight. It will take a lot of time and hard work, and you need to be realistic about that with yourself. Now that you’ve established your short-term goal start there. Break that goal down into smaller steps until you reach something actionable that you can do today to get started. Consider how long each step will take until you fully complete your short-term goal. As you complete this step, you may realize that you need to go back and set a new goal. That is absolutely fine and a significant first step toward success. As you begin to work through these steps, you may find that you need to edit or change some.

Don’t Invest All of Your Money on Day One

It can be exciting to get started in real estate investment. However, you should not put all of your money into your very first investment. You are at your least experienced that you will ever be, and you’ll likely make a few mistakes. These mistakes will help you grow as an investor and eventually make millions in real estate, but not if you put all of your money into them right away. The best thing you can do for yourself is to start small and make less expensive investments like single-family homes to start. Once you gain more knowledge, experience, and connections, you can begin to make larger investments.

article continues after advertisement

Constantly Educate Yourself

The biggest thing you can do for yourself when learning how to make millions in real estate investing is to educate yourself. Learn as much as you can from every experience and every connection you make. Ask lots of questions to others in the field. Consider getting a mentor who aligns with your goals to help you quickly learn how to become as successful as they are. Read books and articles, watch videos, and listen to podcasts. Constantly learning about everything new in real estate will quickly put you ahead of your competition and have you making millions years before anyone else.

Take Action

Education is nothing without action. You can spend years learning everything from every book and article and person you talk to, but it means nothing if you don’t put it into practice. Getting started will be scary, but you’ll never know if you can succeed unless you try. All of the knowledge you gained will help you get started. From there, you’ll gain invaluable experience that will teach you more than any book ever could.

Start an Emergency Fund

Ideally, you will reach a point in your career where you can trust all of your income streams to support you. When you are just starting, you don’t have that type of protection. Try to save at least six months’ worth of expenses in a savings account if anything happens, and you no longer have your income. You never know when something might happen. You may have to make extensive repairs on a property that cost a lot of money. Sometimes your properties may sit vacant and have no income. In situations like these, it’s crucial to be covered financially.

Utilize Mortgage Loans

Many people assume that you need to have a lot of money to get started investing in real estate. You don’t have to be rich to make millions in real estate; you just have to be smart. While there certainly are very wealthy people who do very well in real estate, it isn’t a necessity when you are just getting started.

Many people utilize mortgage loans when buying their first income property. How this works if you take out a loan to pay for a property. When you get tenants, they will pay you enough to cover the loan payments while still making a profit entirely. Utilizing loans allows you to buy a larger property and make more money. Once you start profiting off of that property, you can continue investing in others.

Use Data to Your Advantage

If you understand how to pull and read data and analytics, you have a greater chance of making millions in real estate. Understanding how to track and read numbers is essential for your success. When looking at potential properties, you should pull reports from different investment software and take the time to analyze how profitable those properties could potentially be. Once you get started, being able to analyze the reports from your real estate accounting software will help you make better decisions and understand your profits.

Utilize Appreciation for Profit

While not as guaranteed as profit from tenants, investors can make a lot of money by investing in properties that they predict will appreciate. When a neighborhood is up and coming, and you buy a property for a reasonably low value, rent from your tenants will be low for a few years. Once the neighborhood has become more in-demand and popular, you can start raising the rent. Because property values are high in the area, you won’t detract potential tenants by raising your rent. Plus, if you decide to sell the property, you’ll make a nice profit.

If it’s not an up-and-coming area, there are still things you can do to increase the value of your property and charge more in rent. Making small cosmetic changes and improvements with your profits can result in you making more money.

Build Your Real Estate Team

If you are looking to make millions in real estate, you cannot do it alone. You have to prioritize teamwork and trust in others to help you succeed. There are many different aspects of real estate that plenty of people specialize in. As a beginner in real estate investing, it’s even more critical that you find a real estate team you can trust. These people can help you avoid costly mistakes and succeed in real estate.

The following are some of the most important people that you will want on your real estate team:

Accountant

Accountability Partner or Group

Administrative Assistant

Attorney

Bookkeeper

Cleaning Company

Electrician

General Contractor

Handyman

Hard Money Lender

Inspector

Insurance Agent

Leasing Agent

Marketing Coordinator

Mentor

Pest Control Company

Private Money Lender or Equity Partner

Property Manager

Title Company

While you certainly won’t need every single one of the people on this list right away, you should start making connections now for the day that you will need them. Not every person you add to your team needs to be a permanent member. As you learn and grow, many of these people will change, but it’s essential to have them to start.

Summary

Making money through real estate investing is not an easy thing to do. If you take the time to learn as much as you can, set realistic goals, specialize in a specific method, and utilize your connections, you can make millions in real estate. To fully unlock your potential, check out our site and learn how to gain financial freedom through real estate investments.

Joe Arias and his partners have flipped hundreds of properties in the Southern California Region. He has developed cutting-edge systems to simplify and scale the entire remodel process that can easily be applied to flipping, rentals, wholesaling, and other passive income strategies. More recently, Joe founded a real estate investing education company called RealSuccess Investments, allowing him to share his tools and systems with hundreds of up-and-coming investors.

RealSuccess is focused on education on flipping, rentals, passive income, and wholesaling.

Joe is also a best-selling author. He has written 4 books: Finding your RealSuccess, First Steps to Flipping, R stands for Rentals and Retirement, and Wholesaling Real Estate.

“I came from Argentina when I was 20, I am 40 years old now. I didn’t know anyone, I am CERO generation, usually people say, I am first or second generation but I was the one that crossed the border, no language, no friends, no family, no money, nothing, nada… If I can do it, anyone can.”

From a young latino immigrant to a celebrated real estate investor, Joe is a true testament to hard work and discipline. As an investor, he has made it his mission to help others achieve financial freedom while enjoying living a life of passion, fulfillment, and empowerment.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/04/real-estate-money.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-04-08 01:56:262024-04-08 01:56:28HOW TO MAKE MILLIONS IN REAL ESTATE

So here is a quick recap of Part 1 – Tax Deeds & Tax Lien Sales Investing: When homeowners fail to pay real estate (property) taxes, the government has the right to sell their property in a state “tax sale”. In a Tax Lien state, homeowners have an opportunity to pay back the amount owed within a specific time frame even after their property has been “sold” with interest to a real estate investor. Should homeowners miss the payment deadline, the investor becomes owner of the property at a great discount. In a Tax Deed state, investors bid for immediate ownership of a property or are eligible for the deed and ownership of the property after a redemption period passes. In Part 1 – Tax Deeds & Tax Lien Sales Investing I covered the descriptions of the different investing strategies as well as the rewards and the risks investing in tax liens vs. tax deeds.

Tax Deed Investing Process For Real Estate Investors

Now I am going to cover some of the steps you will need to go through as you go through the entire tax deed process and come out a winner with your real estate investment.

Obtain and Review a List

Obtaining a list of the properties that a county is going to auction at the next tax deed sale is the first thing you need to do. You should first of all find a website for the county and see if they have or will publish a list of their tax deed sales on their website.

Sometimes the county will send you a list two weeks prior to the auction for a minimal fee. You will also want to know how often they update the list prior to the auction. If it is possible to obtain this information in person and meet the people at the county office, it is better than by phone. The more people you personally know and the more questions you ask the better off you will be when you really may need help.

Once you obtain a list, they are usually fairly limited on the information they give about the property. Usually it lists Parcel number, name of owner, address of owner or property sometime both, amount of taxes owing.

You will also want to find out:

Date of next auction?

When and how do they publish the list and how you may obtain a copy? (Often they are required by state law to publish the list in a local newspaper by a certain date. Usually newspaper will have a copy or it is available online.)

What is the actual auction and bidding format?

Do they require bidders to register before the auction?

What is the registration process for bidders?

How your tax deed will be paid for at the end of the auction?

How the auction is conducted and rules about bidding?

article continues after advertisement

Initial List Screening

Most lists will have more properties than you can possibly research. You need to screen the list for the types of properties that you are interested in. Usually there is a code number, the county staff can explain to you, that indicates if a property is a single family home, a developed lot, commercial, residential, duplex, apartment, etc. This is the first step in screening the kind of properties that you have decided you are interested in.

Second is to find the properties that are in the part of the town you may have determined you are interested in.

Third you can screen by the value of the property and the amount you are willing to bid.

Most of this initial screening can be done from a basic list.

Additional information that you want to obtain about the property include what type of improvements are on the property i.e. building, utilities, landscaping, curb and gutters, etc. or is it just land. Also find out the assessor value for both the land and improvements. Take note of the taxes due and when they were last paid. If there is a house or any type of building on the property find out the size, year built, number and type or rooms and if possible find about any other special features the structure may have. Learn additional information about the neighborhood by looking at the houses next door or across the street and maybe even talking to neighbors.

With all of the above information you can narrow your list down to the few properties that you need to drive buy and check out.

Visit the Property

If at all possible, a personal visit to the property is essential. If you can’t do that, a visit via the internet, through different search sites is the next best thing. However nothing tells the whole truth better than visiting the property. What seems like a very nice house could turn out to be next to a crack house or a busy grocery store or on a very busy street. What sounds like a normal building lot may have a beautiful view. You need to screen your list down to a number of properties that you can take the time to go see, especially with tax deed sales.

To save time and money you need to organize on a map your drive-bys so that you can find and record information about the properties in a timely manner. There are many mapping programs available on the internet that you can put the address in, and they will automatically give you a route. When you drive by, the number one thing is to take a picture of the property for your files. You want to write down identifying features found in the picture in case you get them mixed up. You want to rate the house, note any problems and repairs that are needed and rate the neighborhood. Usually unless the property is vacant you should not approach the house or talk to anyone about it.

Some quick things to take note of are as follows:

Paint and roof condition

Broken windows, doors, cement

Underground or overhead utilities

Trees, shrubs, general landscaping

Condition of adjacent properties

Property accessibility

Discolored soil or dead vegetation

Traffic on the street

House vacant, lived in, for sale sign

Make sure to drive around the area looking for any industry or business that would distract from the desirability of the property. Also look for similar properties in the neighborhood that may be for sale and call the owner or real estate agent to find out the price and condition as a comparison for properties value. You can print out this checklist on a spreadsheet that you can fill out while you are in the neighborhood and attach the picture of the property too.

Once you have accomplished all of this research, you are now ready to narrow your list, to the final properties that you will bid for at the tax deed auction.

Check for Recorded Problems

Now is the time to return to the county offices. Go to the county clerk’s office to check if there are any liens on the few properties you now have on your list. Some counties make this process very easy by having the information available online once you have the parcel numbers and address of the property. If there are liens on the property make sure you get the name and contact information on the business of person placing the liens. You need to also check for mandatory deed restrictions on the property. In other words, find out what you can or can’t do or build on the property. You should also check for any government assessment that may be filed against the property.

article continues after advertisement

The last thing you need to check, as close to the actual auction as possible, is to see if there were any last-minute redemptions by homeowners that would have removed the property from the auction table. One of the most frustrating things about tax deed auctions is the fact that many people don’t want to lose their property and will somehow pay their taxes at the very last moment.

It is not uncommon for a tax deed sale to have 40 to 50 percent of the properties redeem at the last minute. We therefore recommend that you research twice as many properties as you think you can afford to buy because half of them may be redeemed the last day or hour before the auction takes place.

Attend the Auction

The basic work is now over the fun and hopefully reward begins. Go to the auction with a very specific plan and stick to your plan.

Usually, you should arrive about 30 minutes before the auction begins, so that you can register, check the final list that will be there for any last-minute redemptions of your properties, find a good seat where you can see what is happening and review the written or oral instructions that will be given. You may be surprised that there will probably be many people at the auction. Only half of them will actually bid while the rest of the people just come to watch.

There are many types of people at the auction who you will be able to quickly identify. The professional investors who have deep pockets and usually win whatever bid they participate in. The local investors who know the area and the properties around their home or offices and understand value, they are important to watch. The beginners who have no idea what is going on and of course YOU. At this point just smile, stick to your plan and bid amounts. Do not get emotionally involved with the bidding.

Purchasing and Maintaining Your Deed

If you are a successful bidder on a deed, you will need to be prepared to pay the full bid amount plus any fees and outstanding taxes. In some state or counties, you will only be required to pay a deposit of perhaps 10% with the balance due in 30 days. You need to make sure that you have talked with the county official before the sale and know what the payment policy and procedures are if you are successful in obtaining a deed.

In some counties, the owner can still redeem the property within a year after the deed sale. Most states and counties, of course, recommend that no major expenditure and improvement be done during this waiting period in case the sale is over turned. However, this does not prevent you from using the property, renting the property, leasing the property with an option to buy, or using the property for financing purposes.

It is always best to consult with a local real estate attorney about any legal strategies you may have prior to final settlement. Whatever you do make sure that you place liability and fire insurance on the property as soon as the auction is complete. If something happens you will be liable and no one will overturn the sale at that time.

Selling the Property

Now it is up to you, your family, and your real estate agent as to how you profit from this real estate investment adventure once you have the finalized deed. The bottom line is profits no matter what strategy you follow. This concludes my article on Investing in Tax Deeds and Tax Lien Sales from a real estate investor’s prospective.

Tamera Aragon

Tamera Aragon is a professional online entrepreneur and has bought and sold over 300 properties, establishing her as an expert in the real estate investing field. Since 2003, she has purchased over 10 million dollars in real estate and currently holds properties all over the world. Tamera’s focus is on the booming Foreclosure market, buying Pre-foreclosures, REOs and Short Sales. Tamera who is a noted Author, Success Trainer, Speaker & Coach, shows her passion for helping others with the 17 websites she has created and several specialized products to support fellow investors throughout the world. When Tamara is not busy running her website, she is very involved with her Fiji joint ventures and investments. Tamera Aragon is one of the few trainers and coaches who is really “doing it” successfully in today’s market. Tamera’s experience has earned her a solid reputation in the industry as well as the respect and friendship of many of the top national real estate investment and internet marketing experts. Tamera Aragon believes her success has garnered her the financial freedom to fully enjoy her marriage and spend quality time with her children.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

The biggest purchase of a person’s life for the average American is their primary home where they live. Later in life, the equity in this same owner-occupied home will likely represent the bulk of the homeowner’s entire net worth.

A wise purchase can make you very wealthy, while an unwise purchase can be financially devastating. Would you prefer to take this risk alone or with a team of experienced professionals by your side?

article continues after advertisement

How many of you have seen how thick a real estate purchase and mortgage file can be at the time of closing? I’ve seen files for residential or commercial real estate loans that were three, six, twelve, and twenty-four plus inches thick by the time of closing. Could you imagine handling the closing of a purchase transaction without the expert assistance provided by real estate licensees, mortgage brokers, loan processors, underwriting teams, escrow, title insurance, appraisers, home inspectors, and several others?

As a result of the recent $418 million dollar anti-monopoly lawsuit settlement that the National Association of Realtors® (NAR) approved, let’s take a closer look at how these new buyer agency relationship regulations may directly impact you as a buyer or seller.

The potential reduction of brokerage commissions

The potential elimination of buyer’s agents from a larger percentage of future sales transactions will obviously hurt many real estate licensees. Prior to this NAR settlement, the average commission paid per real estate transaction was about 5.5%. It can be split evenly at 2.75% to the listing agent and 2.75% to the buyer’s agent or with more of the commission split going to the listing agent such as 3% for list agent and 2.5% for the buyer’s agent. Will future commission splits fall to lower amounts?

There are upwards of 1.5 million Realtors® who belong to NAR and about 500,000 additional real estate licensees who don’t belong to NAR for a grand total of nearly 2 million real estate licensees.

Upwards of 80% of real estate licensees (about 1.6 million) own at least one home. With the future loss of income from discounted or eliminated buyer’s brokerage fees, many of these real estate licensees may be forced to list their home for sale while pushing the national home listing inventory rates higher.

Generally, the buyer’s agent does the most work in a real estate transaction because they tend to interact with almost every party involved in the transaction (listing agent, mortgage broker or banker, escrow, attorney, and/or title insurance, appraiser, home inspectors, environmental specialists, etc.). Wouldn’t the elimination of a buyer’s agent be problematic for many transactions across the nation?

article continues after advertisement

How will first-time buyers afford to buy their buyer’s agent directly?

The average first-time homebuyer invests approximately 6% of the purchase price. For all homebuyer types (move-up, 2nd home, investor, etc.), it’s closer to 13% nationwide and as high as 18% here in California.

VA (Veterans or active military personnel) homebuyers are not allowed to pay buyer’s agent fees. Most of them qualify with no money down 100% LTV loans. FHA buyers usually come in with somewhere between 0% and 3.5% down. Many times, FHA home buyers do not have any extra cash to pay their buyer’s agents directly.

If homebuyers are now expected to find and hire their own buyer’s agent and pay them anywhere between 1% and 3%, it will be very challenging for many homebuyers to come up with the additional funds to pay their buyer’s agent directly and purchase their dream home.

Commissions and seller credit negotiations

Commission fees for the listing agent and buyer’s agent have always been negotiable. This new NAR settlement doesn’t change that option. Yet, it makes it more challenging for buyers, sellers, and real estate licensees to complete a transaction.

If a buyer prospect signs a buyer’s agency agreement with a real estate licensee for 2% and the seller or new home builder offers to pay 3% to the buyer’s agent, then can the buyer’s agent be paid the higher 3% commission offered by the seller or is the commission amount limited by the 2% fee mutually agreed to by the buyer and buyer’s agent? For licensees, this is a topic to be discussed with your employing broker and/or advising legal experts.

Many times, a purchase deal is structured with seller credits that cover the buyer’s agent and listing agent fees and overall closing cost credits (loan, escrow, title, inspection, and/or appraisal fees), which may vary between 5% and 10% of the total purchase price. Without these seller credits, the buyers may not have enough of their own funds to cover the required down payment and closing costs with or without being required to pay their own buyer’s agent.

The rise of dual agency, attorney closings, and self-represented deals

This NAR case settlement may set a legal precedent for future courtroom cases to completely outlaw dual agency where one licensee represents both the buyer and seller. I’ve written real estate courses in more than 30 states over the years and have held eight different real estate, mortgage, and securities brokerage licenses, so I’m somewhat familiar with the fact that many states already outlaw dual agency.

Many legal groups are behind the push to eliminate real estate licensees so that lawyers handle a higher percentage of closings like they do in New York state and elsewhere. Attorneys like to say that dual agency for Realtors® is akin to an attorney unfairly representing both sides in a lawsuit.

A buyer’s agent is focused on protecting their buyer more than any other licensed or unlicensed professional involved in a purchase transaction. Why would so many people be happy to eliminate the main party who is truly working in the buyer’s best interests?

Contingency dates and disclosure risks

Real estate contracts and inspection reports are incredibly complex. A buyer or seller who attempts to represent themselves in a purchase contract may miss important contingency dates for the completion of the appraisal, home inspection reports, or formal mortgage approval and lose their 1% to 3%+ in earnest money deposits.

Sellers, in turn, who don’t fully disclose all known or potential home and environmental risks to their buyers may later be subject to multi-million dollar lawsuits related to mold, cracked foundations, leaky roofs, or toxic air from a nearby chemical plant. The seller’s $300,000 home price sales gain later turns into a – $1.7 million dollar loss after the $2 million dollar court judgment is filed for not clearly disclosing all known or potential risks.

The median U.S. home sales price is at or just below $400,000. The average buyer’s brokerage commission fee is 2.5% or about $10,000. A buyer who is self-represented may pay too much for the home at prices well above $10,000 and put themselves at greater risk for missing out on the disclosure risks that could later cost them tens or hundreds of thousands of dollars.

A future lawsuit against the seller may net them zero if the seller files for bankruptcy protection unless fraud can be proven. The buyer still may collect zero from a recorded judgment if the seller has no assets.

For more successful real estate licensees who can afford a rather large marketing and networking budget while controlling a high percentage of the listings in their region, how many buyers’ agents will show your listing if there’s no buyer’s agent commission being offered by the seller? Why would someone work for free and take on such significant risk for nothing?

Mortgage brokers who hold a real estate broker’s license like me could step in and write up the purchase contract, negotiate the seller credits, and bring in the money to close it. Yet, why would I want to double my workload if I act as the buyer’s agent to collect no additional commission and significantly increase my liability risks? In many of my purchase deals, I value the assistance provided by the buyer’s agent more than any other professional.

Will home values be impacted by new agency regulations?

The real estate sector represents upwards of 20% of the national economy. For people who don’t hold real estate licenses, they may still be directly impacted as future home inventory numbers possibly rise and property values start to decline. As foreclosures rapidly increase, these become the neighborhood sales comps that either hurt or help your home value.

Some in the media are claiming that this buyer’s agency commission reduction or elimination will be very good for homeowners. Again, the average buyer’s brokerage commission is closer to 2.5% than 2.75% or 3%, yet I will increase it to 3% for the average $800,000 home sales price in California to arrive at an alleged $24,000 commission savings for the buyer and/or seller.

If home prices fall just 5% in California due solely to these massive Realtor® regulation changes, that’s equivalent to a $40,000 price reduction for the seller. If so, the seller is now losing $16,000 in gains ($40,000 – $24,000 = $16,000 in total losses) with just a 5% reduction in sales prices in spite of paying no buyer’s agent commission fee on a typical $800,000 home sales transaction. What happens if home prices fall 10%, 20%, or more?

The rise in mortgage rates, insurance costs, utilities, and overall skyrocketing inflation rates will also inspire more homeowners to list and sell. Real estate prices are influenced the most by the old economic theory known as supply and demand, for better or worse.

As more and more residential and commercial property go underwater or upside-down (mortgage debt exceeds value), how will buyers or sellers be able to handle the complex process of forbearance, pre-foreclosure, or short sale discounts on their own without the help of an experienced advisor?

Whether you’re in favor of this NAR settlement agreement or hate it, please research as many different sides of this topic to better understand how it may help or harm you as a buyer, seller, landlord, tenant, real estate licensee, or third-party professional.

Rick Tobin

Rick Tobin has worked in the real estate, financial, investment, and writing fields for the past 30+ years. He’s held eight (8) different real estate, securities, and mortgage brokerage licenses to date and is a graduate of the University of Southern California. He provides creative residential and commercial mortgage solutions for clients across the nation. He’s also written college textbooks and real estate licensing courses in most states for the two largest real estate publishers in the nation; the oldest real estate school in California; and the first online real estate school in California. Please visit his website at Realloans.com for financing options and his new investment group at So-Cal Real Estate Investors for more details.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/04/impact.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-04-02 01:15:562024-04-02 01:15:58Will the Realtors®’ Commission Settlement Impact You?

We are back in the East Coast to connect with our readers. Realty411 will host an Investor Summit in the City of Brotherly Love to network and learn the latest REI strategies. Our last event united investors from across the nation and many Eastern states for a fantastic day of education and collaboration. In addition, a delicious catered breakfast and lunch will also be served.

Take advantage of our discount code: 411 — to receive a discount on tickets. To learn more, CLICK HERE

Be Sure to Register, Educators Include:

Joseph V. Scorese, National Private Lender Marco Kozlowski, Investor & Author Jonah Dew, The Cash Compound Randy Hughes, Mr. Land Trust Paul Finck, The Maverick Millionaire Eric Mauz, MB Capital Solutions Michael Poggi, Investor and Author Andrea Lane, Coast2Coast Turnkey Linda Pliagas, Realty411.com and More!

-Advertisements-

Attention savvy real estate investors, it’s time for another educational and exciting Realty411 Virtual Investing Summit uniting readers for an amazing day of information and motivation.

Register for Our NEW Virtual Investing Summit on Friday, April 26th, from 9 AM to 2 PM PT (East coast time: 12 PM to 5 PM ET) and Saturday, April 27th, from 9 AM to 2 PM PT as well.

Guests can join Realty411’s complimentary VIRTUAL investing summit and learn from experts sharing important knowledge, strategies and insight.

Realty411 will virtually unite some of the most successful, knowledgeable and savvy investors in the REI (Real Estate Investing) industry to help our readers make educated and informed decisions.

Join us for an amazing day of real estate education. Every online event we produce is unique, be sure to reserve this day for REI learning at its best.

Since 2007, Realty411.com has assisted top companies expand their visibility and grow their business. Contact us for a complimentary marketing session. Investors, do you have questions about real estate investing? Are you looking for a turnkey rental? Need a solid REI referral?Book a meeting with a Realty411 team member: CLICK HERE.

Investing in apartments is one of the easiest and best ways to make money as a real estate investor. Apartments will always be in demand, especially as younger demographics continue to wait until later in life to buy homes. Aside from the regular maintenance, renting apartments for profit is a generally hands-off process, making it great for beginners just getting into real estate investing. In this article, we will share how you can buy an apartment to rent out for profit.

article continues after advertisement

Why You Should Buy an Apartment as an Investment

Before explaining how you can buy an apartment as a real estate investment, it’s important to address why you want to. When done correctly and knowledgeably, apartments can be a very profitable real estate investment strategy. With apartment investing, you have a guaranteed amount of money that you know will come in every single month. Many other real estate investing strategies do not have this reliable income stream. Apartments are also generally easy to maintain. As long as you are not investing in a large complex – which is not recommended for beginners – you will not need to rely on paying any management companies. Since demand is high for apartments, they are seen as low-risk investments, which is perfect for any beginner. It will be very easy for you to keep vacancy low and profit quickly.

How to Buy an Apartment for Real Estate Investing

There are many steps to buying an apartment for real estate investing. You will have to pick where it will be, find a good fit, conduct an analysis, look into options for financing, get it appraised, and then get tenants to start making an income from it. Below are the steps broken down into specifics to help you get started in apartment real estate investing.

Decide on a Location

The first step of buying an apartment is to decide where you will buy. There are important factors to consider: median home value, median age, unemployment rate, population growth, median salary, and job growth. All of these factors give you a little more insight into the area and the direction in which it is going. Areas with high job growth and low unemployment rates mean there are plenty of jobs. This, in turn, will lead to population growth and will result in more demand for apartments and eventually allow you to charge higher rates. Choose somewhere that is growing but not outright unaffordable for buying your first property.

Find Apartments for Sale

Once you have decided on a location, it is time to start looking for apartments for sale. At this point, you need to start considering what you are looking for in an apartment building. Consider things like the number of units, whether or not you will need to renovate, and home value. An apartment building may be a perfect fit with unit types, but it may not be the best option for your first investment property if it is pricey and will require work.

Perform a Property Analysis

Once you have narrowed down your search and found a few properties that you think could be a good fit, it’s time to perform a property analysis to understand further which property is the best option. Use the investment property calculator to get an idea of each property’s cap rate, positive cash flow, and cash on cash return. These numbers will let you know the property is a good investment or not.

Look Into Financing Options

Now that you have a better understanding of the costs of the apartments you are looking at and the return you expect to get, it’s time to look into your financing options. Most real estate investors do not have the capital on their first deal to buy it outright. Using financing will allow you to buy the property and use the income to pay it off quickly. You can either choose to finance through a traditional mortgage, a home equity loan, or private financing. Most beginners prefer to do a traditional mortgage for their first property, but you must do your research and find the financing option that works best for you. If you already have a home, you may be better off with the home equity loan.

article continues after advertisement

Get the Apartment Inspected and Appraised

Once you decide on the apartment you feel is the best investment, you need to have it professionally inspected and appraised. The inspection is essential to ensure you are not buying a property with any damage you were not aware of. Structural damage especially could be very costly. Your mortgage provider will require an appraisal to ensure the purchase price is similar to the appraised value.

Renting the Apartment

Once you have purchased the apartment, it’s time to rent it out and make some income. For the best results, you will want to invest in making any necessary home improvements and ensuring the apartments have a modern look with updated appliances and amenities. Make sure to screen all potential renters to lessen your chances of dealing with eviction or undesirable tenants. Hire an attorney when you first start off to deal with all of the legal aspects of renting out an apartment.

Summary

Learning how to buy an apartment is essential to a successful real estate investment strategy. It’s an excellent way for beginners to start making a reliable income from their investment properties. Apartments are generally very little work once they are purchased and are an easy way to make passive income.

For more tips on real estate investing, make sure to check out the rest of our articles.

Joe Arias and his partners have flipped hundreds of properties in the Southern California Region. He has developed cutting-edge systems to simplify and scale the entire remodel process that can easily be applied to flipping, rentals, wholesaling, and other passive income strategies. More recently, Joe founded a real estate investing education company called RealSuccess Investments, allowing him to share his tools and systems with hundreds of up-and-coming investors.

RealSuccess is focused on education on flipping, rentals, passive income, and wholesaling.

Joe is also a best-selling author. He has written 4 books: Finding your RealSuccess, First Steps to Flipping, R stands for Rentals and Retirement, and Wholesaling Real Estate.

“I came from Argentina when I was 20, I am 40 years old now. I didn’t know anyone, I am CERO generation, usually people say, I am first or second generation but I was the one that crossed the border, no language, no friends, no family, no money, nothing, nada… If I can do it, anyone can.”

From a young latino immigrant to a celebrated real estate investor, Joe is a true testament to hard work and discipline. As an investor, he has made it his mission to help others achieve financial freedom while enjoying living a life of passion, fulfillment, and empowerment.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/03/apartment.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-03-14 04:54:322024-03-14 04:54:33HOW CAN YOU BUY AN APARTMENT TO RENT OUT FOR PROFIT

Legacy Invest specializes in turnkey real-estate solutions, offering meticulously renovated properties that are tenant-ready and low-maintenance in St. Louis, MO.

This city has has emerged as Legacy Invest’s focal point, offering investors a thriving market with affordable yet appreciating properties.

Founded on principles of integrity and client care, Legacy Invest stands apart in the competitive landscape of real estate investment.

Legacy Invest, a company deeply rooted in family values, aims to provide top-notch properties that enable clients to build and sustain generational wealth.

In addition to single-family homes, Legacy Invest offers opportunities for investors to explore duplexes and multifamily properties. While turnkey solutions remain the firm’s forte, Legacy Invest has flexibility in accommodating individual preferences and investment strategies.

Learn more about Legacy Invest and the burgeoning St. Louis market today.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/03/legacy.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-03-07 03:42:352024-03-07 03:42:53Learn About Legacy Invest and Build Your Legacy

When homeowners fail to pay real estate (property) taxes, the government has the right to sell their property in a state “tax sale”. In a Tax Lien state, homeowners have an opportunity to pay back the amount owed within a specific time frame even after their property has been “sold” to an investor. The investor may be paid back with interest. Should homeowners miss the pay deadline, the investor becomes owner of the property at great savings. In a Tax Deed state, investors bid for immediate ownership of a property or are eligible for the deed and ownership of the property after a redemption period passes.

By law, Tax Deed sales must be announced to the public, and are usually sold to the highest bidder. The winning bidder purchases the deed to a piece of property, becoming the new owner and obtaining all rights to the property – clear of any mortgages, liens, deeds of trust, etc.

One interesting thing to note is very few people know much about Tax Deed sales. So, competition may not be as fierce in this niche as it is in others.

Why Is Tax Lien & Deeds a Good Investing Niche to Consider?

Tax Deeds are sold in almost every state throughout the United States. 50 states are governed by state-mandated laws to protect & reward investors.

You can pick Your Price. Research the list and pick ones out that are in your price range.

You can obtain properties which allow for all types of exit strategies (flip, rent, or live).

Investors & Banks have been using this strategy for over 150 years.

The rules vary from state to state. In certain circumstances you can obtain an entire property for only the taxes and penalties owed. Generally, you will pay between 50 to 90 percent below market price.

article continues after advertisement

General Downsides of Investing in Tax Lien & Deeds Niche?

Lacking Liquidity of Funds: In a Tax Deed transaction, you can have your money tied up for several years before you can sell the property, because title companies may not issue title insurance on the property until all liens are cleared, and it is obvious that clear title can be granted. This process will sometimes take more than a year. Fixing up and or remodeling properties to maximize your eventually sale can also take considerable time.

Time and Complexity: Tax Deed laws vary from state to state and sometimes from county to county within a state. This requires a time commitment to learn the rules of a state and its counties, research properties and attend auctions. In addition title companies sometimes will not issue title insurance for at least the first year on any property bought at a Tax Deed sale. This means it could be hard to get a loan until it is clear.

Investing Risk: Purchasing property at a Tax Deed sale definitely has risks if you have not done extensive due diligence. You must do your homework, title searches, drive buy inspections, history reports etc. Once you buy a Tax Deed, you will own the property including all of it potential problems. The major thing to keep in mind is that at a Tax Deed sale, unlike a Tax Lien sale, you are buying the real estate and we believe that the required level of due diligence becomes extremely high. The other thing you want to know at a Tax Deed sale is if the property is being purchased free of all other liens and encumbrances. There are a number of states where this is true and a few where it is not true. You need to make sure that you get what you paid for. This requires knowledge of what the values are and what the potential hazard could be.

In summary, Real Estate tax sale laws vary from state to state, as do the redemption periods, and there are risks investors should be aware of in addition to the potential rewards of buying tax sale properties.

Pros and Cons of Tax Lien & Tax Deed Sales

TAX LIENS: A lien is a financial claim made against a property. A Tax Lien is a claim for unpaid property taxes issued by the local taxing authority. Failure to pay real estate taxes is one of the leading causes of distressed properties leading to home loss. Investors typically buy Tax Lien properties through an auction after a homeowner fails to heed warnings by the tax authority to pay property taxes. Most states allow homeowners to reclaim their property by paying off the debt in full by a certain date. This is called the “Redemption Period”. The redemption period offered varies from state to state. However, in some locations, investors may have to wait two full years before being paid back or gaining the deed for the property.

Tax Lien Pros

Possibility of good returns in interest (up to 24 percent in some states) paid by homeowners.

Possibility of owning property at a fraction of its true value.

Option to sell, rent or hold the property for additional profit once title is held.

Lower Investment Risk: If the homeowner doesn’t pay up, the tax purchaser is first in line to own the property. No tenants, banks or brokers to deal with.

article continues after advertisement

Tax Lien Cons

May Not Make Any Money: There is no guarantee the homeowner will pay off taxes and interest on the lien. The process of getting the deed at the end of the redemption period isn’t simple and may require a lawyer.

Required Capital: You must pay what is typically a large amount of cash for your bid at the tax sale. You definitely will need more capital to buy properties at Tax Deed sales. Although it varies from property to property, from county to county, and even from state to state, you will likely need a minimum of $5,000 to $10,000 to get started in Tax Deed investing. A good credit rating may also be necessary to sign finance contracts. Check local rules and regulation as well as the history of Tax Deed auctions in an area to get a feel for the capital you may need.

Uncertainty of property condition: With no prior home inspection, there is no guarantee of the property’s condition or value.

Property Owner may Be Foreclosed on: If you foreclose, you are stuck with the hassle of selling the property from which you may profit but on the other hand you may not recoup your initial investment.

TAX DEEDS: A Tax Deed is a legal document indicating ownership of property, also referred to as “title.”When the government intervenes to put properties delinquent in real estate tax payments up for auction, investors can pay the back taxes and own the property for well below market value. To locate and invest in Tax Deed sales, check local newspapers, local tax collectors or the Internet, where many websites post relevant information.

Tax Deed Pros

Quick and easier way to become a property owner.

Opportunity to acquire existing equity.

Opportunity to purchase property directly from the property owner at bargain-basement prices prior to a Tax Deed sale.

Fortunately, investors who sow the seeds of diligent research can reap the rich rewards of tax property sales. DUE DILIGENCE is required for Tax Lien and Tax Deed investing deals. This concludes my article on Investing in Tax Deeds and Tax Lien Sales – PART 1.

Please watch for my next investing article that will wrap up all you need to know to start investing in Tax Deeds and Tax Lien Sales – PART 2. I’ll be going over the steps real estate investors should take for Tax Lien and Tax Deed Investing deals.

Tamera Aragon

Tamera Aragon is a professional online entrepreneur and has bought and sold over 300 properties, establishing her as an expert in the real estate investing field. Since 2003, she has purchased over 10 million dollars in real estate and currently holds properties all over the world. Tamera’s focus is on the booming Foreclosure market, buying Pre-foreclosures, REOs and Short Sales. Tamera who is a noted Author, Success Trainer, Speaker & Coach, shows her passion for helping others with the 17 websites she has created and several specialized products to support fellow investors throughout the world. When Tamara is not busy running her website, she is very involved with her Fiji joint ventures and investments. Tamera Aragon is one of the few trainers and coaches who is really “doing it” successfully in today’s market. Tamera’s experience has earned her a solid reputation in the industry as well as the respect and friendship of many of the top national real estate investment and internet marketing experts. Tamera Aragon believes her success has garnered her the financial freedom to fully enjoy her marriage and spend quality time with her children.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

Between January 2020 and October 2021, the M1 money supply (cash or cash-like instruments) quickly rose from $4 trillion up to $20 trillion in just 22 months. Money velocity, or money creation speed, is the true root cause of rapidly declining purchasing power and skyrocketing inflation. The more money in circulation, the less purchasing power for the dollar.

article continues after advertisement

In January 2024, Americans were paying $213 per month more to purchase the same goods and services one year earlier in 2023 because of rising inflation and the declining purchasing power of the dollar. As compared with two years ago in 2022, Americans are paying $605 more per month. Sadly, we’re now paying $1,019 more PER MONTH ($12,228 more per year) today for the same goods and services we purchased three years ago in 2021.

Shipping, trucking, and other transportation costs are quickly rising amid geopolitical tensions. Historically, increasing transportation and energy costs are a root cause of inflation trends. Don’t be surprised if inflation rates and interest rates are both higher later this year instead of lower.

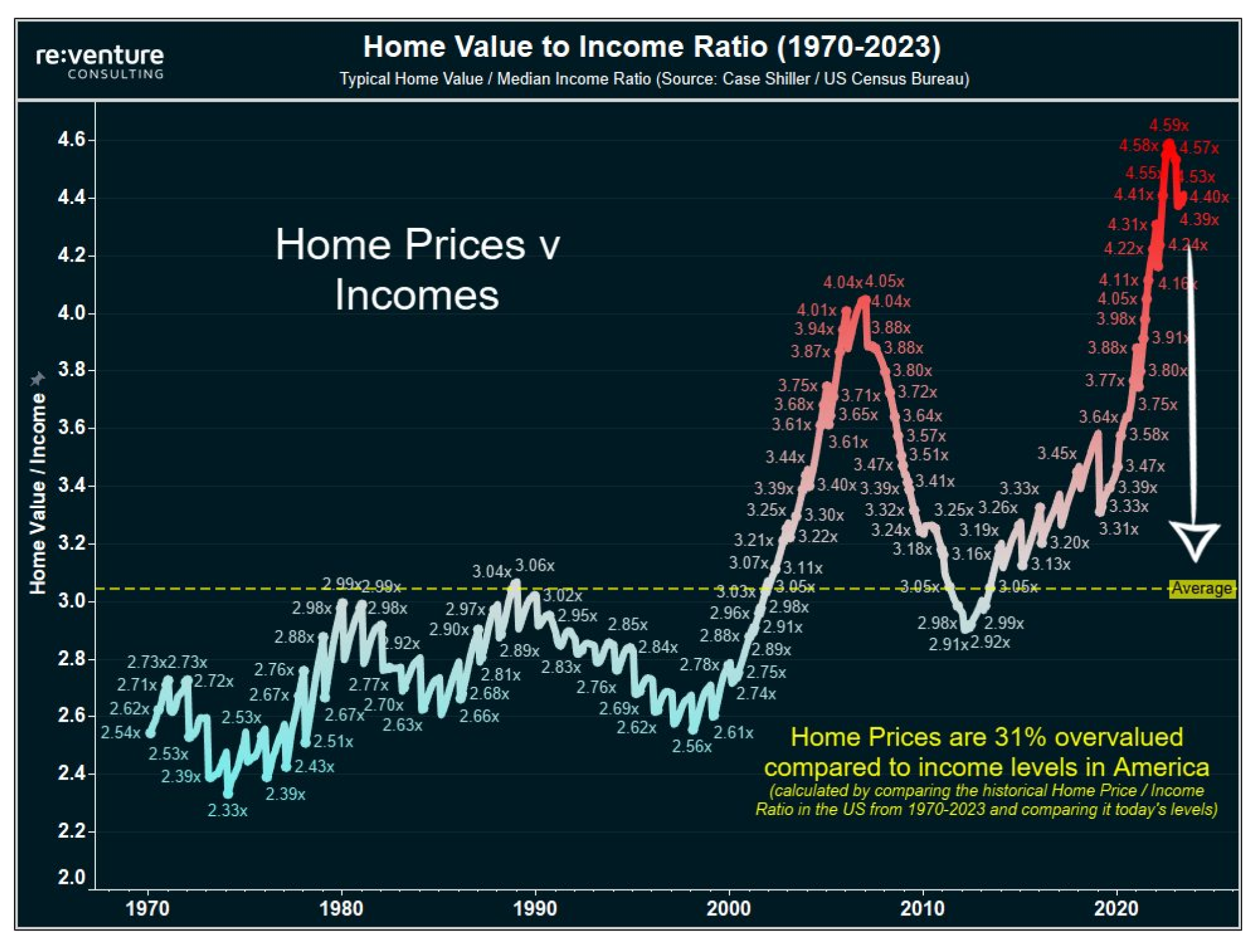

Home Value-to-Income Ratio in the U.S.

The U.S. home value-to-income ratio is calculated by dividing the $342,000 median home value by the $74,580 median household home, according to Economy Vision. If home prices had grown at the same rate as income since 2000, the median U.S. home would cost nearly $294,000, or 31% to 32% lower than today’s prices.

U.S. households need an average income of $166,600 to afford a home, but the median household income is $74,580. The lowest home price-to-income ratios in large metropolitan regions are in Pittsburgh (3.2x), Buffalo (3.5),and Cleveland (3.5), while many California regions are near 10 to 20x. Some smaller suburban or rural regions in Southern Illinois and other Midwest regions are closer to 1.5 to 1.8 for home price-to-income ratios.

Increasing Distressed Residential and Commercial Mortgage Numbers

Millions of Distressed Residential Mortgages

The federal government keeps extending the millions of distressed FHA and VA loans, or offering discounted loan modifications, partly so that they don’t push the national home listing supply skyward and reduce home prices at the same time.

The C-19 foreclosure or forbearance moratoriums for millions of FHA and VA borrowers began back in the fall of 2020. As a result, many of these home borrowers haven’t made a mortgage payment for more than three years.

The FHA forbearance moratoriums for FHA borrowers expired on November 30, 2023 while the VA forbearance moratoriums were extended until May 31, 2024. At some point, these loans will need to be brought back current, sold, or foreclosed.

In the previous housing crash that was especially bad during 2008 to 2012, only about 2% (or 1 in 50 mortgages) of all residential loans were delinquent. Yet, these distressed home mortgages became future lower value comps for the nearby homes while driving their prices downward too, sadly.

If and when the national home listing supply numbers rapidly increase this year, it will eventually have a negative impact on home price trends because it’s all supply-and-demand economics at the true core. When supply of a product or asset rises and exceeds buyer demand, then prices tend to fall (and vice versa).

Concerning Commercial Mortgage Trends

An estimated 44% of office buildings nationwide with mortgages in place are claimed to be upside-down with negative equity here near the start of 2024. Some office buildings are selling for as low as $9 per square foot, not $900/sq. Ft. By the end of 2024, the underwater office building numbers may be well over 50% and the overall underwater or upside-down numbers for all commercial property types may be somewhere within the 20% to 25% range.

Physical and Online Retail Store Numbers

In Q3 2023, the amount of U.S. retail space available for lease plunged to an all-time low since the CoStar commercial real estate group started tracking back in 2007.

The previous seven years in a row (2017 – 2023) shattered all-time retail space closings per square foot in U.S. history.

Through just September 2023, 73 million square feet of retail space closed in 2023, as per Coresight.

140 million square feet of retail space has been demolished in the last decade, according to CoStar.

Top 6 online sales percentages in 2023: 1. Amazon (37.6%); 2. Walmart (6.4%); 3. Apple (3.6%); 4. eBay (3%); and 5. Target and Home Depot (a tie at 1.9% each), per Statista.

10.4% of total annual U.S. retail sales were online in 2017;

12.2% of total annual retail sales were online in 2018;

13.8% of total annual retail sales were online in 2019;

17.8% of total annual retail sales were ecommerce in 2020;

18.9% of total annual retail sales were ecommerce in 2021; &

18.9% of total retail sales were online in 2022, per Statista.

The full 2023 online year results weren’t published yet.

Record-High Car Payments

Some new monthly car payments are reaching $3,000 per month, while average new car payments are near $730 to $750 per month. Additionally, many monthly car insurance payments are reaching $400 to $500 per month in cities like Detroit and Philadelphia. How much are these car owners paying in gas and maintenance as well?

The national average cost for car insurance rose a whopping +26% from last year, according to Bankrate.

The most expensive cities for car insurance are:

Detroit – $5,687 Philadelphia – $4,753 Miami – $4,213 Tampa – $4,078 Las Vegas – $3,626

The cheapest cities are:

Seattle – $1,759 Portland – $1,976 Minneapolis – $2,044 Boston – $2,094 Washington D.C. – $2,430

The average car loan today is valued at 125% LTV (loan-to-value) for the typical car on the road with a loan with an average negative equity balance of -$6,000. This is partly because so many car buyers are purchasing cars with no money down and adding their registration, licensing, taxes, and warranty fees on top of it before driving off of the car lot. New cars usually drop in value about 20% in the very first year of purchase.

article continues after advertisement

Inflationary or Deflationary Economic Cycles

Inflation has been described as an increase in the general level of prices of a certain product in a specific type of currency. Inflation can be measured by taking a “basket of goods,” and then comparing them at different periods of time while adjusting the changes on an annualized basis.

General inflation measures the value of a currency within a certain nation’s borders, and refers to the rise in the general level of prices. Currency devaluation measures the value of currency fluctuations between different nations. Some related terms associated with inflation are as follows:

* Deflation is a rise in the purchasing power of money, and a corresponding lowering of prices for goods and services. The Fed doesn’t like this economic period of time and will probably cut short term rates to offset it.

* Disinflation refers to the slowing rate of inflation. The Fed may like this type of economic time period, and may stop raising rates at this point in the economic cycle.

* Reflation is the period of time when inflation begins after a long period of deflation. Depending upon the severity of inflation, the Fed may pause the rate hikes or gradually begin rate hikes.

* Hyperinflation is rapid inflation without any tendency toward equilibrium. It is inflation which compounds and produces even more inflation. It is when inflation is much greater than consumers’ demand for goods and services. The Fed, and the rest of America, do not typically like this economic period, so they may enact a series of significant rate hikes to slow inflation.

The Wealth Distribution Imbalance

Wealth distribution across the U.S. has become increasingly concentrated in the hands of fewer people since 1990. Overall, the top 10% of wealthiest Americans own more than the bottom 90% combined, with more than $95 trillion in wealth for the top 10%.

Here in 2024, the share of wealth held by the richest 0.1% is near its peak with a minimum of $38 million in wealth in just 131,000 households.

With $20 trillion in wealth, the top 0.1% earn an average of $3.3 million in income each year. The greatest share of the wealth owned by the top 0.1% is held in corporate equities or stocks and in mutual funds, which make up over one-third of their total assets.

Households in the lower-middle and middle classes as found in the 50% to 90% income and asset brackets are claimed to have a minimum of $165,000 in wealth held primarily in real estate and followed by pension and retirement benefits.

Unless you’re in the Top 0.1%, the odds are quite high that the bulk of your wealth is concentrated in real estate if you’re fortunate enough to own at least one property today. In our next meeting, we will discuss how to find discounted real estate and other investments and how insurance and estate planning can help protect your assets for you and your family.

Extreme Rate Swings, Steady Home Gains

Between 2000 and 2023, the median U.S. home appreciated approximately 10.63% per year. By comparison, California homes rose 12.55% per year between 2000 and 2023.

Doubling Value Forecasts: The Rule of 72 is an investment formula used to estimate how long it may take for an asset to double in value using a projected annual rate of return (72/7 or 7% = 10+years).

A home purchased using the national average annual gain of 10.63% would double in value in just over 6.77 years if purchased this year (72/10.63 = 6.77 years). A California home would double in just 5.74 years (72/12.55) if these same average annual appreciation gains continued.

Home prices tend to go skyward following a Fed pivot when they start slashing rates. When will the Federal Reserve start cutting rates again? Let’s take a look at their calendar for 2024 two-day meeting dates: Jan. 30-31 (no rate change); March 19-20; April 30- May 1; June 11-12; July 30-31; Sept. 17-18; Nov. 6-7; & Dec. 17-18.

Inflation severely damages the purchasing power of the dollar while usually boosting real estate values. Because it’s more likely than not that inflation will continue rising above historical average trends, then real estate may be one of your best hedges against inflation as your wealth compounds and increases as well.

Rates may be lower, the same, or higher by the end of 2024, partly due to our volatile inflation movement and weakening dollar. However, there’s a tremendous upside for real estate investors if you’re willing to stay focused on the opportunities and not let the negative news scare you away.

Rick Tobin

Rick Tobin has worked in the real estate, financial, investment, and writing fields for the past 30+ years. He’s held eight (8) different real estate, securities, and mortgage brokerage licenses to date and is a graduate of the University of Southern California. He provides creative residential and commercial mortgage solutions for clients across the nation. He’s also written college textbooks and real estate licensing courses in most states for the two largest real estate publishers in the nation; the oldest real estate school in California; and the first online real estate school in California. Please visit his website at Realloans.com for financing options and his new investment group at So-Cal Real Estate Investors for more details.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/02/house-prices.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-02-29 06:30:332024-02-29 06:30:35Inflation, Home Price Swings, and Wealth Distribution