One of the longest proven successful ways to get good leads as a real estate investor is calling on For Sale by Owner (FSBO’s) listed properties. In my experience, I have found great success in helping FSBO’s with their situation while at the same time buying discounted real estate. If you are on a budget and just getting started then you can do this yourself, or if you can at all afford it, I highly recommend you hire someone like a virtual assistant to do it for you.

article continues after advertisement

Why Are FSBO’s Good Leads?

Often times homeowners who place their house on the market without a realtor ( FSBO’s), are in a position where they need to sell a home quickly. When this happens, you are able to help them by closing quickly with cash, while at the same time, you receive a great discount. There are many reasons a homeowner might need to sell quickly. Some are trying to avoid getting behind on payments, some are already behind on payments, others need to immediately move to new location for job, some received a property gifted through probate, may be experiencing illness or maybe the landlord doesn’t want to own a property for rent any more, etc. Whatever the specific reason a person doesn’t utilize a realtor and place their property for sale on the MLS, Craigslist, Kijiji or even EBay, it is likely there is an opportunity for you to get a great wholesale deal.

Where Do You Get FSBO Leads?

The first step is to locate the properties not listed on MLS, however for sale by the owner direct. How do you do this?

1. Classified Ads Online: There are several online classifieds such as Craigslist.org or Kijiji.ca or backpage.com and many others. It’s so easy to search the internet for this stuff just type “your city” properties for sale by owner; see what comes up in the Google and Bing search engines!

2. Newspaper classifieds: Checkout newspapers in the areas you would like to buy. (also often available online)

article continues after advertisement

What Do You Do Once You Have The Locations For Leads?

A. Grab a copy of the FSBO magazines offered for FREE in grocery stores. These could be great leads as someone is paying a lot of money to put their house in a magazine. I view this as sign that the owner could be a motivated seller.

B. Go the websites of newspapers and look at their classified section online. You can put these links in your favorites.

C. Visit FSBO online websites. Here are a few sites I like:

Owners.com

ForSaleByOwner.com

FSBO.com

HomesByOwner.com

Trulia.com

You will want to check the FSBO sections in these resources daily. If there is a good real estate deal for sale, it will be sold quickly to the person who acts quickly – You!

What Do I Look For In A FSBO Deal?

All ads listed could be potential investments. To save time however , you want to be looking for keywords or phrases that indicate the seller has a motivation to sell or is showing signs of flexibility. Here are a few examples of keywords to watch out for:

“Must sell” “Just reduced” “For Sale Or Lease” “Seller Financing” “Fixer Upper” “Handyman Special”

Create Your Motivated Seller “Hit” List

This is a list of those you will want to contact to find out more about the property and the seller’s situation. If using paper (like a newspaper in hand), you will want to mark the ads with your sharpie or highlighter as you are scanning the paper for those “motivated” words listed above. Mark as many ads as you can! It is better to have too many leads than too few. If online- – -copy and paste the ads found on newspaper, classifieds and FSBO sites to a word or excel doc, then print it out. Remember having too many leads is a good thing as it keeps your options open.

Tamera Aragon

Tamera Aragon is a professional online entrepreneur and has bought and sold over 300 properties, establishing her as an expert in the real estate investing field. Since 2003, she has purchased over 10 million dollars in real estate and currently holds properties all over the world. Tamera’s focus is on the booming Foreclosure market, buying Pre-foreclosures, REOs and Short Sales. Tamera who is a noted Author, Success Trainer, Speaker & Coach, shows her passion for helping others with the 17 websites she has created and several specialized products to support fellow investors throughout the world. When Tamara is not busy running her website, she is very involved with her Fiji joint ventures and investments. Tamera Aragon is one of the few trainers and coaches who is really “doing it” successfully in today’s market. Tamera’s experience has earned her a solid reputation in the industry as well as the respect and friendship of many of the top national real estate investment and internet marketing experts. Tamera Aragon believes her success has garnered her the financial freedom to fully enjoy her marriage and spend quality time with her children.

Learn live and in real-time with Realty411. Be sure to

register for our next virtual and in-person events. For all the details,

please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/01/fsbo.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-01-30 04:45:112024-01-30 04:45:13Targeting Properties – For Sale By Owner (FSBO)

This is an incredible opportunity for skilled professionals who want to work with a company that guarantees abundant direct organic daily leads, hands-on management training and support, niche mortgage loan programs with competitive pricing, and advanced mortgage technology.

Mortgage Loan Officers can expect to close their first loan within four to six weeks after the completion of their initial training.

Mortgage Loan Officers who join the Stratton Equities team can expect the following:

Competitive compensation: Stratton Equities offers a highly competitive compensation plan, potentially allowing Mortgage Loan Officers to earn their first year $110,086.26 – $190,677.36.

Strong resources: Stratton Equities’ interest rates are some of the lowest nationwide in private lending, starting at 6.75%, and can pre-approve a loan in 24 hours.

Room for growth: As a rapidly growing company, Stratton Equities offers ample opportunities for advancement and career growth. With a focus on promoting from within, Mortgage Loan Officers who join the team will have the chance to take on new challenges and responsibilities as they progress in their careers.

A dynamic work environment: At Stratton Equities, Mortgage Loan Officers will work in a fast-paced, dynamic environment focused on innovation and results. As a part of the loan officer team, you can work directly with prospective real estate investors, entrepreneurs, and borrowers on their real estate endeavors.

If you are an experienced Mortgage Loan Officer looking for an exciting new opportunity to grow your career or a licensed Mortgage Loan Originator that is new to the industry and needs help finding business, then Stratton Equities is the place for you to earn a great income.

This is an incredible opportunity to join a leading nationwide mortgage lender and build a bright future with a company that values its employees and their contributions.

Contacts For media inquiries and interviews, please contact Kelly Bennett of Bennett Unlimited PR at [email protected].

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/01/we-are-hiring.jpg5001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-01-15 01:15:142024-01-15 01:15:16Stratton Equities is Hiring Mortgage Loan Officers to Join Their Dynamic New Jersey Team and Build a Lucrative Career in the Mortgage Industry

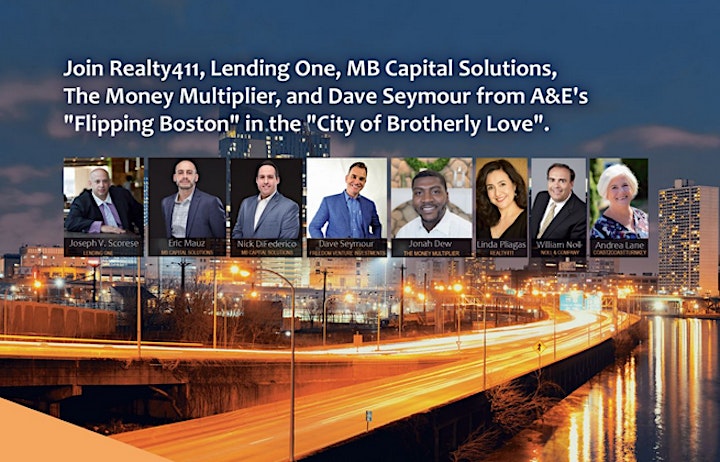

Join us to Meet with Fantastic Company Leaders, Network with Investors and Liked-Minded Wealth Builders from around the Nation!

Date and time Saturday, April 13 · 8:30am – 6pm EDT

Location Mummers Museum 1100 S 2nd St. Philadelphia, PA 19147 United States

About this event 9 hours 30 minutes Mobile eTicket

Grow Your Wealth with Real Estate Investing – Join Us for an In-Person Realty411 Investor Summit in Philadelphia, PA.

We have exciting news regarding our In-Person Event in Philadelphia, PA. Our special one-day conference in “The City of Brother Love” will host incredible educators from around the country, who are ready to share their valuable insight.

Be sure to join us in PERSON in Philadelphia.

We will have wonderful resources and guests will have direct access to private capital, plus business and commercial funding as well. Now is the time to grow your real estate business to new levels.

Now is the moment to grasp this opportunity — the chance to network with sophisticated investors from Pennsylvania, New York, New Jersey, Florida, Denver, Maryland, California, and many other states!

Be sure to pencil this date now and join us in-person to gain specialized insight and knowledge. The information shared on this day could catapult your portfolio to new levels.

This one-day conference also is combined with a special pre-event Clubhouse Party on Friday evening, PLUS a property bus tour on Sunday. This THREE-DAY investor intensive will unite active real estate and landlords and has something for everyone regardless of their experience level in real estate.

Join this memorable day and receive knowledge for a lifetime.

Learn the Latest Niches in Real Estate + Connect with Influential Investors from across the nation right here in The City of Brotherly Love.

Are you ready to Grow Your Real Estate Business, Portfolio and Network? JOIN US!

This is Your Chance to meet TOP Leaders in REI, Local & National Experts

Learn from Leaders & Industry Pros

Meet Local PLUS Out-of-Area Investors

NON-Stop Tips for Real Estate Success

Bring Lots of Business Cards

Join us at the famous and festive Mummers Museum for a unique and exciting real estate event! This event is produced and hosted by Realty411.com. Since 2007, we have dedicated our time and resources to help expand real estate investing knowledge and education by producing magazines, virtual conferences, webinars, podcasts, and live events.

We also produce REI Wealth magazine, which is our digital publication. REI Wealth has been existence since 2012 and was designed for online learning.

Learn more about our digital publication at: http://REIwealthmag.com

INVEST YOUR TIME HERE FOR ONE SPECIAL DAY OF NETWORKING & MOTIVATION – TAKE YOUR REAL ESTATE KNOWLEDGE TO A WHOLE NEW LEVEL.

Don’t miss our complimentary real estate investor summit. What can you expect?

Learn with PROVEN Leaders in the Industry:

Receive the latest REI knowledge from active investors

We feature the latest technology to expand your income

Meet other investors with common goals and mindsets

Develop relationships with leaders in the industry

Share your opportunities with potential clients

Realty411’s publisher has owned national rentals for decades

We will share life-changing information with as many as possible

We host national and local events to meet our readers and spread knowledge

To learn more, read and download our event flyer, CLICK HERE.

Our mission is simple: To provide realty knowledge and resources so that everyone can learn about the benefits of real estate investing.

OTHER SPECIAL BONUS PERKS INCLUDE:

All Guests Will Receive Our Investment Magazine

Meet Local Leaders & Industry Giants – From Coast to Coast

Influential Real Estate People & Business Owners Are Attending

Learn How to Leverage and Meet Private Capital Lenders

Find Potential Partners, New Friends, Build Your Circle of Influence

Your Net Worth = Your Network — Don’t miss this event

Mingle with Top REI Leaders & Industry Professionals Here

Realty411.com’s founder is an accredited investor and REALTOR® in the state of California and has been a licensed real estate agent for over17 years.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/01/Philadelphia-event.jpg470940dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-01-09 03:59:252024-04-17 02:48:21Realty411’s Investor Summit in Philadelphia – Join Us to Network and Learn

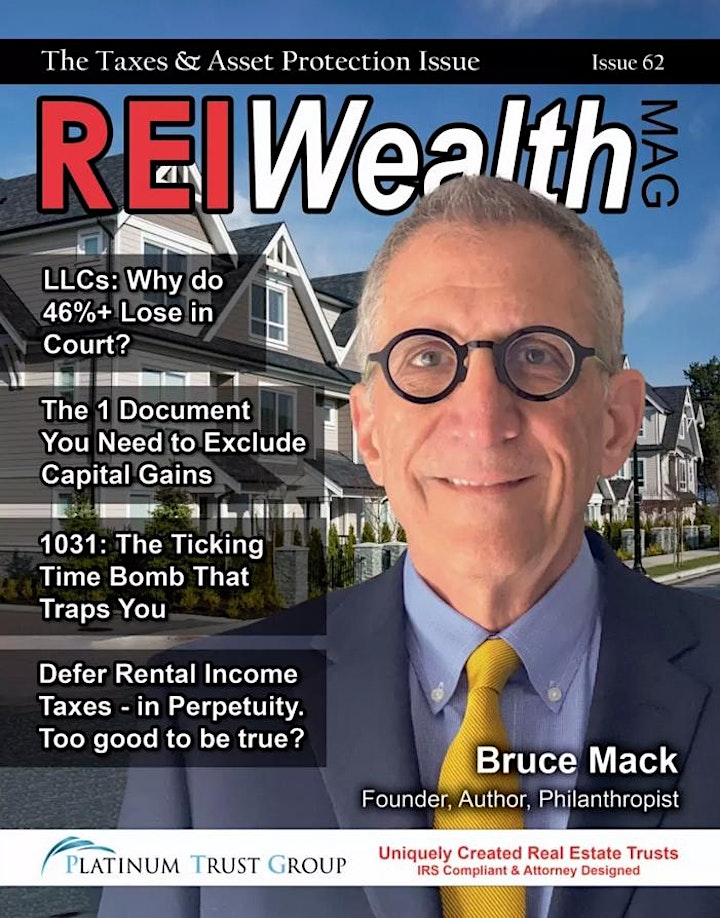

Were you aware that Real Estate Investors can save 78% – 90% or more on their annual taxes? And, now you can too! RSVP to our webinar today.

Date and time Saturday, January 20 · 5 – 6pm PST

Location Online

About this event 1 hour Mobile eTicket

Were you aware that Real Estate Investors save 78% – 90% or more on their annual taxes? And, now you can too! Did I get your attention yet?

We have a solution that completely solves that giant tax problem for ALL Real Estate Investors.

In today’s real estate market, the only constant is volatile change…Your business is in a constant state of flux. Yet, there is one thing that’s not changing…

Uncle Sam is still demanding his tax payments on your rental income and capital gains from your REI business, including Flippers who get classified as Real Estate Dealers. Using our Trust, you cannot be classified as a Real Estate Dealer.

Real Estate Dealers are taxed at ordinary income rates, plus self-employment @ 15.3%, Medicare Surtax & AMT. That could easily be over 50% of your profits. OUCH!!

There is a new explosion of lawsuits because of the economy and people are getting desperate!

LLCs don’t protect you (in fact over 46% of the time when litigated, the corporate veil is pierced). My special guest and nationally known speaker, author and real estate investor, Bruce Mack, is going to show you a superior solution to keep your lien, levy and judgment proof.

On this upcoming, MUST attend, LIVE webinar for your REI BUSINESS SURVIVAL, you’re going to get the solutions to both problems. You will be amazed at how simple the solution is!

Join us and our friend, Licensed Financial Advisor, Bruce Mack, for this LIVE Webinar.

Reserve Your Seat here now!

January 20, 2024

5pm PST / 6pm MST / 7pm CST / 8pm EST

Reserve your space today and the event Zoom link will be sent to guests for this amazing webinar that could potentially save you money.

Make sure you stay until the end of the webinar! Bruce will tell you how you can get a complimentary one-on-one consultation ($250 value) just for attending the webinar.

See you on the upcoming MUST attend LIVE webinar!

PS: Join us for this LIVE webinar and learn if you qualify to defer 78% to 90% or more of your tax burden in perpetuity … LEGALLY, and without having to move to another country to do so.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/01/asset-protection.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-01-09 01:54:492024-04-17 02:49:47Stop Overpaying on Your Taxes and Get Absolute Asset Protection

For many licensed real estate professionals and investors, this year will likely be the most important year for their career and investment strategies. I could write the same thing for the start of any previous year because it’s true for almost every single new year that brings us new opportunities.

I’ve held various real estate broker licenses in multiple states over the past few decades, so I fully understand the pressure that real estate licensees are under to find new clients and listings. I’ve also written college textbooks and courses (economics, finance, and real estate) in most states for the top 2 largest U.S. real estate educational firms and for the oldest and best-known real estate school in California.

Whether you just passed your very first real estate exam or have been an “old pro” for the past few decades like me, please reach out to me and we will work together to create a marketing plan for your target region. I’m also available online for brokerage office meetings and can be found as a new OnZoom instructor on their national public platform that’s linked here: OnZoom – Rick Tobin.

REALTOR® Statistics

In 2023, the U.S. had 1,566,354 Realtors, members of the National Association of Realtors, out of approximately 2 million real estate agents.

There have been between 200,000 and 300,000 active real estate licensees in California in recent years, depending on the boom and bust cycles.

Sixty-four percent of REALTORS® were licensed sales agents, 20 percent held broker licenses, and 18 percent held broker associate licenses.

The typical REALTOR® is a 60-year-old white female who attended college and is a homeowner.

62% of all REALTORS® are female, and the median age of all REALTORS® is 60.

Real-estate experience of all REALTORS® (median): 11 years

Median tenure at present firm (all REALTORS®): 6 years

Most REALTORS® worked 30 hours per week in 2022.

The median gross income of REALTORS®—income earned from real estate activities—was $56,400 in 2022, an increase from $54,300 in 2021.

REALTORS® most often prefer to communicate with their clients through text messaging, at 94%. Ninety-two percent preferred to communicate via telephone, and 90% through email. Source: National Association of Realtors

Marketing Strategies for Realtors and Others

Attention spans: You have just 7 or 8+ seconds to quickly capture your readers’ or viewers’ attention span with a print or digital media ad. Focus on their needs and wants, not yours, for a higher rate of response (1% or higher).

Cash-on-cash advertising returns: The investment return for every $1 invested in your advertising campaign. For example, you invest $100 and collect $10,000 from a future closed commission at a 100-to-1 return on your investment.

Print media: Forms of marketing that can be held in your hand like mailed letters, postcards, flyers, newspapers, and magazines. Please avoid blind ad risks when you don’t clearly identify yourself as a real estate licensee.

Digital media: Online ads can be found on your blog, website, social media, and in native ads or sponsored ads (examples: Facebook, Google, Nextdoor, Alignable, Taboola, Outbrain, etc.). Email, text, and telephone marketing also work if the prospects aren’t on any do-not-call lists that exceed 300 million phone numbers.

Repetition is the key to programming and advertising. The more often that consumers see your ads online and/or in print media, the more likely they will remember you before contacting you for your services.

Merge print and digital media: The addition of a QR code on a print media design, which readers can scan with their phones prior to them seeing your online home listing or personal website, is an exceptional combination of both print and digital media at the exact same time at a fraction of the cost. There are free or affordable QR sites that will take your websites and convert them into a new QR code (Adobe, Canva, etc.).

article continues after advertisement

Social Media Marketing Numbers

Numerous published studies note that younger Americans are spending somewhere between 4.8 and 6+ hours on social media and a grand total of closer to 9 to 11+ hours on all types of media (gaming, television, movies, videos, etc.) every single day. If you want to reach your target audience for young first-time home buyers and older prospects, they’re found online.

With first-class stamps reaching 68 cents in January 2024 (3rd increase in a year; it’s rumored to rise to 70 cents in July ‘24), digital media ads may be more affordable and effective than print media.

Top 10 Social Media Apps (October ‘23)

1. Facebook: 3 billion (monthly active users) 2. YouTube: 2.5 billion 3. Instagram: 2 billion 4. TikTok: 1.2 billion 5. Snapchat: 750 million 6. X (Twitter): 541 million 7. Pinterest: 465 million 8. Reddit: 430 million 9. LinkedIn: 350 million 10. Threads: 100 million

The flip side of this print vs. digital media debate is that you will probably have much less competition this year when mailing letters and postcards because of the high postage costs. Will this translate to a much higher rate of response from your target audience? Please share with me later this year about which marketing strategies are working and which ones aren’t as effective so that we can learn together.

article continues after advertisement

Distressed Properties & Home Listing Opportunities

Listed below are strategies to either save distressed properties from being foreclosed and/or ways to generate new home listings:

Forbearance agreements: The lender agrees to postpone or delay their foreclosure actions with the delinquent borrower. These foreclosure postponements can last months or years.

Forbearance moratorium expirations: The Covid-19 FHA forbearance moratoriums ended on November 30, 2023, which may affect millions of distressed FHA borrowers who haven’t made a payment for upwards of 3+ years ($100,000+ in unpaid mortgage debt?). The VA moratoriums were extended until May 31, 2024, partly since the federal government probably didn’t want too many distressed home listings hitting the market at the same time. Please consider sending mailings out to both FHA and VA borrowers.

Loan modification: The lender or mortgage service company agrees to reduce the existing interest rate and/or monthly payment so that the loan is more affordable as a way to avoid foreclosure.

Deferment: The lender agrees with the borrower’s request to delay their delinquent payments until a future date. The late payments and penalties are added years later when the loan becomes due.

Reinstatement: After the borrower and lender agree to modify the monthly payments to avoid foreclosure, the loan is reinstated in good standing.

Short sale: If and when the mortgage debt is greater than the current market value for the home (aka “upside-down” or “underwater”), the owner should contact me so that I can negotiate a discounted mortgage payoff and help you obtain the listing and find a buyer. My past client worked on 6,000 short sales (#1 in the US) many years ago and I was their main mortgage broker.

Target the Subconscious Mind

Your subconscious mind is a type of automatic thinking center where your desires to purchase or sell a product or service truly originate. Most people are “impulse buyers” who quickly purchase a product, service, or asset like a home without really thinking it through and closely analyzing the potential pros and cons associated with moving forward with the purchase.

Repetition is the key to programming or deeply influencing others as I intentionally wrote earlier for better memory recall. Advertisers know this as well, so they continually flood your digital screens over and over to inspire you to purchase their products or services offered.

A simple way to find out what your target audience (one person standing next to you or in a hotel ballroom filled with 1,000 people) is to ask them a question like “What do you really want in life?” For many people, they will likely respond with love and money. It’s your turn then to show them how your product or service will help them later find love and money as you build the sales presentation around their needs and interests, not yours.

Interesting Subconscious Mind Facts:

It records everything.

It’s automatic and fully alert.

It takes almost everything literally.

It’s built on habituation and repetition.

It controls 95% to 99% of our thoughts and beliefs.

It’s one million times more powerful than our conscious mind.

It’s deeply affected more by voice tones, body language, numbers, and symbols than spoken or written words.

Influential Sales Strategies: Dale Carnegie

Warren Buffett, one of the most famous wealth builders in the history of the world, publicly gives full credit to Dale Carnegie for helping him overcome his overwhelming fear of public speaking and later becoming one of the best-known sellers and investors of all time.

I also took this brilliant Dale Carnegie course shortly after graduating from USC. To this day, I continue to use many of the same marketing and selling techniques that I learned while also sharing them in real estate and finance courses that I create for others.

A key component of a Dale Carnegie sales and speech course includes the A.I.C.D.C.: Attention, Interest, Conviction, Desire, and Close strategy. Let’s look next at how this sales concept can help you:

A (Attention): You’ve got about eight seconds to grab attention either online or in print like with a postcard. Either way, colorful and vivid images can attract your viewers’ eyes to your ad. In person, you grab their attention by learning their name (usually our favorite word), repeating it every so often, and talking primarily about them and their needs and interests to build rapport and trust.

I (Interest): Please think of the initial attention as akin to a “spark” that you must kindle by boosting the “flames” of interest by continuing to focus on your clients’ needs and interests. Keep asking them questions to find out their root needs and interests. You then speak to them by sharing how your product or service can give them exactly what they’re seeking.

C (Conviction): During this stage, you as the salesperson are certain that the client is interested in what you’re offering. Now, you offer valuable eye-opening statistics to support your claims.

D (Desire): You repeatedly show the prospect how the features or benefits of your product or service will get them what they desire (“Fact, Bridge, Benefit” technique). When successful, the customer’s desire to purchase your product or service will rise from low to high rather quickly.

C (Close): The absolute most important sales step is to close ‘em by asking them to buy your product. Your client may be 100% interested in your product, but may not know what to do next. It’s here where you show them how easy and simple it is to buy your product or for them to sell their off-market home with seller-financing that you mutually agree to and close the deal within a few days. Ask for the close and it’s more likely to happen.

Building a Trusted Network

● Circle or Sphere of Influence: Your friends, family, classmates, current and former co-workers, and connections from clubs, church, and networking groups and their connections as well that may number in the hundreds or thousands of people.

● These friends, family, and business professionals may be found at the local Chamber of Commerce, American Legion, Rotary Club, and Elks Lodge as well as with our Trusted Business Partners (TBP) networking group.

● Building a support network helps alleviate the burden of financial distress and increases opportunities like with our So-Cal Real Estate Investors group that meets at Canyon Lake Golf Club, Shoreline Yacht Club in Long Beach, and online.

● You’re more likely to take on the traits of the five main people in your circle of friends, family, and/or advisors, so choose wisely!!!

Helping Realtors & Investors Close More Deals

I’ve created hundreds of articles about fix-and-flips, short sales, seller-financing (subject-to, wraparounds, & paper flips), foreclosure bailouts, and was featured on the cover of Creative Real Estate Magazine (I was their #1 most published author for 10 years).

I’ve taught real estate licensees and investors across the nation how to find clients, distressed properties, and boost their sphere of influence to find more clients and homes to sell or buy.

If you or your clients have credit issues, I’ve written courses about credit for the two largest real estate publishers in the nation and may help quickly increase your clients’ FICO credit scores.

I can get you fast pre-approvals and help structure the offer with maximum credits to minimize cash to close.

My Realloans team and I will simplify your complex deals so that you and your clients are relieved, calm, happy, and close on time.

I’m affiliated with hundreds of real estate investment clubs and 1031 tax-deferred exchange groups, which have tens of thousands of qualified or all-cash buyers who can close quickly.

I will help your listings by sharing mortgage flyers with you and on my networking platforms to optimize viewer traffic.

2024 can either be your best year ever as a real estate licensee, or investor or it could be quite challenging if you’re not willing to make necessary changes. The choice is yours and yours alone as to your willingness to attempt new creative marketing strategies to boost your sales and purchase numbers.

I’m here to help you reach and surpass your goal targets. The best time to start is today, not next year. Best wishes for success in 2024 and beyond!

Rick Tobin

Rick Tobin has worked in the real estate, financial, investment, and writing fields for the past 30+ years. He’s held eight (8) different real estate, securities, and mortgage brokerage licenses to date and is a graduate of the University of Southern California. He provides creative residential and commercial mortgage solutions for clients across the nation. He’s also written college textbooks and real estate licensing courses in most states for the two largest real estate publishers in the nation; the oldest real estate school in California; and the first online real estate school in California. Please visit his website at Realloans.com for financing options and his new investment group at So-Cal Real Estate Investors for more details.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/01/2024.png4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-01-08 02:23:292024-01-08 02:23:32Helping Realtors Find Clients and Listings in 2024

A regular accountant can perform many of the same functions as a CPA (Certified Public Accountant), including tax preparation and bookkeeping. So how do you know if hiring a CPA is the right fit for your business?

article continues after advertisement

What is the difference between an accountant and a CPA?

An accountant is someone who has earned their bachelor’s degree in accounting or finance.

A CPA has a bachelor’s degree, but has earned additional designations upon graduation.

To become certified, an accountant must have work experience, pass the Uniform CPA Exam, and meet all state licensing requirements. The exam covers their knowledge of business, accounting, taxes, and auditing.

Additionally, CPAs are required to take continuing education courses throughout their careers to stay up to date on laws and regulations.

Because of this certification, a CPA has a fiduciary responsibility to their clients, while an accountant does not. This means CPAs are legally required to act in the best interests of their clients, whereas a standard accountant does not have a license to lose.

Not just tax returns

Almost anybody can call themselves a tax preparer. It does not require extensive education to obtain a Preparer Tax Identification Number (PTIN), which the IRS requires for someone to receive compensation for completing a tax return.

But due to the demanding education and testing requirements that a CPA must fulfill, their expertise goes beyond just preparing and filing an accurate tax return on your behalf.

CPAs work with clients all year long, not just during tax season. Your CPA can typically help you with a wide range of issues, including future tax planning, college or retirement savings plans, or business strategies — whatever your goals entail, a CPA can help you achieve them.

article continues after advertisement

You’re not accountable.

Clients usually seek a CPA to ensure that they are dealing with true professionals who can be held accountable for their actions if ever the CPA code of ethics is not respected or for any other dispute between the client and the CPA.

CPAs have rules of professional conduct and a code of ethics. If they deviate or fail to respect that code, they would face sanctions by the professional body of CPAs. That could include monetary penalties or permanent expulsion from the order of CPAs in severe cases. The accountability rests on your CPA, not on you.

So when should I hire a CPA?

1. When You Are Starting a Business:

A CPA can recommend the best business structure for your company. How you structure your business will have an effect on your taxes – – whether that’s a partnership, an LLC, a sole proprietorship, or a corporation. A CPA will work with you to optimize your business’ goals and recommend legal structures.

2. During Tax Season:

CPAs can prepare tax documents, file tax returns, and strategize ways to minimize your tax liability for the following year. Also, CPAs can represent you if the IRS has questions about your return or if you or your business is audited.

3. In Special Circumstances:

If you’re thinking about taking out a loan for your business, a CPA can help you can recommend the best type of loan for your business, figure out the size of the loan and how payments will affect your cash flow, and prepare financial statements for your loan applications.

Or, when you’re facing significant structural or operational changes to your organization – – such as purchasing a business, merging with another company, planning to sell or close your business, or deciding whether to take on a new partner or dissolve a partnership – – you should consult a CPA about the tax implications for your business and for yourself.

MEET JOHN DUTSON

John is a CPA and the owner of Tax Guardian CPA, a tax preparation firm in Santa Barbara that focuses on detailed, personalized tax prep and consultations for small businesses and real estate investors.

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2024/01/cpa-2.jpg4001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2024-01-05 04:09:182024-01-05 04:09:20Why Choose a CPA?

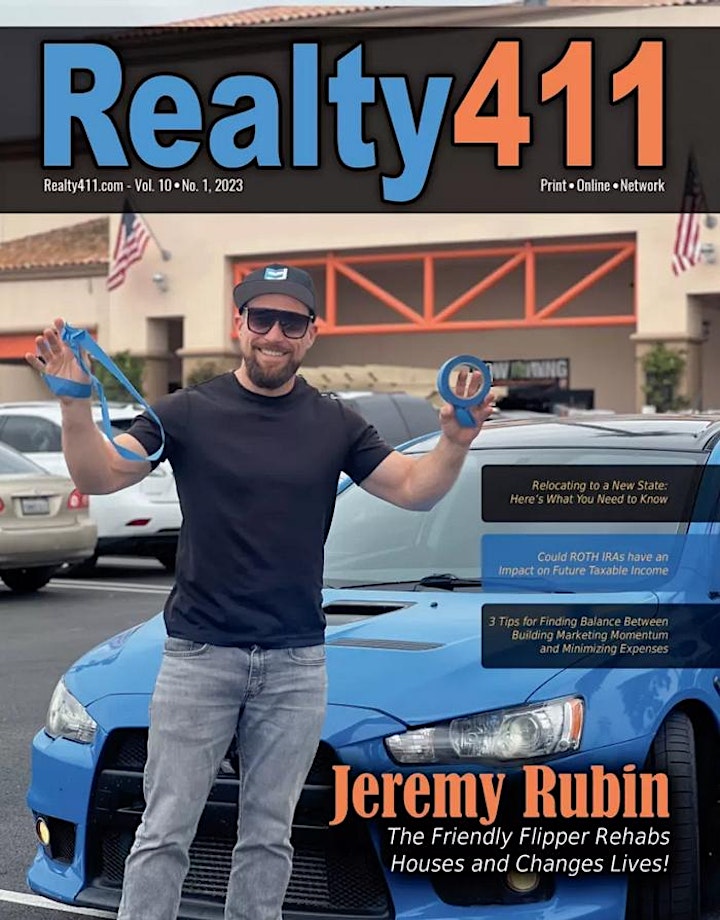

We hope you are enjoying this special season with your loved ones. As we prepare for a new year, this is the perfect time to reflect on some of the important lessons we have learned in 2023.

To help our readers refresh on the most important real-estate insight and strategies we shared this year, be sure to watch a replay of our most recent Virtual Investor Summit.

This replay will explain many strategies for real-estate investing success. Most of our online educators also join us at our in-person events, so be sure to review our live event dates to join us — see our event schedule below as well.

In the meantime, enjoy our latest tips, news, and information with this replay of our most recent online Virtual Investor Summit. Our replay has fantastic information that you simply don’t want to miss — take note of our educator, their topic, and start time below.

Steve Davis Total Wealth Academy Gain Insight on Your Investing Goals — Investors, Know Where to Start From Speaking Start Time: 01:32

Joseph Kimbrough APEX Holdings Let Money Work for You with Real Estate Speaking Start Time: 57:05

Rusty Tweed TFS Properties Maximizing Cash Flow with 1031 Exchanges and Out of State Properties Speaking Start Time: 1:50:00

Jeremy Rubin The Friendly Flipper From Corporate Career to Full-Time Property Rehabber Speaking Start Time: 3:06:23

Jim Edenfield Invest Success Learn About Invest Success and The Great Mile High Real Estate Investors Summit Speaking Start Time: 4:09:42

Joseph V. Scorese BRRRR Loans How to Leverage Direct Lending to Increase Deal Flow and Profits Speaking Start Time: 4:36:08

Hugh Zaretsky REAL Brokerage Learn How to Get Paid 9 Different Ways with the Fastest-Growing Brokerage in the Nation! Speaking Start Time: 4:58:00

Join us in beautiful Pismo Beach, California. The Central Coast of California is truly one of the most scenic and pristine areas of the state. Be sure to visit and learn real estate investing on the beach with our sophisticated colleagues from throughout the area and beyond. Our guests will enjoy a wonderful breakfast mixer. To learn more, CLICK HERE.

Network and learn in Southern California. Connect and learn from top real-estate investment educators. Subjects to be discussed include, multifamily investing, land banking, industrial real estate, infinite banking, asset protection, real estate development, single-family investing, finance and private lending, lead generation for agents/brokers, out of state investing, and more! Be sure to join us for our catered networking lunch, CLICK HERE.

We are back in the East Coast to connect with our readers. Realty411 will host an Investor Summit in the City of Brotherly Love to network, learn, and enjoy a day connecting. Our last event united investors from across the nation and many Eastern states for a wonderful day of education and collaboration. To learn more, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/12/learn.png5001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-12-29 06:34:072023-12-29 06:34:09Learn Online and In Person

Discover the Latest Insight, News and Investment Strategies at Realty411’s National Investor Summit in Southern California

Investors, we have exciting news, insight and networking at Realty411’s new in-person investor summit in Southern California. Our special one-day conference will host incredible educators from around the country, who are ready to share their valuable insight with our guests.

Since 2007, Realty411 has united thousands of investors from across the nation. Guests will receive our latest publication featuring wonderful resources, insightful news and educational articles.

Now is the time to take ACTION — join us to network with sophisticated investors from California and around the country. Upgrade as a VIP Guest ($49) and join us for a delicious buffet lunch as well.

Be sure to pencil this date now and join us in-person to gain specialized insight and knowledge. The information shared on this day could catapult your portfolio to new levels. Discover our new property portal, our VIP perks, plus connect with new and past industry resources.

Learn the Latest Niches in Real Estate + Connect with Influential Investors from across the nation right here in Southern California.

Are you ready to Grow Your Real Estate Business, Portfolio and Network?

Network and learn in Southern California. Connect and learn from top real-estate investment educators. Subjects to be discussed include: multifamily investing, land banking, industrial real estate, infinite banking, asset protection, real estate development, single-family investing, finance and private lending, lead generation for agents/brokers, out of state investing, and so much more!

This is Your Chance to meet TOP Leaders in REI, Local & National Experts:

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/12/National-Investor-Summit.jpg396795dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-12-29 05:14:532024-04-17 02:49:56New In-Person Investor Summit in So Cal – Take Action

Survey of International Living Readers Also Shows Preference for Beach, City Properties, Good Healthcare, Safety

By Ronan McMahon

Cabo San Lucas, Mexico – Ronan McMahon’s Real Estate Trend Alert, a leading source of real-time information for investors on off-market, insider real estate deals in up-and-coming locales, today released the results of a survey that ran in late October with 434 readers of International Living responding. Both people who are professionally active and retirees were surveyed. Portugal is the preferred destination, in second and third place are Costa Rica and Mexico respectively. When deciding to invest in a property, quality of healthcare and safety and crime rates are among the most important criteria investors consider.

article continues after advertisement

Investing in property abroad is no longer an option that is only available to affluent investors, but has gradually become more and more popular with middle class families in the last decade. Through the survey that was conducted with the readers of International Living, Real Estate Trend Alert set out to understand the preferences of American investors in terms of where they want to invest, how much they want to invest, and what they are looking to achieve with their investments.

Investments

The first question pertained to the amount people are planning to invest.

What is the total amount of investment(s) you are planning to make?

A large majority (79.54%) of respondents plan to invest less than $500,000. 38.14% even plan to invest less than 250,000. The numbers look very similar across retired and employed respondents. While at first sight, one might consider the investment amounts modest, it is important to take into account that in many foreign countries the price of real estate is considerably lower than it is in the United States. In Mexico, for example, it is possible to acquire a luxury condo in a five star beach and golf resort for $250,000.

Objectives

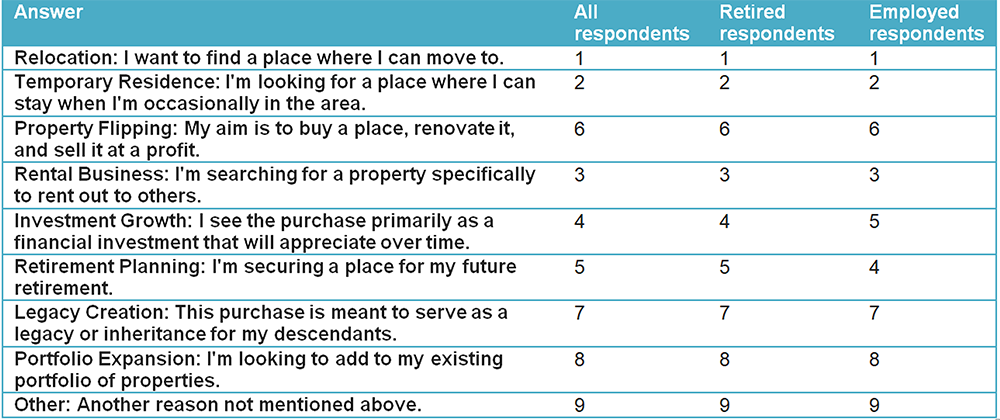

Respondents were also asked about the objectives they seek to realize with their investment(s).

What are your primary objectives with your planned purchase(s)? (Ranked)

The number one reason Americans invest in property abroad is that they want to relocate. In second place comes the search for temporary residence and in third place follows the search for a property that can be rented out. With only a few exceptions, the way respondents ranked their objectives are the same for people who are retired versus people who are employed.

Countries

Respondents were also asked where they plan to purchase real estate.

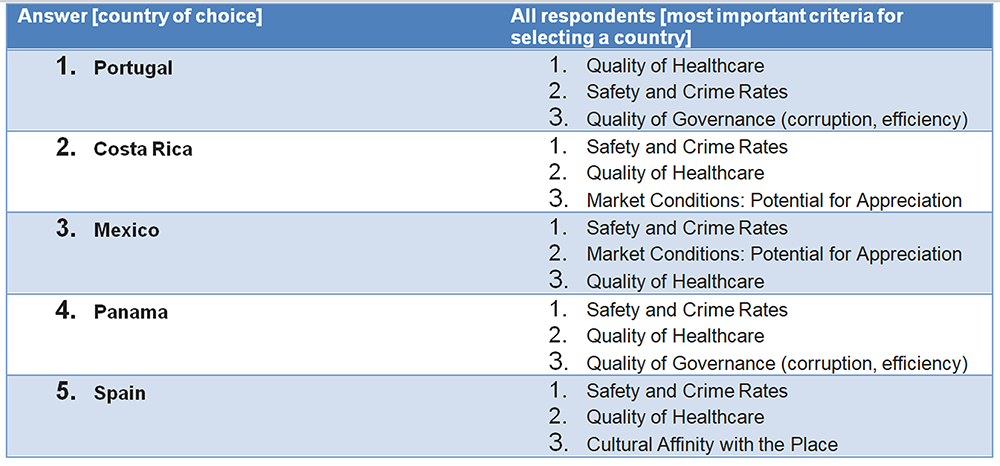

In what countries are you considering purchasing properties? [Top 5]

Portugal came out as the clear winner here, followed by Costa Rica. Mexico, Panama and Spain complete the top five (but the order in which they do so is different for retired Americans versus Americans who are employed).

Types of areas

Investors were also asked in what type of areas they would like to invest.

In what type of area(s) are you considering purchasing properties?

Beach property is the number one category of property purchased by Americans abroad. The city and suburbs follow in second and third place respectively.

Criteria for choosing a country

Finally, respondents were asked what criteria matter most to them when selecting a place to invest. For every country of the top five most popular countries, the three most important criteria were listed for the people who selected that specific country.

View on what people consider important when buying property abroad who selected one of the top five countries.

Safety and crime rates and quality of healthcare are predominantly present in the top three criteria for people who considered any of the top five countries to invest in. Both Costa Rica and Mexico have market conditions (perceived potential for appreciation) in their top three. For people who selected Panama, quality of governance was (on third place) an important factor to consider and Americans who want to invest in Spain attach (on third place) great importance to cultural affinity with the place.

“Americans want to feel safe.”

“The picture we got from the survey is very clear. Americans want to live close to the beach in a country where there is plenty of sun. They also want to feel safe and have high-quality healthcare,” said Ronan McMahon, founder and editor of Real Estate Trend Alert, who’s been a part of more than $2 billion in international real estate transactions over the past two decades.

“When Americans look to invest in property abroad, they do so for many different reasons with relocation being the most important one. People want to move to Portugal, Costa Rica and Mexico first and foremost. Panama takes the third place with retired Americans. When we look at the budgets that people have available to spend on property abroad, with a large majority not planning to spend more than $500,000, it is no surprise that we see Central American countries so prominently represented in the top three most favored countries.”

article continues after advertisement

MEET RONAN MCMAHON AND REAL ESTATE TREND ALERT

Ronan McMahon’s Real Estate Trend Alert (RETA) is a real estate investment newsletter founded in 2008 by international real estate investor and author Ronan McMahon. It’s sourced and written by Ronan and his team of real estate experts who search the globe with boots on the ground for six-months out of the year looking for the best real estate deals. Since its inception, RETA has helped thousands of individual investors access off-market, insider deals in up-and-coming locales the world over. More info at www.ronanmcmahon.com.

Media Contact Ray Young Razor Sharp PR 512.694.6097 [email protected]

Learn live and in real-time with Realty411. Be sure to register for our next virtual and in-person events. For all the details, please visit Realty411Expo.com or our Eventbrite landing page, CLICK HERE.

https://www.realestateinvestormagazines.com/wp-content/uploads/2023/12/Americans-Prefer-Portugal-Costa-Rica-Mexico-for-Overseas-Real-Estate-Investment-featured-image.jpg5001000dulcehttp://www.realestateinvestormagazines.com/wp-content/uploads/2013/04/logo.pngdulce2023-12-18 04:33:182023-12-18 04:33:21Survey: Americans Prefer Portugal, Costa Rica & Mexico for Overseas Real Estate Investment

The company has officially kicked off its franchise offering, vetting franchisees across the nation for potential partnership.

Denver, COLORADO – Invest Success, a real estate investment training franchise known for its best-in-class training and education courses, has just announced the official launch of its franchise opportunity.

The Colorado-based company is pushing to expand nationally, already seeing momentum thanks to its unique program and model. The franchise includes a proven system of processes, development, and marketing strategies all created to draw in students and train them in the best strategies for creating and growing their real estate portfolios.

“We are changing lives through our program already and are excited to now have the opportunity to change lives through our franchise,” stated Jim Edenfield, co-owner of Invest Success.

“The demand for real estate investment education is extremely strong, leaving ample opportunity for our franchisees to grow their customer base quickly.“

Invest Success concentrates on presenting real estate from all angles, enhancing each students’ understanding of different real estate deals, ultimately producing real life results.

“Our franchisees have the opportunity to benefit from our support and training, our established systems, and our branding,” stated Edenfield.

“They will be part of a training model for real estate investment instructors across the country to provide education for people in their area, following a system that generates revenue year-round without relying on real estate market conditions.“

Invest Success is currently accepting applications for new franchise partners. To learn more about the franchise opportunity, visit www.investsuccessfranchise.com or email [email protected].

ABOUT INVEST SUCCESS

Invest Success provides best-in-class training for real estate investment. Students are prepared to take crucial steps towards becoming a successful Real Estate investor, building their portfolio of properties, and even owning their dream home. To learn more about Invest Success, visit www.invest-success.com. To get started with owning your own real estate investment training franchise, visit www.investsuccessfranchise.com.